By Dr Shane Oliver, Chief Economist and Head of Investment Strategy at AMP.

Investment markets and key developments

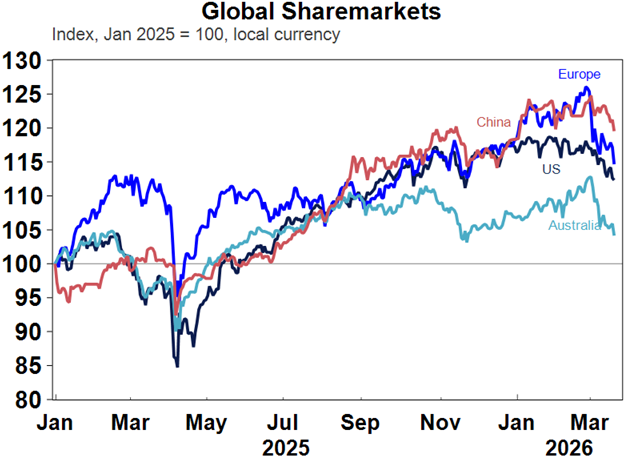

Global share markets had another poor week as the Iran War continued, and the Strait of Hormuz remained effectively closed. This was not helped by contradictory messages coming from the Trump Administration with reports it is considering using troops to takeover Iran’s Kharg Island oil export facility – which would likely escalate the conflict including via more Iranian attacks on regional energy facilities. Then after markets closed on Friday and most likely in response to renewed oil price rises and share market falls Trump posted that he is considering “winding down” the US War on Iran, but this was after ruling out a ceasefire earlier in the day! Oil prices remained around $US100 a barrel – with West Texas little changed for the week but Brent up another 9% or so to $112 a barrel. For the week US shares fell 1.9%, Eurozone shares lost 3.6%, Japanese shares fell 0.8% and Chinese shares fell 2.2%. Reflecting the worries about a boost to inflation and a hit to growth, along with another RBA rate hike, Australian shares fell another 2.2% with energy, utility and consumer staple shares up but most other sectors down. From this year’s highs US shares are down 7%, Eurozone shares are down 11%, Japanese shares are down 9% and Australian shares are down 8%.

Source: Macrobond, AMP

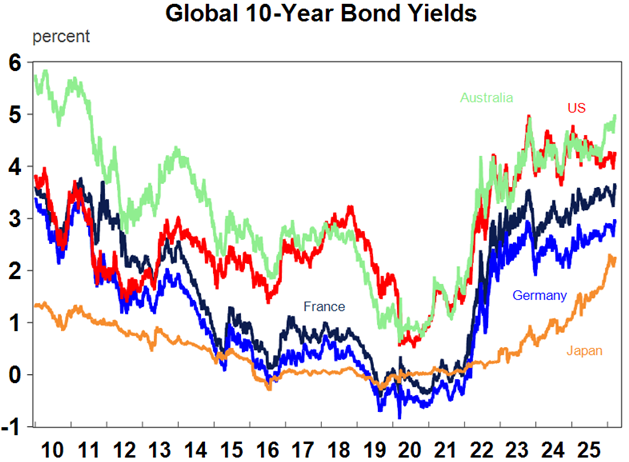

10-year bond yields rose over the last week on rising inflation fears and are now around 5% in Australia which will add to Budget interest costs and fixed mortgage rates.

