Introduction

Three months ago there was much optimism about the Australian economic outlook. GDP regained its pre pandemic level, confidence was strong, the jobs market was roaring, there was minimal community coronavirus & vaccines were providing optimism of a more sustained reopening. Since then renewed coronavirus outbreaks of the Delta variant have seen the near-term outlook turn pear shaped – notably in NSW & Victoria. However, much as the near term is depressing in lockdown states there are good reasons for optimism about 2022.

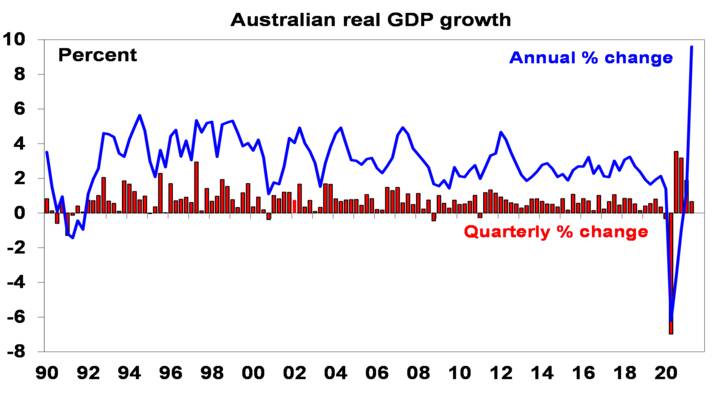

June quarter GDP slowed less than expected

The June quarter saw GDP up 9.6% from the lockdown depressed June quarter last year, but quarterly growth slowed to 0.7%qoq. Thanks to smaller detractions from stocks & trade and very strong growth in public demand (which contributed 0.5 percentage points to growth) this was above our final estimate for a 0.3% gain and well above our initial estimate of a -0.1% decline and avoids the label of a double dip technical recession as September quarter GDP is almost certain to be negative – providing of course we see some recovery into year end.

Source: ABS, AMP Capital

While domestic final demand rose a strong 1.7% – with consumer spending +1.1%, business investment +2.3%, dwelling investment +1.7% & public demand +1.9% – stocks detracted -0.2% points from growth and net exports -1% points.

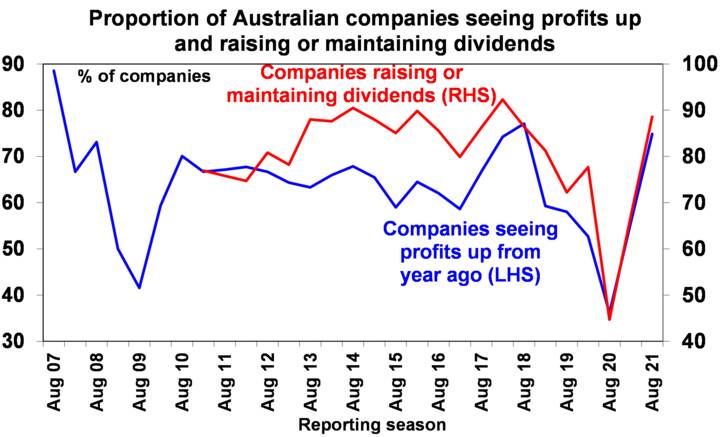

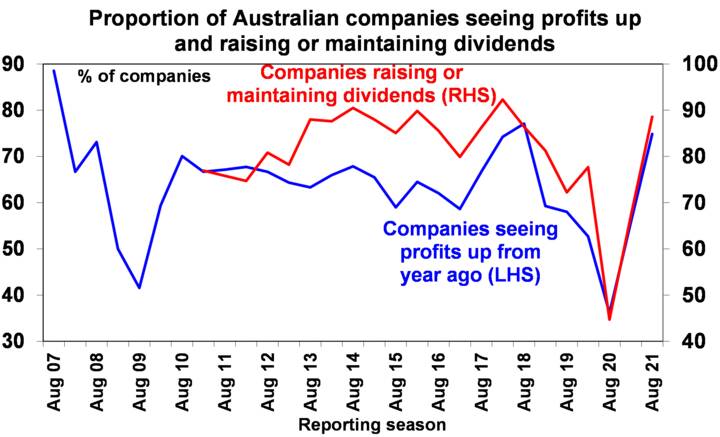

Consistent with the growth rebound since first half last year, the June half earnings reporting season saw listed company profits rise nearly 50% last financial year driven mainly by resources & banks, with 75% of companies seeing profits up. But the big positive was a huge return of capital to shareholders – with 89% of companies raising or maintaining dividends driving a record dividend payout of nearly $40bn and over $20bn in buybacks.

