By Dr Shane Oliver, Chief Economist and Head of Investment Strategy at AMP.

Investment markets and key developments

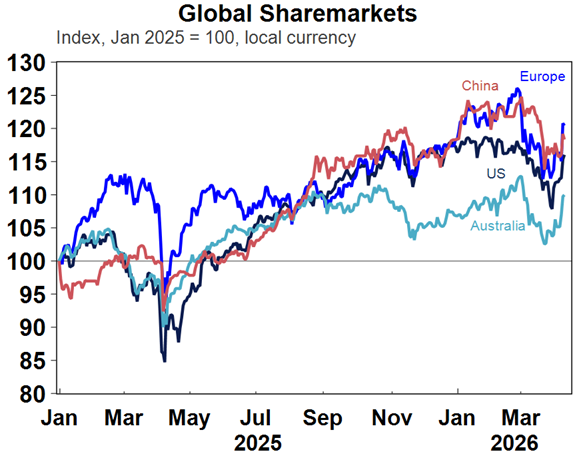

Share markets rose sharply in the past week as the US and Iran announced a ceasefire with optimism this will ultimately lead to an end to the conflict, despite indications the ceasefire is off to a shaky start. For the week US and global shares are up around 4% and Australian shares are up around 4.2% with gains led by miners, banks, property and consumer shares with energy shares down. Bond yields fell on hopes lower oil prices will reduce the threat to inflation but they’re well up on this year’s lows.

Source: Macrobond, AMP

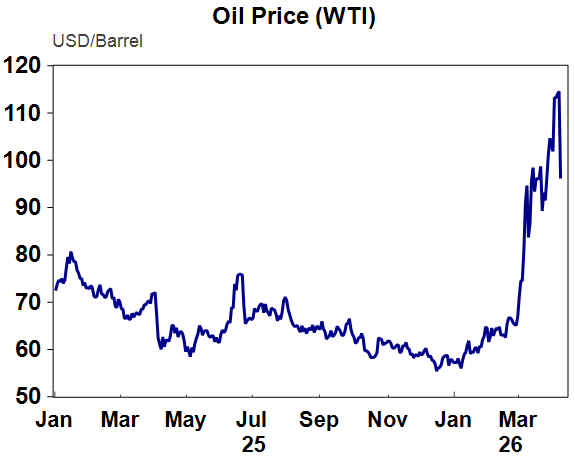

Oil prices fell sharply from recent highs on the ceasefire news but remain just below $US100 a barrel on uncertainty about whether the ceasefire will stick or not. West Texas remains above Brent reflecting increased demand for US oil.

Source: Macrobond, AMP

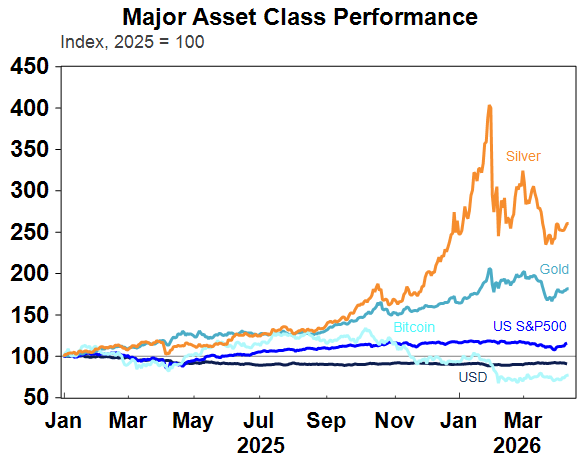

The risk on tone saw the $US fall and the $A rise back above $US0.70 with gold, Bitcoin and copper also up. Iron ore prices fell but remain solid around $US105/tonne.

