Dr Shane Oliver, Head of Investment Strategy & Chief Economist at AMP, discusses developments in investment markets over the past week, economic activity trackers, major global economic events and Australian economic events.

Investment markets and key developments

Global share markets were mixed over the last week. US shares were whacked by ongoing tariff uncertainty and this also weighed on Japanese shares. But Eurozone shares rose on the back of likely fiscal stimulus in Germany and another ECB rate cut and Chinese shares were also buoyed by news of more stimulus. Australian shares fell around another 2.7% taking the ASX 200 back below the 8000 level as tariff announcements out of the US added to uncertainty. The falls were led by energy, financial and consumer shares. Eurozone bond yields rose around 40 basis points on the back of a likely big fiscal easing in Germany and this pulled up yields in the US, Japan and Australia. Prospects for more fiscal stimulus in Europe pulled up the Euro and pushed down US dollar. This in turn saw the $A, metal prices and gold prices rise. Oil prices fell though on global growth concerns and the iron ore price also fell. Interestingly, the global policy moves with tariffs in the US and stimulus in Europe have seen US shares and the US dollar give up all their gains since the US election in November whereas Eurozone shares are at record highs. Australian shares and the $A are just getting buffeted by all the global policy uncertainty.

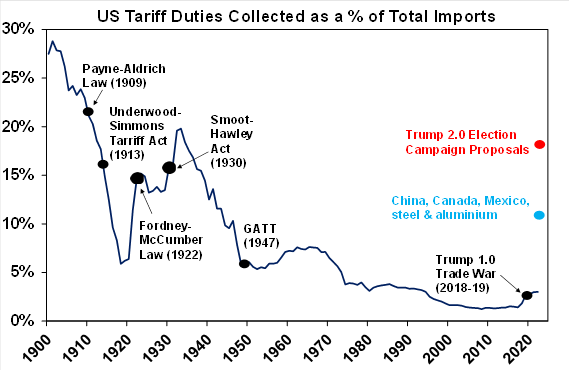

The past week has seen another round of erratic tariff announcements from Trump with: an extra 10% tariff on imports from China (taking it to well above 30%); the 25% tariffs on Canada (10% on oil) and Mexico starting on Tuesday only to see a delay till 2nd April for autos announced on Wednesday and then a delay again till 2nd April for all goods covered by the USMCA “free trade” deal (which is around half or a bit more of their exports); and Trump announcing an investigation into lumber imports and plans to put tariffs on agricultural imports on 2nd April. And then there are the tariffs on steel and aluminium to start in the week ahead and plans for reciprocal tariffs, tariffs on the EU and tariffs on various industries (semi conductors, autos, pharmaceuticals, copper, etc) set to start from 2nd April. So 2nd April looks like being the big day and its kind of looking like the Canadian and Mexican tariffs will get rolled into broader announcements then around “reciprocal tariffs” and various industry tariffs. Trying to make sense of all this and work out the end point for the tariffs is guess work as Trump’s motivation seems to vary wildly – eg the flow of people and fentanyl were given as the reason for the tariffs on Canada and Mexico but they have already moved on that and yet he has told auto makers not to come back for another extension as he wants production to be in the US and more broadly he is focussed on the rest of the world “ripping us off”. The tariffs on Mexico and Canada, assuming they do go ahead on 2nd April, along with those on China and steel and aluminium in the next week will take the average effective tariff rate on imports to the US to around 11.5%, up from 3% in January and its highest since the early 1940s. And Trump isn’t finished yet.

