By Dr Shane Oliver, Chief Economist and Head of Investment Strategy at AMP.

Investment markets and key developments

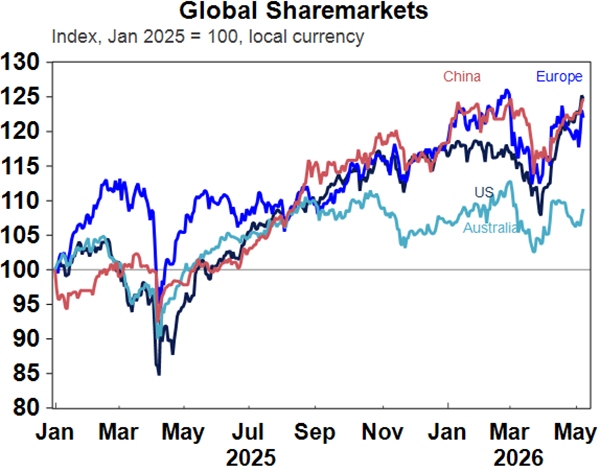

Global share markets rose strongly over the last week led by US shares on the back of renewed hopes for a peace deal with Iran to reopen the Strait, strong US earnings results and mostly good economic data. The Australian share market initially had a strong rise too but ended pretty flat for the week on the back of renewed doubts for an imminent peace deal and Australia’s perceived greater vulnerability to an extended closure of the Strait of Hormuz. For the ASX 200 strong gains in resources and financials were offset by falls in health, IT and retail shares. Bond yields were little changed – rising slightly in the US but falling slightly elsewhere.

Source: Macrobond, AMP

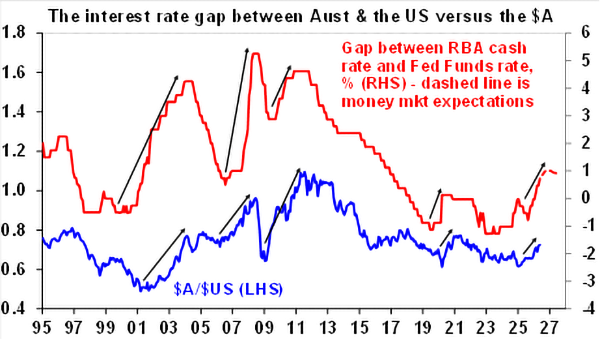

The $A has risen to its highest since April 2022, partly offsetting the relative underperformance of Australian shares. It’s now around fair value of $US0.72 but absent a global recession its likely to rise further in response to the widening interest rate gap to the US and strong commodity prices. Metal, gold and iron ore prices also rose over the past week as did Bitcoin with the $US basically flat.

Source: Bloomberg, AMP

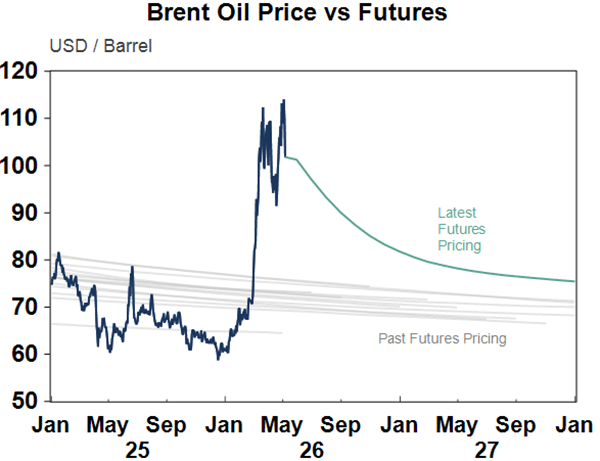

Renewed hopes for a peace deal saw oil prices fall, but it remains messy. The week started badly with an exchange of fire between Iran and the US Navy and UAE as the US sought to escort stranded ships through the Strait, but progress towards a resolution appeared to be resuming again with Trump saying “we’ve had very good talks” with the US proposing a gradual reopening of the Strait and a lifting of its blockade of Iranian ships with negotiations of Iran’s nuclear program to come later. Of course, we’ve heard it all before from Trump and by the end of the week it was all looking shaky again with another exchange of fire between Iran and the US and Iran yet to respond to US proposals. Pressure for a deal remains immense though particularly on Trump with his approval hitting new lows, and Trump’s lack of follow through on many of his threats suggests he wants to end the War and move on. And China appears to be urging Iran to agree to a deal. So, our base case remains that Trump will do whatever is required to stay on the off ramp to peace and that a deal will soon be reached leading to a bigger fall in oil prices.