Source: AMP Capital

First the bad news

The news flow since late June has been bleak:

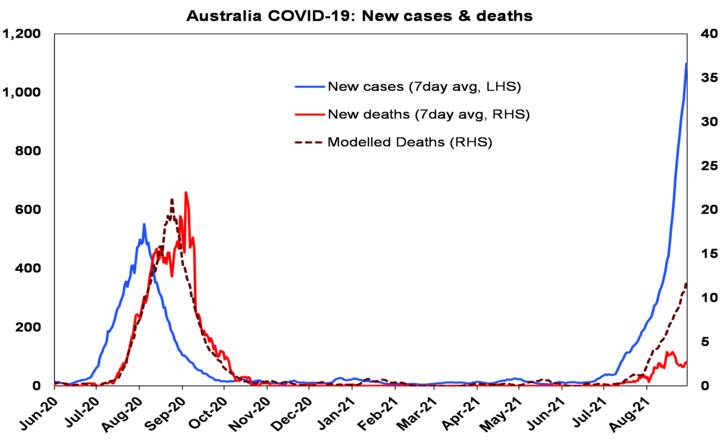

- Locally acquired coronavirus cases have surged – driven mainly by NSW but with problems in Victoria & the ACT too.

Source: covid19data.com.au

- This has led to various hard lockdowns notably in Sydney and Melbourne with both likely to be extended into October.

- Our rough estimate is that the lockdowns since late May are costing the economy around $25bn in lost output and will result in a 4% fall in September quarter GDP. And of course, there is the psychological costs of lockdowns too.

- This is occurring when other developed countries are reopening thanks to being more advanced in vaccinations – leading to a sense that Australia is being left behind.

- Even when reopening comes as vaccination targets are met it will be very different to last year’s reopening. That occurred when coronavirus cases had fallen to around zero, but this time coronavirus cases are likely to be running much higher. While people in Europe, the UK & the US may be used to this (eg, the same number of per capita cases as the UK is now seeing would mean 13,000 cases a day in Australia), it may take a bit of getting used to in Australia which may act as a constraint on confidence, and hence the pace of economic recovery, initially, compared to last year.

- The degree of reopening that can safely occur without problems in hospital systems when the national 70% & 80% of adults’ vaccination targets are met (which mean that 44% and 36% of the whole population will still be unvaccinated) may initially be limited if daily case numbers remain high in some states, and the zero case states (like WA & Queensland) may delay the opening of their borders until higher vaccination rates are achieved.

…but there is good news too

While it would be wrong to get too confident – as coronavirus has had a few occasions over the last 18 months where it looked under control only to flare up again – there is reason for optimism and this, along with the strong return of capital to shareholders, partly explains why the Australian share market remains relatively resilient.

- First, while the lockdowns are very painful, Australia’s policy of suppression has saved lives. If we had taken a laxer approach and had the same per capita number of deaths as the UK and US, we would have lost an extra 48,000 people.

- Second, while the vaccines are less effective in preventing infection from the Delta variant (at 60-80% effective), look to require top ups and may have to be tweaked against new variants, they remain highly effective in preventing serious illness (at 85-95%). This is evident in the UK (where deaths are running around one fifth the level predicted on the basis of the last wave), Europe, Canada and in highly vaccinated US states. It can also be seen in Australia where deaths in this wave are running around one quarter the level predicted on the basis of Victoria’s second wave last year likely thanks to high levels of vaccination amongst older/at risk people.