Source: Macrobond, AMP

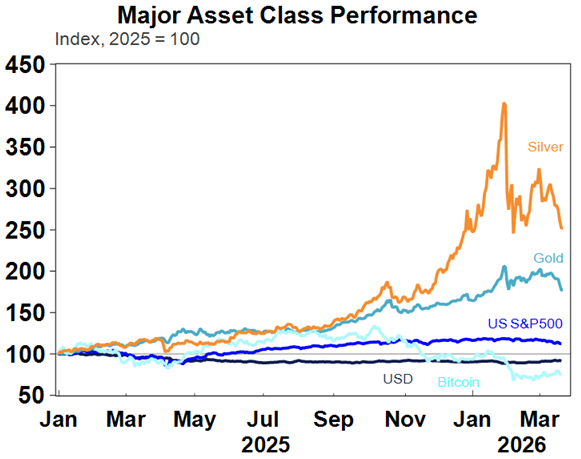

Gold and silver remained under pressure despite the geopolitical and inflation risks as excessive speculative positions were wound back and in response to expectations for higher interest rates. Bitcoin also fell. Iron ore prices rose but metal prices fell. The $A rose slightly as the $US fell and it remains relatively resilient reflecting ongoing expectations for RBA rate hikes at a time when the Fed is still expected to cut, albeit by less than before the War.

Source: Macrobond, AMP

Despite the hit to global oil supplies threatening to be the biggest on record the market reaction so far has been relatively mild. Global oil prices are up “just” 80% from their January low (compared to the three or four fold increases of the 1970’s oil shocks) and US shares have only fallen 7% and the Australian share market has had a fall of around 8% – both of which would count as a mild correction. So maybe the markets know something. There are several reasons for the mild reaction (so far):

- The experience of the last year has been that a shock and awe event (Liberation Day tariffs, ICE raids in Minneapolis, attacks on the Fed, the threats around Greenland, etc) are followed by a backdown or moderation. So, market still expect another TACO.

- Similarly, Trump’s military adventures (Nigeria, Venezuela) have been targeted and brief.

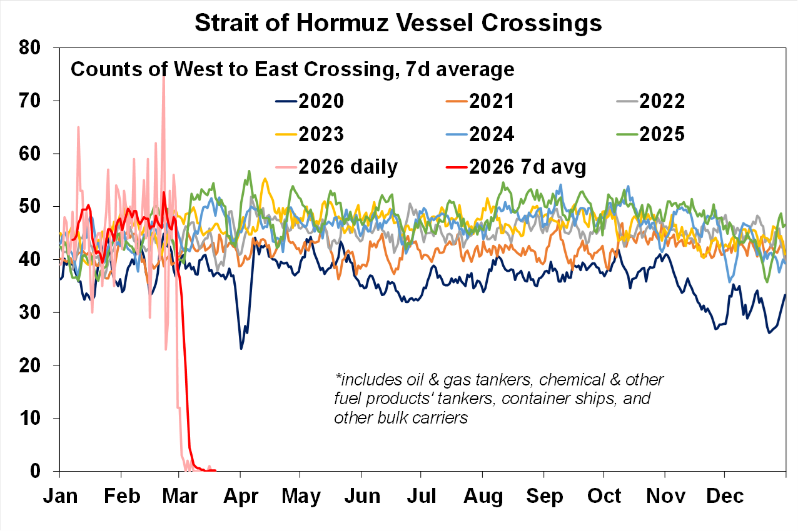

- There is hope the hit to supply flowing from the effective closure of the Strait of Hormuz will be overcome or by-passed in various ways (naval escorts, IEA reserve releases, Iran letting some ships through, etc).

- And finally, Trump is regularly using jawboning to head off a market meltdown – the War will be over “pretty soon”, the Iranian military is being “literally obliterated”, “we are getting very close to meeting our objectives”, oil prices will see a “sharp fall” when it’s over, etc. He did it again on Friday night. And this may be helping put a lid on investor fears – so far. Nixon, Carter and Bush senior never had Trump’s ability to bamboozle!

Some or all of these may be true to varying degrees. And Trump has a huge incentive to do a TACO with the War being unpopular, increasing odds he will lose the Senate as well as the House in the midterms, & increasing objections from MAGA supporters over his waging of another war. Losing the House would be normal in a midterm election for the president’s party, but losing the Senate would be a huge win for the Democrats as all four GOP Senate seats up for election are in safe Republican states.