Source: Macrobond, AMP

TACO Tuesday – will Trump’s ceasefire stick? Trump’s announcement of a two-week ceasefire was good news and consistent with our base case that the War will be relatively short. Trump appears to have become increasingly desperate (evident in his petulant “Open the F…… Strait” comment) with his poll support collapsing, markets threatening to riot and the reality that any follow through with his threat of the “complete demolition” of Iranian power plants and bridges would have made the situation worse as Iran would simply retaliate against its neighbours further pushing up oil prices. Trump may claim he is just playing the “madman” as part of a negotiating ploy but it risks backfiring if he never delivers, and if he does ever deliver on his extreme threats, he will likely further lose domestic and international support (which is already weak). While Trump has military superiority on his side, Iran has weaponised the Strait of Hormuz to control global oil supplies. Trump maybe (with Israel’s suggestion) thought he would be fighting another Venezuela, but it turned out to be more like Vietnam – the US had overwhelming military might, but North Vietnam and the Vietcong still won by 1975 using so called “asymmetric warfare”. So, it has become a sort of MAD (mutually assured destruction) stand off from which Trump had to back down (or literally “chicken out”), but this appears to be partly on Iran’s terms.

It’s a messy TACO with a lot of uncertainty. The ceasefire is off to a shaky start with Israel firing missiles at Lebanon, Iran crying foul and the number of ships moving through the Strait remaining limited. This could just be teething problems though with Israel opening talks with Lebanon and uncertainty around whether ships have to pay $2million to Iran to use its Strait toll gate system (Trump says no, Iran says yes) – but it highlights how fragile the ceasefire is. More fundamentally, the likelihood of a quick deal from talks between the US and Iran seems low given how far apart the US and Iran are but there is a good chance Trump will want to extend the ceasefire with an excuse that talks are continuing. More fundamentally if a deal is reached its unclear as to whether it will be sustainable as while Iran has been weakened in terms of its conventional military its ability to engage in asymmetric warfare – by attacks on its neighbours and by controlling the Strait – remains, which the US, its Gulf allies and much of the rest of the world may not accept indefinitely. This would point to a resumption of the conflict at some point – maybe after the midterms when Trump is less politically constrained or if his polling gets so bad that he has nothing to lose by escalating again.

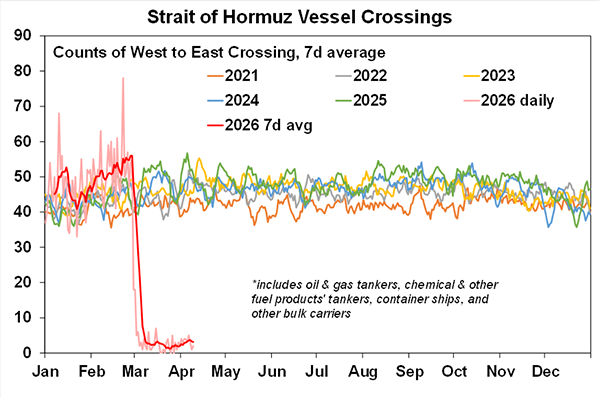

The key thing to watch for remains a significant and sustained pick up in the number of ships coming through the Strait of Hormuz – it has picked up but it’s a fraction of normal levels. But if this were to occur even with Iran collecting a fee it could allow the War to continue but with less impact on the global economy and markets.

Source: Bloomberg, AMP

Even if there is a sustained and extended ceasefire leading to a quick end to the War and/or a sustained increase in ships flowing through the Strait it will take months for global oil flows to return to normal. This is because it will take time to reopen shuttered energy production in the Gulf (weeks for oil, potentially years for some gas plants), to then load this on ships and for those ships to arrive at importing countries including in Asia then for refineries to ramp up and again and refined products to flow to countries like Australia.

So, some near term stagflationary impact of higher inflation and weaker growth is likely baked in, but if oil starts to flow again it would be temporary. In Australia we see inflation peaking around 5-5.5% in the current quarter and GDP growth slowing to around 1.5% this year. This assumes that the ceasefire holds and morphs into a longer-term cessation of conflict or at least a return to more normal oil flows from the Gulf, in which case the boost to inflation and hit to growth will be short-lived. Obviously if the War resumes and the Strait remains effectively closed then the boost to inflation will be bigger and longer and there would be a high risk of recession.