Source: ourworldindata.org, covid19data.com.au, AMP Capital

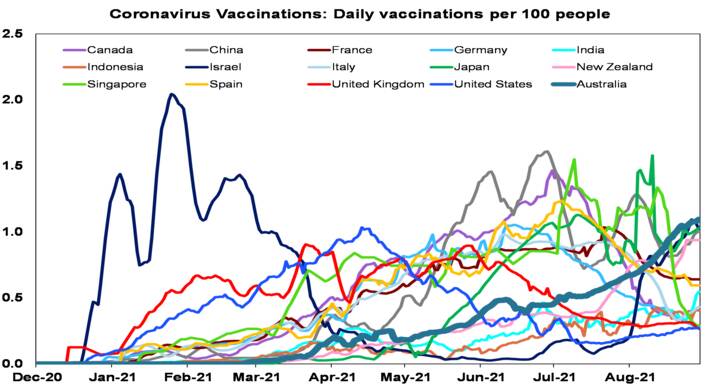

- Third, the pace of vaccination in Australia has doubled from 1 million vaccines a week to nearly 2 million a week over the last six weeks. At the current rate we will reach the first national reopening target of 70% of the adult population in October, 80% of the adult population in November and 80% of the whole population (which may be needed for a safe reopening) in December and 90% of the whole population (which would be ideal) in January. Of course, incentives may be needed to reach the higher vaccination rates – vaccine passports (no jab, no entry) are being implemented and will help in this. NSW is about 3 weeks ahead of the national average.

Source: ourworldindata.org, AMP Capital

- Fourth, while the process of “learning to live” with covid may mean that the initial part of the recovery will be slower than seen last year, pent up demand (thanks to government support payments and constraints on spending in the lockdowns) and a reasonable degree of job security (with state business support payments contingent on businesses maintaining their workforce) along with bank payment holidays will still see significant spending unleashed once reopening occurs which will spur recovery through 2022.

- Fifth, despite the lockdowns the ABS’s business investment survey of July/August still points to significant growth in investment this financial year.

- Sixth, monetary policy will likely be easier as the hit from the lockdowns and a slower initial recovery results in a higher unemployment profile through next year than the RBA has been assuming. We expect the RBA to delay the tapering of its bond buying and to continue buying bonds at the rate of $5bn a week into early next year and the first RBA rate hike is now likely pushed back into 2024.

- Finally, Australia will benefit from the cyclical recovery globally. While peak global growth will probably be seen this year with global GDP growth of 6% it’s still likely to be strong next year at 5%, increasing vaccination globally allows a continuing reopening. This assumes that China moves to boost its growth rate which has slowed lately.

The Australian economy – rough now, better in 2022

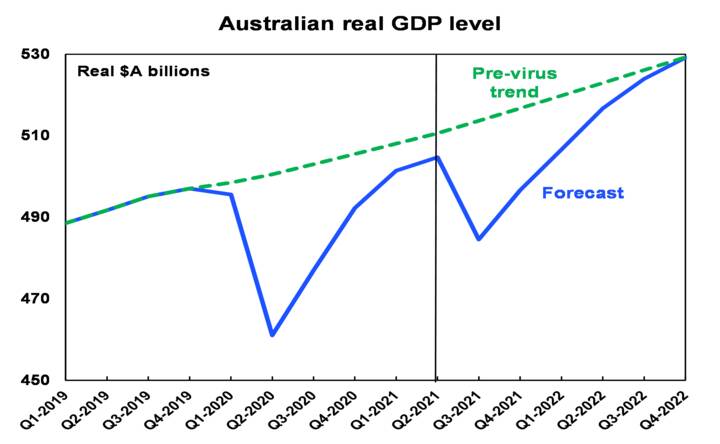

The Australian recovery will see a big setback this quarter (of around -4% for GDP), but the start of a gradual reopening from October gathering pace later this year and through next year as higher vaccination rates are reached should see the recovery start to get back on track in 2022. While growth though this year is likely to be just 1% (compared to our expectation for 4.8% 3 months ago), it’s likely to be around 6.5% through next year.

Source: ABS, AMP Capital