Source: Bloomberg, AMP

But at this point it looks like the War has further to go and so oil prices could still go a lot higher before they start sustainably falling even if the War is relatively short. Aerial campaigns don’t have a great track record of success and reports indicate that the Iranian leadership is digging in and getting more hardened in resistance to the US. And the Pentagon has reportedly asked Congress for $US200bn to fund the War suggesting it has a way to go yet with now talk of using troops. So much for Trump’s hope (or was it a plan?) for a re-run of the Venezuelan model. Despite Trump’s latest bravado about considering “winding down” it may now be hard for the US to simply declare victory in relation to some of its narrower military objectives (like wiping out the navy, missiles and nuclear capability) and then simply withdraw as Iran may still have an ability to cause havoc including with the Strait of Hormuz. Even though Trump is now implying it’s the responsibility of other countries to reopen the Strait because the US does not use it, it’s closure is boosting oil product prices in the US just as in other countries. And while there are various workarounds to the Strait blockage of around 20 million barrels of oil a day, or 20% of global supplies, these won’t make up for all of the loss:

- The IEA reserve release is likely to be only around 3% of pre-War global oil consumption a day;

- Easing Russian sanctions may cover 1.5% at most;

- Allowing the sale of oil on stranded Iranian ships will provide only temporary relief;

- Allowing ships from China, India and Pakistan to pass will provide around 7.5%;

- And maybe an extra 2% or so can go through Saudi and UAE pipelines that by-pass the Strait.

But that still leaves a shortfall greater than the 5% supply hit from the second oil crisis in 1979. And the steady destruction of energy (mainly gas) infrastructure in Iran and surrounding countries means it will take longer to get supply back to normal once the War ends. And its also worth noting that past oil shocks unfolded over many months in terms of the rise in oil prices as the full impact became clearer – it was over about 4 months in 1973 and a year in 1979. So far, it’s still early days.

On a more optimistic note, reports that Iran will allow Japanese related vessels to pass through the Strait could be a good sign as Japan accounts for around 3% of global oil consumption. That said, reports of allowing Chinese, Indian and Pakistani ships to pass through a week ago still only saw a trickle of ships go through. Furthermore, details are lacking and it’s quite possible that it will involve Iran charging a fee which the US may not be happy with as it will give Iran the upper hand over the US in ensuring global energy security for a period.

Our base case is that the War and oil supply shock will be relatively short. Iran will not be able to keep the Strait closed indefinitely as it continues to see its military capability degraded, the US will eventually turn to naval escorts (albeit they are problematic) and or look for some sort of off ramp as the political pressure mounts. But it could still go on for many weeks yet and so could still see oil prices rise a lot further in the interim say to $US150 as the risks of a longer War and threat to oil supplies (oil to $US200) escalate.

The key things to watch out for will be a sustained fall in missiles & drones coming from Iran, increasing numbers of ships through the Strait of Hormuz, indications Iran wants to negotiate and another sharp rise in oil prices and a 10% or more fall in US shares which will increase pressure on Trump to find a way out.

Source: Bloomberg, AMP

Given Australia’s vulnerability as it imports 80-90% of its oil products it should be moving to cut back on demand now to add to our stockpile. So far the supply of fuel coming to Australia has not been disrupted according to the Government but there is a high risk it will be as some of our supplying countries impose bans on exports the longer the War continues, like China has. So, just as other countries are already starting to do, we should be moving now to curtail demand in ways that are least disruptive to business – like encouraging or allowing workers who can to work from home, encouraging more reliance on public transport, encouraging people and businesses to avoid non-essential air travel and encouraging greater use of E10 fuel. The longer we leave it the greater the risk of real disruption.