For central banks wary of letting inflation expectations rise the focus is likely to be on the boost to inflation rather than the hit to growth. This is particularly the case in Australia where inflation was already well above target and signs of rising wage growth pressures – for youth and the minimum and award wages for starters – will worry the RBA. So, we are allowing for the RBA to hike again. This is likely to occur in May but if the ceasefire sticks and is extended there is a good chance the RBA will decide to hold.

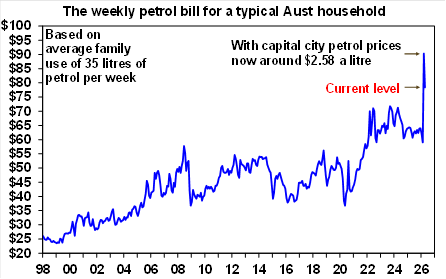

The hit to Australian households has fallen thanks to the fuel tax cuts but remains significant. Petrol prices have fallen from around $2.58/litre at their high to around $2.25/litre thanks to the cuts to fuel excise and GST. This has lowered the hit to household budgets compared to February from around $31 a week at the high last month to around $19 a week now (or $73 a month). It’s worse for those with diesel vehicles though as diesel prices have now reached a new record high. If the Strait quickly reopens then Australia should be able to make it through without fuel rationing, but if not then it’s likely to be necessary from late next month.

Source: Bloomberg, MotorMouth, AMP

The anticipation and then announcement of the ceasefire and optimism that the US and Iran are now on the off ramp to end the War has seen share markets recover around 70% of the falls they saw into the lows last month. And they have broken through key technical resistance levels which is a positive sign. We lean optimistic that Trump will find a way to keep the ceasefire going and extend it which should support further gains. Similarly, if the Strait shows further significant signs of reopening even if the War continues. But the ceasefire could be just another flip flop from Trump of which there have been lots since the War started so it wouldn’t be at all surprising to see a return to an escalation. This means that the near-term risks for oil on the upside and shares on the downside are very high and a retest of share market lows or new lows taking shares to our forecast for a 15% top to bottom correction this year is still possible. As such, it remains a time for those with a short-term investment horizon to remain cautious.

Major global economic events and implications

US economic data was mixed. December quarter GDP growth was revised down to just 0.5% annualised, growth in personal income and spending was weak in February and the personal savings rate fell to well below pre-Covid levels. Underlying capital goods orders were solid in February, but the services ISM for March started to show the impact of the War with conditions down, particularly for employment and prices paid spiking to their highest since October 2022. Meanwhile, core private final consumption deflator inflation came in as expected at 3%yoy but with a solid rise in core goods inflation likely due to tariff pass through. The minutes from the last Fed meeting showed it still biased towards cutting rates at some point but grappling with risks to both inflation and jobs. For now, it’s likely to remain on hold with the money market pricing in about a 20% chance of a cut by year end.

Japanese consumer confidence fell sharply in March.

Chinese CPI inflation edged down to 1%yoy in March with core inflation falling to 1.1%yoy, but producer price inflation turned positive at 0.5%yoy for the first time since 2022 on the back of higher energy costs pointing to higher CPI inflation ahead.

The RBNZ left rates on hold at 2.25% and while it acknowledged the War could weaken demand it seemed a bit more concerned about the impact on inflation.

Australia economic events and implications

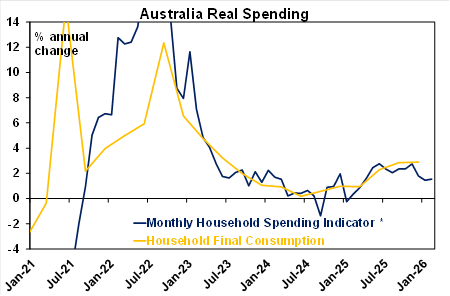

Consumer spending appeared to be cooling prior to the War. Household spending for February rose a slightly stronger than expected 0.3%mom or 4.6%yoy, but this was boosted by the purchase of tickets for future recreational events and in any case so far points to a loss of momentum in consumer spending in the March quarter, particularly once the rise in inflation is allowed for – see the next chart. New motor vehicle registrations also slowed in the March quarter consistent with slowing consumer spending, although EV sales reached a record 15% of the total with the War to provide a further boost to this. ANZ job ads also fell 3.1% in March which could be noise or the start of reduced hiring.