Source: Macrobond, AMP

Of course, it could just be another false dawn on a peace deal and the clock is still ticking as the longer the Strait remains closed the greater the hit to the global and Australian economies as the world will have to adjust to a 10-15% reduction in global fuel supplies. This would mean even higher fuel prices (a rough calculation is that oil would need to go to around $US150/barrel) and/or fuel restrictions. So far the global economy has been protected by reserve drawdowns, fiscal handouts like fuel tax cuts, just in case buying, expectations that it will be temporary aided by Trump’s regular comments that it will soon be over and the AI boom in the US. But oil crises have always impacted oil prices, shares and economies with a long lag. For example, the full impact on oil prices unfolded over four months in the first oil shock in 1973 and over a year in the second oil shock in 1979. So hopefully we are right and a deal is soon reached. The other big risk is that any deal reached is of low quality – with Iran effectively more aggressive than before and progress towards nuclear weapons just delayed. In which case it could all flare up again down the track.

Source: Bloomberg, AMP

The RBA hiked rates a third time citing upwards impetus from the oil shock to already high inflation and the need to lower demand in the economy below depressed supply. The RBA has less flexibility than most other major central banks which have mostly held rates constant because depending on the country being compared to inflation is further above target here, productivity is weaker and or unemployment is lower. The Norwegian central bank was an exception and hiked rates this week to 4.25% because inflation was “too high” and of concerns about “eroding confidence in the inflation target” if it did not hike – a bit like the RBA. The experience from the 1970s supply side shocks is that the RBA is right to be giving priority to getting inflation back down as a failure to do so will only lead to higher inflation expectations making it even harder to get inflation back down later. In an ideal world fiscal policy should be used to spread the load more equally than mainly mortgage holders but politicians cannot be relied upon to do so and often make inflation worse so its best to rely on the RBA and the blunt instrument of rate hikes. Unfortunately cash handouts to households in the WA Budget (eg $700 for a family with two high school children) are a classic example of how Australian governments are just adding to the inflation problem and making life harder for the RBA and hence mortgage holders. Hopefully the Federal Budget doesn’t make the same mistake. Our assessment is that having hiked three times in a row the RBA can afford to pause at its June meeting, but we are allowing for one final hike in August and then rate cuts next year in response to weak growth bearing down on inflation.

Source: Bloomberg, AMP

The Australian Federal Budget (Tuesday) has more riding on it than has been the case for many years with the Government promising a focus on reforms to address years of poor productivity while at the same time dealing with the impact of the global oil supply shock. Unfortunately, the latter could derail the former – but so far the signs are positive that it won’t. The Treasurer has promised a “responsible budget focussed on resilience and reform” with objectives around cost-of-living support that doesn’t add to inflation, budget savings, lifting productivity and capacity, tax reform, improving economic resilience and intergenerational equity. Key measures under each of these categories look likely to include:

· Cost-of-living support – a $200-$300 tax offset for all salaried workers. It looks like it won’t be means tested which is a bit silly as why do rich people need such help.

· Budget savings – Treasurer Chalmers and Finance Minister Gallagher have announced $64bn in gross savings and indicated that there will be net savings as well. The Treasurer has also indicated that any upward revenue revisions (which could be around $40bn over the forward estimates) will be banked. If this is all the case and any cost-of-living support is more than offset by savings elsewhere it won’t add to inflation.

· Productivity – cuts to red tape and money for states to make productivity enhancing reforms along with a boost to R&D tax incentives. Action to reform company tax as proposed by the Productivity Commission is possible.

· Tax reform – election promises for a 1% cut to the bottom tax rate and the optional $1000 standard tax deduction will be included. But beyond that so far leaks have flagged a return to taxing real capital gains with new builds given a choice of the old or new CGT systems, curtailing negative gearing to either limit the number of properties or limit it to just new builds, a minimum tax on trust distributions of 30% and a phased reduction in the EV fringe benefit tax break. Of course, if this is all there is it will amount to nothing more than a tax hike and not real tax reform. Ideally Australia needs an increase in the GST rate to finance a cut to income tax rates and tax indexation. This would make the tax system less distortionary, provide greater incentive and help deal with intergenerational equity by taxing self-funded retirees more (via the GST) & taxing workers less.