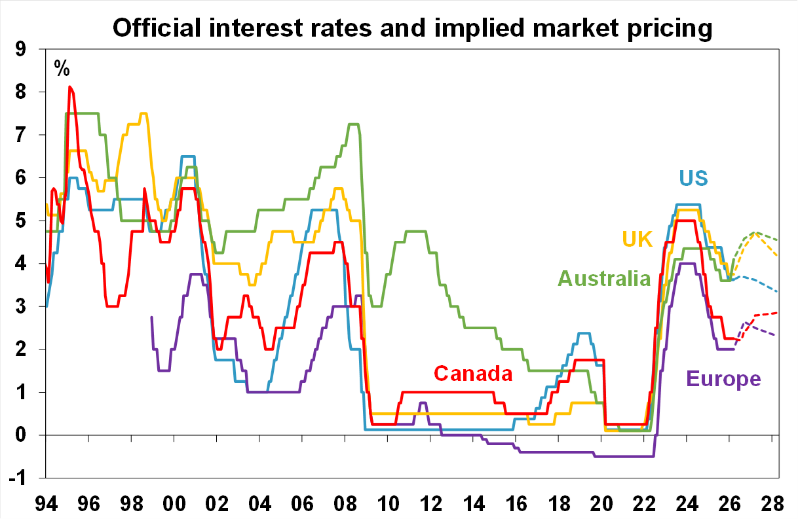

Central bank caution prevailed with the Fed, ECB, Bank of Canada, Bank of Japan, Bank of England and the Swiss and Swedish central banks all leaving rates on hold amidst the uncertainty and two-way risks – upside to inflation and downside to activity – flowing from the War. However, there was some shift in a less dovish direction, consistent with money market moves leading a higher profile for policy rates since the War began. The outlook for rates has become less favourable as central banks will fret about a flow on to underlying inflation and inflation expectations. The Bank of England notably lurched from dovish to hawkish and the Bank of Japan kept prospects for an April hike live.

Source: Bloomberg, AMP

But bucking the global response, the RBA hiked again, citing inflation already above target thanks partly due to capacity constraints and sharply higher fuel prices thanks to the War tilting the inflation risks to the upside including for inflation expectations. These concerns are understandable and the RBA arguably had less flexibility than the other central banks because depending on the country being compared to inflation is further above target here, productivity is weaker and there is less spare capacity in the economy. While money market expectations for most central banks policy rates have shifted higher this is more noticeable in Australia with the money market expecting nearly another three rate hikes this year.

We are now forecasting one more RBA rate hike in May. The RBA is clearly worried about the boost to already high inflation and higher inflation expectations than the hit to growth and March quarter inflation data will show a sharp spike in inflation if petrol prices stay at current levels. Governor Bullock’s press conference comments appeared to indicate a preparedness to risk a recession if necessary to get inflation back to target. Current petrol prices if sustained mean a whopping 1.4% boost to inflation taking it well above 5%. However, it is a close call with the 5/4 Board vote in favour of hiking versus holding suggesting that some board members are a bit wary of tightening and there is a chance that the War will have ended by the next meeting seeing oil prices starting to fall.

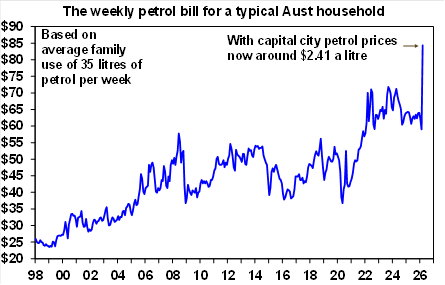

Rate hikes will compound the hit to growth and the risk of recession. The negative impact on growth from higher fuel prices on disposable income and possible fuel shortages necessitating rationing will become increasingly apparent in the months in the months ahead. Current capital city petrol prices of around $2.41 a litre imply a $108 a month rise in the petrol bill for an average household if sustained. Taken together with higher mortgage interest payments from the two rate hikes so far this means a hit to the spending power of households with a mortgage and a petrol car in excess of $300 a month. And don’t forget that mortgage holders are far more sensitive in their spending to changes in their disposable income than those who have paid off their mortgage. Depending on how long the disruption lasts the hit to activity could knock 1 percentage point of economic growth and push the economy back into a per capita recession. We expect that the RBA will be cutting rates again in 2027 as slumping economic activity eventually drives lower inflation.