Source: ABS, AMP

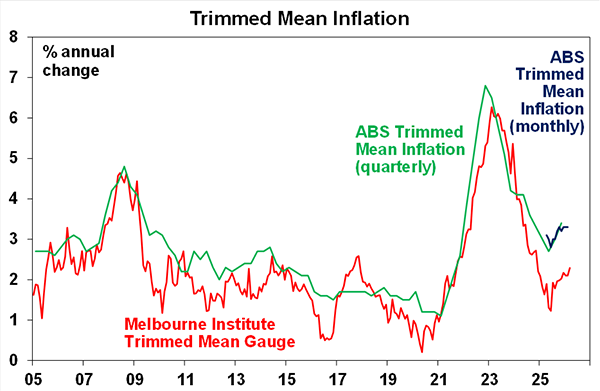

Meanwhile, the Melbourne Institute’s March Inflation Gauge showed a sharp 1.3%mom rise in the headline inflation taking it to 4.3%yoy as higher fuel prices impacted. There was some slowing in its estimate of trimmed mean inflation in the March quarter, but there was a pick in March and over the year to March.

Source: Bloomberg, AMP

What to watch over the next week?

In the US expect producer price inflation for March (Tuesday) to show a sharp rise on the back of the rise in oil prices. Manufacturing surveys for the New York and Philadelphia regions for April are also likely to show a rise in prices and weaker conditions with NAHB’s home building conditions index (Wednesday) remaining weak. Industrial production data for March (Thursday) is expected to show a modest rise. The US March quarter profit reporting season will also start to ramp up. Consensus expectations are for 14%yoy earnings growth, but this is likely to end up around 17%yoy allowing for average beats, which will be the strongest in four years. Tech is likely to continue to lead the charge with earnings growth of around 30%yoy.

Chinese March quarter GDP data (Thursday) is expected to show growth remaining at 4.8%yoy helped by a continuing strong contribution from net exports. However, March activity data is likely to show some slowing in growth in industrial production and retail sales after stronger than expected growth in January and February.

In Australia, expect the Westpac/MI consumer sentiment index for April (Tuesday) to show a further sharp fall on the back of higher fuel prices, ongoing expectations for higher interest rates and general uncertainty flowing from the Iran War. The March NAB business survey (also Tuesday) is also likely to show a fall in confidence and conditions and a rise in cost and price pressures. Jobs data for March due Thursday is likely to show a 5000 rise in employment after a surprise 49,000 gain in February and unemployment rising slightly holding at 4.3%. Speaking events by RBA Deputy Hauser on Tuesday and Thursday may provide an update on RBA thinking.

Outlook for investment markets

Global and Australian share markets may have seen the worst from the War and oil shock if the flow of oil quickly resumes but the risk of further falls taking us to a 15% top to bottom correction are high given uncertainty around the ceasefire and flow of ships through the Strait along with still stretched valuations, political uncertainty associated with Trump & the midterm elections and increasing worries about private credit and the impact of AI. However, returns should still be positive for the year as a whole thanks to Fed rate cuts likely later in the year, Trump still likely to pivot to consumer-friendly policies ahead of the midterms and solid profit growth.

Bonds are likely to provide returns around running yield.

Unlisted commercial property returns are likely to be solid helped by strong demand for industrial property associated with data centres.

Australian home price growth is likely to slow to around 3-5% due to poor affordability, RBA rate hikes and the hit to confidence from higher fuel prices and the War.

Cash and bank deposits are expected to provide returns around 4.25%.

The $A is likely to rise as the interest rate differential in favour of Australia widens as the Fed cuts and the RBA hikes. Fair value for the $A is around $US0.72.