Source: US ITC; EvercoreISI; AMP

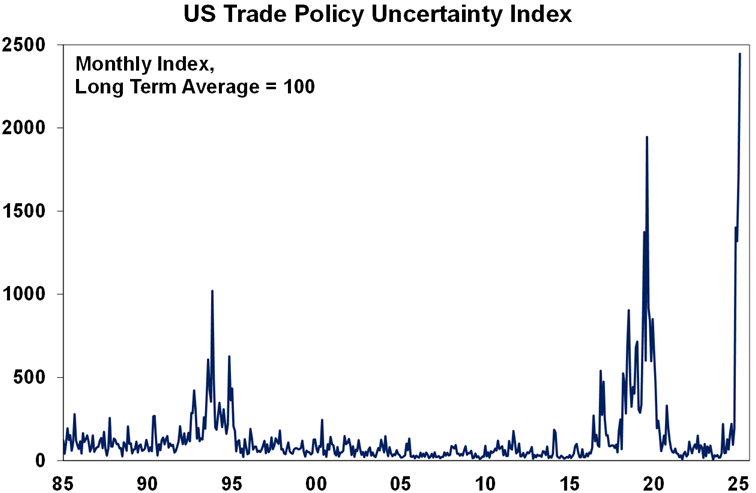

Trump’s chaotic policy making will come with a cost to the US economy and global growth. Rough estimates suggest that the tariffs on China, Canada and Mexico will directly knock around 0.5% off US and Chinese GDP and more off Canada and Mexico. They could also add around 0.7% to US inflation this year resulting in the Fed keeping rates higher for longer. But as noted there is more to go. More broadly, Trump’s erratic and inconsistent policy making with no certainty as to the end point on tariffs, uncertainty flowing for Musk’s DOGE cuts to the Federal workforce and service delivery and geopolitical uncertainty with Trump seeming to side more with Russia than allies like Europe, Canada and Mexico all risk a broader hit to the US economy as consumers and businesses curtail spending in the face of policy uncertainty. As can be seen in the next chart US trade policy uncertainty is exploding.

Source: Baker, Bloom & Davis, Bloomberg, AMP

Increasing uncertainty risks pushing shares even lower. So far US shares have had a 6.6% fall from their recent record highs, global shares 5.1% and Australian shares 7%. The problem is that price to earnings multiples for US and to a lesser extent global and Australian shares remain high and the risk premium shares offer over bonds (as proxied by the gap between the earnings yield and bond yield) is low. In the face of ongoing Trump driven policy uncertainty with a flow on to economic conditions this means a high risk of a further likely volatile correction in shares. Of course, at some point economic weakness and its impact on poll support for Trump and Republican politicians along with share market falls – with Trump seeing share gains as a key performance indicator – will put pressure on Trump to reverse course and focus on more positive policies. But Trump’s acknowledgement that his policies will cause “a little disturbance, but we’re ok with that” and Treasury Secretary Bessent’s comment about 6-12 months of pain suggest that we may have a way to go yet. So, we continue to see a high likelihood of a 15% plus correction in shares before more positive forces around Trump’s tax cuts and deregulation and more Fed rate cuts get the upper hand.

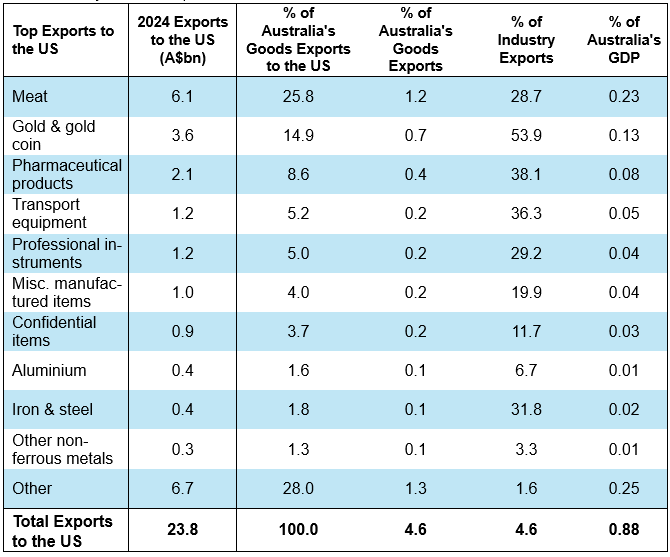

It’s hard to see how Australia won’t face some direct tariffs on our exports to the US. Even if we avoid the 25% tariff on our steel and aluminium exports (which is looking questionable) we likely face tariffs on our pharmaceutical exports (which are more than double the value of our steel and aluminium exports to the US) or meat (which is our biggest export – and he is saying he will tariff agriculture from 2nd April) or more broadly via his reciprocal tariffs where he could take a dislike to lots of things like to the GST (which would be totally irrational but then…) or that we like Aussie Rules and rugby and not gridiron. The key to remember though is that compared to other countries we are a small exporter to the US with a total value of $24bn worth last year or 0.9% of our GDP. That is similar to the value of Australian exports China restricted in 2020 with little impact on the macro economy. The main threat to Australia by far comes from Trump’s trade war leading to a hit to global trade and growth leading to less demand for our exports.