Source: Bloomberg, MotorMouth, AMP

The best way the Government can help reduce inflation pressures and respond to the War is to cut Government spending and help boost productivity. This would provide more room for private spending and at the same time expand the capacity of the economy to grow without boosting prices. So, it’s very good news to see the Treasurer acknowledging the key problems around inflation and productivity and confirming that the Budget will contain three reform packages: “substantial” budget savings; “a sustained and substantial effort” to boost productivity; and “tax reform to drive more productive investment” and improve budget sustainability and equity – all with a “supply side emphasis”. The key is that government spending is cut in real terms such that Federal Government spending falls back to 25% of GDP or less in the forward estimates, that the productivity reforms be hard-nosed and broad based and that tax reform be more than just a cut to the capital gains tax discount or restrictions on negative gearing – otherwise it will just be a tax hike. The Treasurer is saying the right stuff so hopefully words are turned into action in May and it’s not overtaken by political timidity in the face of the War as now is the time to make hard decisions before the focus shifts back to handouts before the next election.

Major global economic events and implications

US economic data was mixed. Industrial production rose by more than expected in February and the Philadelphia regional manufacturing conditions index for March rose, but the New York index fell. Home building conditions rose in March but remain weak, along with home sales and housing starts. Initial jobless claims remained low as usual though. Meanwhile, producer price inflation rose in February but key components that flow through to core PCE inflation imply that it will slow to 3%yoy from 3.1%.

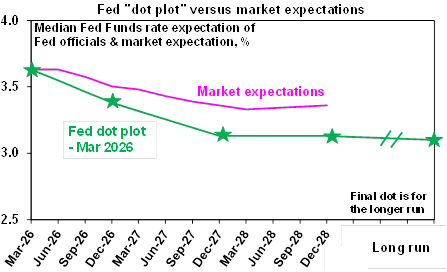

The Fed left rates on hold at 3.5-3.75% as it remains in wait and see mode and noted the uncertain impact of the Iran War with risks to inflation and growth. It still sees another rate cut this year and next, but Powell noted that will require inflation to fall. Interestingly there is now only one dissent in favour of a rate cut (Miran and only now for a -0.25% cut). With tariffs and now War set to add to inflation Trump appears to have blown his push for much lower rates with even his Fed appointees backing away.

Source: Bloomberg, AMP

Canadian inflation fell more than expected in February with core measures at 2.3%yoy but the BoC stayed on hold citing “acute” uncertainty flowing from the Iran War.

It was the same story at the Bank of Japan, the ECB, Bank of England and Swiss & Swedish central banks – all leaving rates on hold but as noted earlier the outlook is now more hawkish with money markets pricing in rate hikes for all major developed country central banks this year except the Fed.

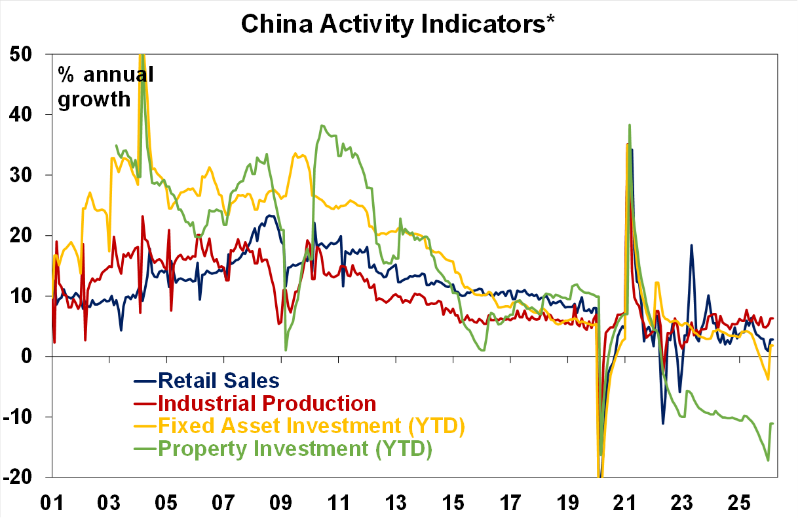

Chinese economic activity had a strong start to the year. Growth in retail sales, industrial production and investment for January and February came in well up from December. That said, retail sales and investment are still soft and property prices, sales and investment are still falling.