· Economic resilience – so far on this front a $10.7bn fuel security package has been promised to help boost fuel reserves to at least 50 days. There are likely to be more efforts to “make more things in Australia.”

· Intergenerational equity – so far all that’s been talked about on this front are measures to curtail the capital gains tax discount and negative gearing and the minimum tax rate for trusts. Unfortunately, I can’t see how these will improve intergenerational equity. Older generations have got the benefit of these tax concessions to grow their wealth and now they are being curtailed for the young! What’s more the property tax changes won’t fix the undersupply of housing. The key ways to improve intergenerational equity are to boost productivity growth so living standards grow at a rate older generations experienced, get the housing balance right with more supply and less immigration and raise the GST and cut income tax.

Ideally the budget needs to do these three things: cut government spending by around $100bn over the period to 2029-30 taking it back to around its long-term norm of around 24.8% of GDP to provide more space for private spending; provide serious tax reform and not just tax hikes; and slash red tape and provide more incentives to invest. It should also include a return to firm fiscal rules around spending, tax and the budget balance with a reform of the Charter of Budget Honesty to refocus on the headline budget deficit given the use of “off-budget” spending.

In terms of the budget numbers we will likely see this financial year’s underlying cash deficit forecast revised down to around $25bn (from $36.8bn in MYEFO) and next year’s to $24bn (from $34.3bn) with deficits still projected out to mid next decade. The Government’s growth forecasts are likely to be revised down to 1.5% for the next financial year with subsequent years revised down slightly due to slower productivity growth. Next financial year’s unemployment forecast is expected to remain around 4.5% and inflation is forecast to fall to 2.5% after 5% this financial year. Net migration forecasts are likely to be revised up.

Here’s another happy song in Andy Kim’s version of Baby I Love You. “So cool in a dorky way” sums it up. He also co-wrote Sugar Sugar, which was record of the year in 1969 and sang as part of The Archies.

Major global economic events and implications

US economic data was mostly solid. As with the manufacturing ISM the services conditions ISM remained strong in April, albeit down a bit. The main concern remains that prices paid remains high. New home sales rose but remain relatively low. The Atlanta Fed’s GDP Now growth indicator is tracking at a 3.7% annualised pace this quarter.

Source: Macrobond, AMP

Jobs data was mainly solid suggesting a stabilisation in the labour market after a slowing through last year. The job openings and quits rates were pretty stable in March and the hiring rate actually rose. The ADP private employment survey rose solidly in April and initial jobless claims remain low. So no need for the Fed to rush into a rate cut here.