Australian exports to the US as a share of GDP

Source: ABS, AMP

Trump’s establishment a US crypto reserve fund with Bitcoin, Ethereum, Solana and some others like ADA and XRP lacks any economic justification. Reserves are normally set up – say with oil, grains or commonly accepted foreign exchange – if there is a risk that a country may run out of what’s in the reserve for a period which could cause economic disruption. But how is this the case with crypto currencies? Fortunately, Trump’s crypto czar David Sacks has indicated that scarce taxpayer money – for which there are better uses given the US’ huge budget deficit – would not be used but it would be capitalised with Bitcoin already held as a result of criminal or civil actions.

Making the rest of the world greater again! The news over the last week wasn’t all negative though with lots of stimulus in Europe and more in China.

- Germany’s centrist political parties agreed to relax the brake on public debt by setting up a 500bn Euro fund for infrastructure investment and allowing open ended borrowing for defence. This suggests a big boost to German economic growth. That said it still needs support from the Greens to pass the current Bundestag in the next two weeks.

- European leaders are working on a plan to mobilise nearly 800bn Euro in defence spending. Defence spending is not the best of use of public money – but at least it will provide a stimulus to growth.

- This is coming as the European Central Bank cut its policy rates by another 0.25%, with its deposit rate now at 2.5%, and retained dovish guidance albeit President Lagarde noted “huge” uncertainty and that it will be more data dependent.

Source: Bloomberg, AMP

- China’s National Peoples’s Congress has set a growth target of “around 5%” again for this year and with a budget deficit target of 4% of GDP up from 3% in 2024. The fiscal stimulus included a doubling in subsidies for consumers trading in goods. The extra stimulus in combination with the 5% growth target suggests the Government is prepared to provide more stimulus to offset the negative impact of Trump’s tariffs in order to maintain economic growth.

And in Australia GDP growth picked up late last year. December quarter GDP rose to 0.6%qoq or 1.3%yoy. This is the fastest in two years and per capita GDP rose for the first time in two years. It suggests the worst may be over for Australian growth. However, it’s not quite as good as it appears: per capita GDP has had just a small uptick; inventories and trade contributed roughly half of the 0.6%qoq growth and they are both very volatile; public spending is continuing to boom up 1%qoq or 5.5%yoy and accounted for 0.2 percentage points of growth; and private final demand remains pretty subdued up just 0.4%qoq or 0.8%yoy with consumer spending potentially exaggerated by higher levels of sales and sports music/events than normal.