Source: Bloomberg, AMP

Australia economic events and implications

February jobs data was messy, but its ancient history anyway. Employment rose by a stronger than expected 48,900 jobs but full-time employment actually fell by 30,500, hours worked fell and unemployment rose to 4.3% as the participation rate rose. The ABS noted that this February saw less people moving into employment and more into part time employment compared to recent Februarys. This may all be a sign of some slowing in the jobs market but jobs data can be very noisy month to month and the RBA would probably still characterise the jobs market as slightly tight anyway. That said it’s all ancient history if the oil supply disruption continues for more than another month as it will start to depress spending and economic activity and hence jobs in the economy.

Source: Bloomberg, AMP

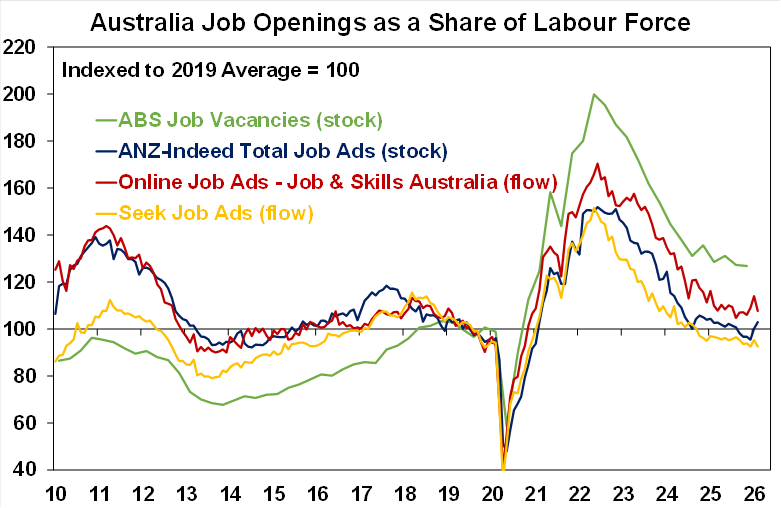

Job vacancies had been showing signs of stabilisation after a sharp fall pointing to still okay jobs growth – but they will be key to watch for signs of the impact from the War.