Source: Macrobond, AMP

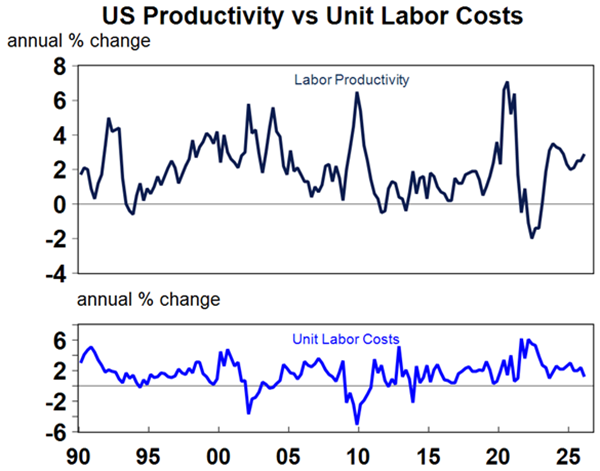

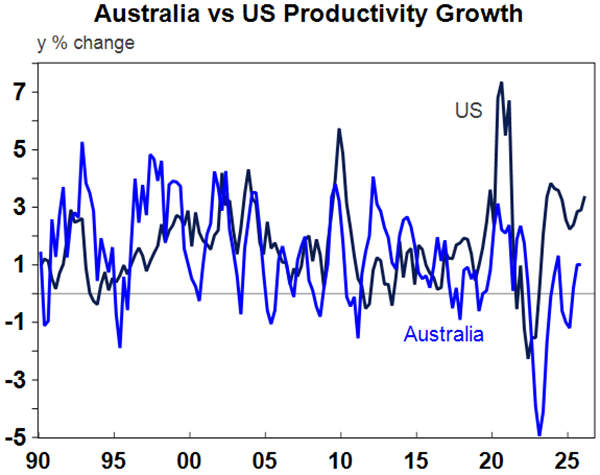

US productivity growth slowed to a 0.8% annualised pace in the March quarter, but remains very strong at 2.8%yoy and means that unit labour costs are up just 1.2%yoy posing very little upwards pressure on inflation.

Source: Macrobond, AMP

US productivity growth continues to run well ahead of that in Australia. This translates to lower growth in living standards here and highlights the urgent need for productivity enhancing reforms in Australia.

Source: Macrobond, AMP

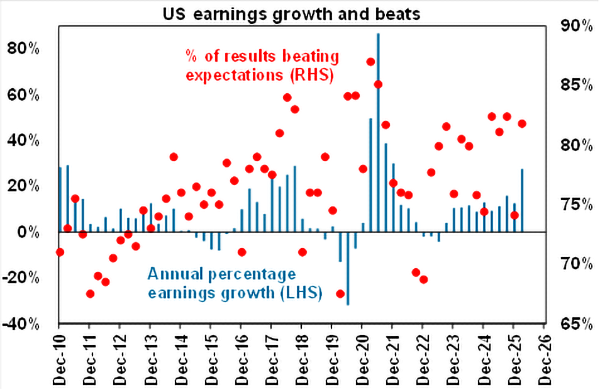

US profits are booming. Nearly 90% of US S&P 500 companies have now reported with 81.8% beating expectations and consensus earnings growth for the quarter moving up to a whopping 28%yoy, up from 14%yoy a month ago. This is the strongest pace since 2021. Tech companies are leading the charge with earnings growth around 59%yoy, financials at 24%yoy, cyclicals up 11%yoy and non-cyclicals seeing flat growth.

Source: Bloomberg, AMP

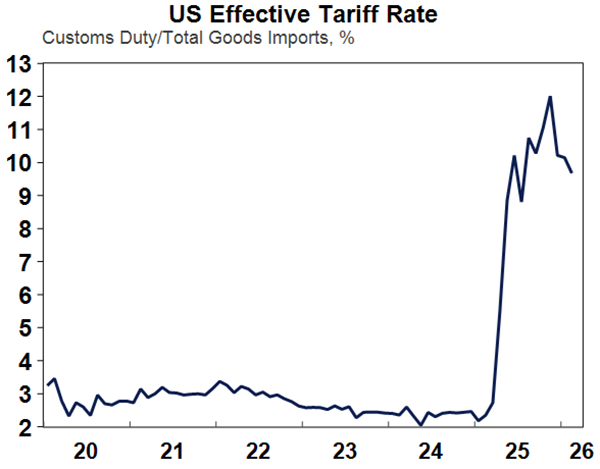

US tariffs have taken a back seat lately but are still bubbling away. A week ago, Trump threatened the EU with 25% auto tariff citing dissatisfaction with the EU’s implementation of its trade agreement. It’s a risk, but likely to be avoided though much like a similar threat to Korea earlier this year. Meanwhile, the Trump Administration is now starting to pay out refunds for the reciprocal and Fentanyl tariffs that the US Supreme Court declared illegal which could amount to $US166bn. This will lead to a temporary fiscal stimulus and budget deficit blow out. Those tariffs were then replaced with a temporary 10% tariff (under section 122) from late February that will expire on 24th July, but these have now also been ruled illegal by the US Trade Court which will likely lead to another round of appeals. In any case they will likely be replaced by more permanent section 301 tariffs taking them back to where they were before the Supreme Court decision. Meanwhile from a peak of nearly 12% the average effective US tariff rate has fallen back to around 10% thanks to import substitution from countries with high tariffs to those with lower tariffs. It’s still way up on where it was at the start of last year…so still adding to US costs and distorting trade.

Source: Macrobond, AMP

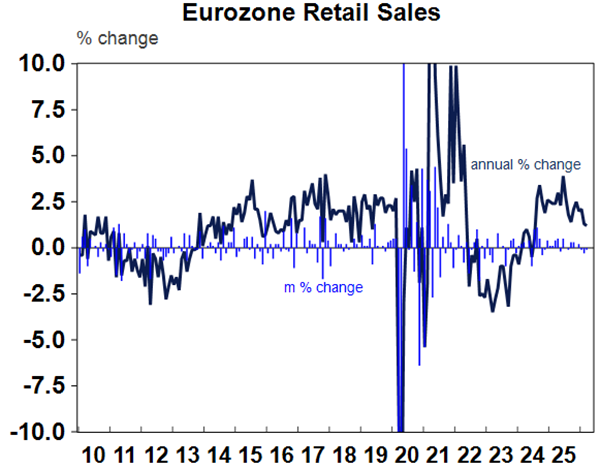

Eurozone retail sales are slowing again.

Source: Macrobond, AMP

Australia economic events and implications

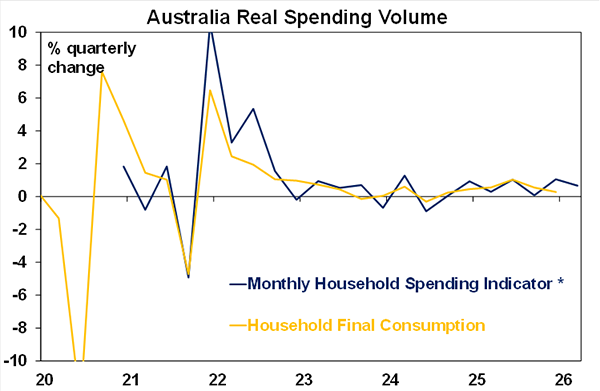

Household spending rose a strong 1.6% in March and is up 6.3%yoy. A 5% rise in fuel spending due to higher prices was part of it but spending growth was solid in most categories and real spending rose a decent 0.7%qoq in the March quarter. This suggests that consumer spending growth likely had a good head of steam going into the oil supply shock.

Source: ABS, AMP

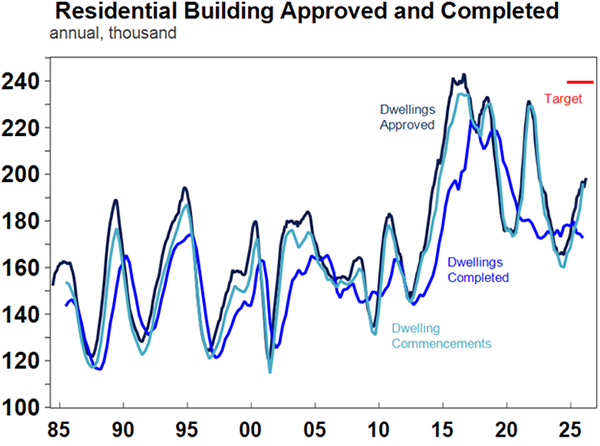

Home building approvals fell 10% in March driven by volatile units, but this was after a 31% rise in February leaving in place a rising trend. Approvals are running around an annual pace of 205,000 new dwellings which is up from recent lows but is still well below the Housing Accord target of 205,000pa and likely to slow over the year ahead due to rate hikes and cost increases and uncertainty caused by the oil supply shock.

Source: Macrobond, AMP

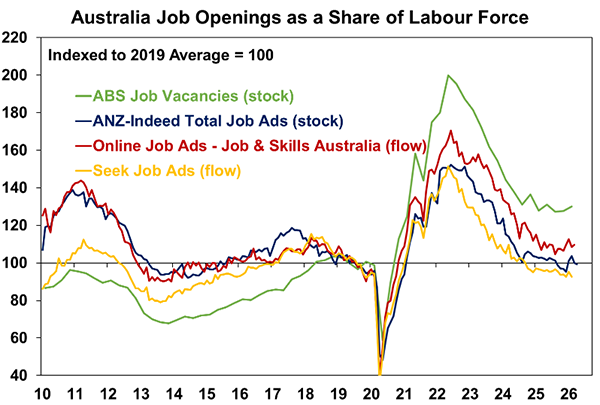

Job ads slowed again in April according to the ANZ-Indeed survey. This could be a sign of uncertainty due to the oil shock and rising rates.