Source: ABS, AMP

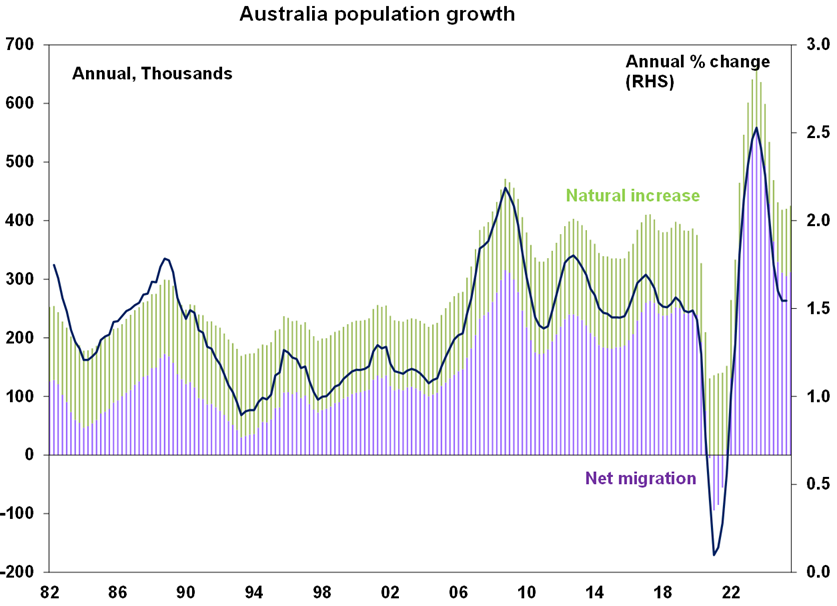

Population growth in the September quarter last year remained around 1.6%yoy, with net migration of 311,000 people making up about three quarters of the rise. Treasury reportedly now see net migration remaining around this level, whereas in the Midyear budget update they saw it slowing to 260,000 people this financial year and then to 225,000 next year. In the absence of a quick pick up in home building this means the housing shortfall of 200,000-300,000 will remain for some time to come. Meanwhile, interstate migration out of NSW and into Queensland is slowing rapidly and will likely lead to slower relative home price growth in Queensland.

Source: ABS, AMP

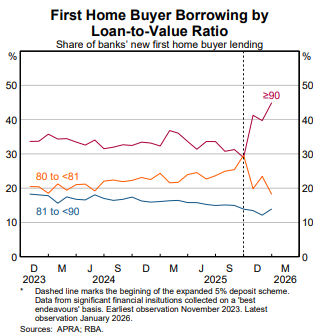

The RBA’s six-monthly Financial Stability Review noted that the Iran War coming at a time of increased leverage and concentration risk in global asset markets and low risk premia has increased the potential for a disorderly repricing of assets but that the Australian financial system had a good degree of resilience. It noted Australian banks are well capitalised and have prudent lending standards and that non-performing loans remain low. This includes for housing loans where arrears are low and the vast majority of borrowers have sufficient income to cover mortgage payments and expenses with most borrowers having large buffers that can help withstand shocks. The FSR does highlight the pickup in high loan to value loans for first home buyers on the back of the 5% deposit scheme. This may be helping buyers get in earlier but apart from pushing prices up its also leading to increased risk for such buyers.

What to watch over the next week?

Obviously, the Iran War will remain the main focus for investors but on the data front, developed country business conditions PMIs for March to be released Tuesday are likely to show the initial impact of the hit to growth from the War.

In Australia, we expect February CPI data (Wednesday) to show a 0.1%mom rise or 3.8%yoy, unchanged from January. Expect fuel prices to have fallen but increases in education, housing transport fares. Trimmed mean inflation is expected to be 0.3%mom or 3.4%yoy, which is also unchanged from January. Of course, a sharp spike in headline inflation is expected for March on the back of the Iran War with the rise in fuel prices expected to add around 1% to headline CPI inflation.

Outlook for investment markets

Global and Australian share markets are at high risk of further falls in the near term in response to the War with Iran against the backdrop of stretched valuations, political uncertainty associated with Trump & the midterm elections, increasing worries about private credit and AI & tech valuation worries. We continue to see a 15% or so top to bottom fall in share markets along the way this year, but the risk is that it could go deeper the longer the Strait of Hormuz remains effectively closed. However, returns should still be positive for the year as a whole thanks to Fed rate cuts likely later in the year, Trump still likely to pivot to consumer friendly policies ahead of the midterms and solid profit growth.

Bonds are likely to provide returns around running yield.

Unlisted commercial property returns are likely to be solid helped by strong demand for industrial property associated with data centres.

Australian home price growth is likely to slow to 5% or less due to poor affordability and the RBA raising rates with talk of more to come.

Cash and bank deposits are expected to provide returns around 4.25%.

The $A is likely to rise as the interest rate differential in favour of Australia widens as the Fed cuts and the RBA hikes. Fair value for the $A is around $US0.72.

Eurozone shares fell 1.9% on Friday and the US S&P 500 fell 1.5% on reports that the US is considering using troops to take over Iran’s Kharg Island oil exporting facility and worries this will cause a further escalation in the War. Reflecting the poor global lead ASX 200 futures fell 156 points, or 1.8%, pointing to further falls in the Australian share market on Monday, although this could be affected by developments in the War and oil flows through the Strait of Hormuz over the weekend.