Source: Bloomberg, AMP

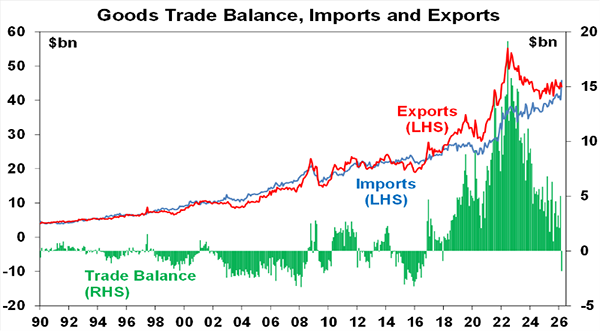

Australia swung back into a goods trade deficit in March with a surge in data centre equipment and fuel imports. Net exports are likely to cut 0.4 percent from March quarter GDP but this should be offset by investment & inventories.

Source: Bloomberg, AMP

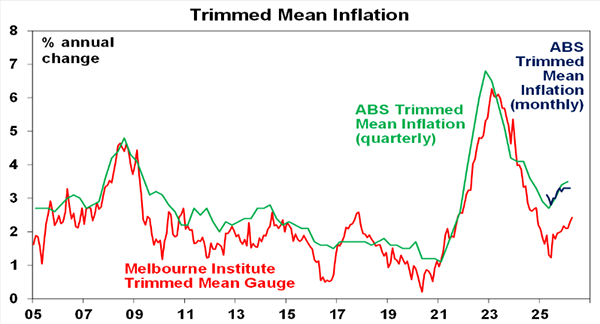

The Melbourne Institute’s Inflation Gauge for April showed an acceleration in trimmed mean inflation.

Source: Bloomberg, AMP

What to watch over the next week?

Globally the summit between President’s Xi and Trump (Wednesday and Thursday) will be watched for any progress in easing trade tensions.

In the US, CPI data for April (Tuesday) will likely show prices rising 0.7%mom due to higher energy prices & rents. This will see annual inflation rise to 3.7%. Core inflation is also expected to pick up to 0.3%mom or 2.7%yoy. In other data expect a modest rise in existing home sales (Monday), slower growth in retail sales (Thursday) and a slight rise in industrial production for April but a pull back in the May New York manufacturing index (Friday).

Chinese inflation data for April (Monday) is expected to show a sharp rise in CPI inflation to 1.8%yoy reflecting higher fuel prices from 0.5%yoy in March.

In Australia, the Budget will be the key focus on Tuesday (see earlier for our preview). On the data front expect the Westpac/Melbourne Institute consumer survey for May (Tuesday) to show continued very weak levels of consumer confidence. Likewise, the NAB business survey for April (also Tuesday) will likely show continued weak in business confidence with some softening in business conditions and ongoing high levels for price indicators. March quarter wages data (Wednesday) will likely show wages growth of 0.8%qoq taking annual growth down slightly to 3.3%yoy, which is well below inflation of 4.1%yoy in the quarter. March quarter housing finance data (also Thursday) will likely show a 3% or so fall in housing finance growth reflecting the move back to rate hikes.

Outlook for investment markets

Global and Australian share markets have likely seen the worst from the War and oil shock if the flow of oil quickly resumes but the risk of further falls taking us to a 15% top to bottom correction remains high given uncertainty around the peace talks and flow of ships through the Strait along with still stretched valuations, political uncertainty associated with Trump & the midterm elections and worries about private credit and the impact of AI. However, returns should still be positive for the year as a whole thanks to Fed rate cuts likely later in the year, Trump still likely to pivot to consumer-friendly policies and solid profit growth.

Bonds are likely to provide returns around running yield.

Unlisted commercial property returns are likely to be solid helped by strong demand for industrial property associated with data centres.

Australian home price growth this year is likely to slow to around 3% due to poor affordability, RBA rate hikes and the hit to confidence from higher fuel prices and the War.

Cash and bank deposits are expected to provide returns around 4.25%.

The $A is likely to rise as the interest rate differential in favour of Australia widens as the Fed holds then cuts and the RBA hikes. Fair value for the $A is around $US0.72.