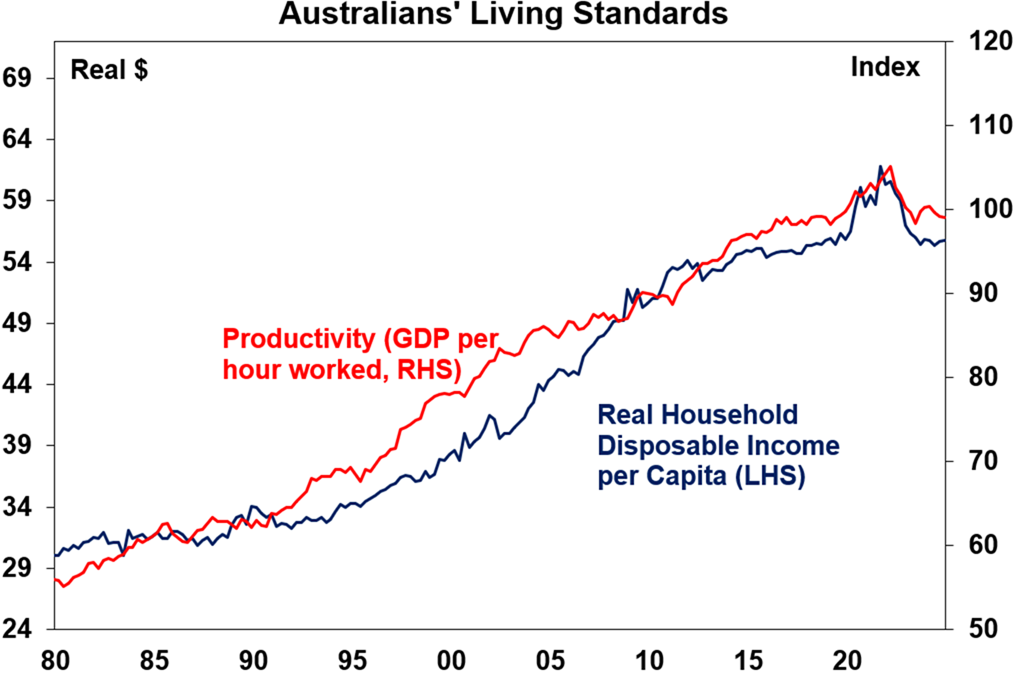

In terms of the “cost-of-living” crisis in Australia the good news is that real household disposable income per person is rising again helped by tax cuts wages growth running above inflation. But so far its just a flick off the bottom and remains around 10% down from its 2021-22 high. Admittedly the high was distorted by things like Job Keeper but even ignoring that, there’s been little growth in real disposable income per capita over the last decade.

Source: ABS, AMP

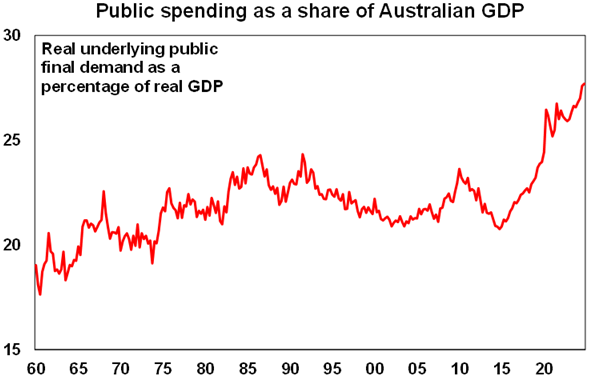

The key to sustainably improving living standards lies in boosting productivity growth which remained negative in the March quarter with a fall of 1.2% over the last year. This means tax reform, deregulation and a whole bunch of other things to help boost the supply side of the economy. A good place to start would be to put a cap on public spending as a share of GDP as it crowds out more productive private sector activity. It’s now reached a new record high of 28% of GDP. And with the surge in public spending has come a surge in public sector employment which rose a whopping 7.3%yoy which in turn is crowding out more productive private sector employment. The key is to get the balance right. But it’s hard to see much of a focus on this in the upcoming election as most productivity enhancing reforms are not vote winners.

Source: ABS, AMP

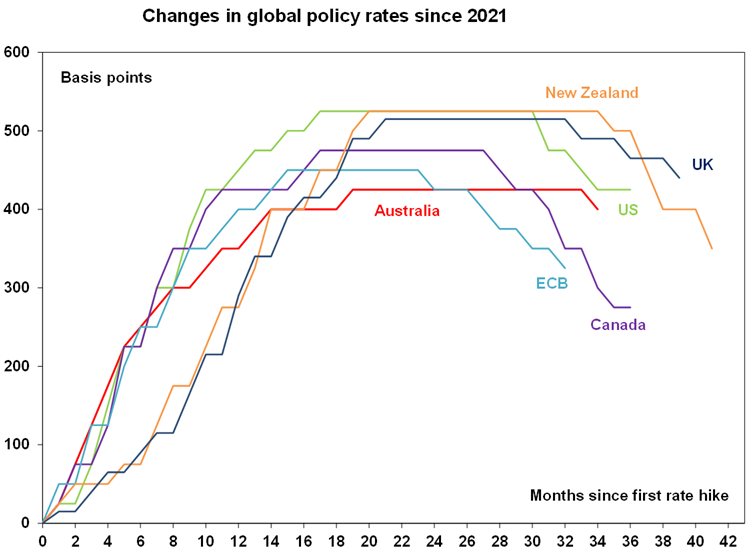

We still see the RBA pausing in April and cutting again in May. The minutes from the RBA’s last meeting and comments by Deputy Governor Hauser reiterated the cautiousness expressed two weeks ago by Governor Bullock particularly around the labour market remaining tight and that easing in line with market expectations would see underlying inflation settle above 2.5%yoy. Stronger GDP in the December quarter than the RBA expected may be seen as adding to this caution. However, with private demand growth remaining weak and inflation likely to come in slightly weaker than expected we continue to see two more RBA rate cuts this year, in May and August.

The economics of cyclones. My thoughts are with those being impacted by Cyclone Alfred. Attention at some point will naturally turn to its economic impact which is likely to be significant as over 4 million people, or just over 15% of Australia’s population, live in Southeast Queensland and northern NSW. Apart from some short-term disruption the impact on GDP is likely to be minor and slightly positive if anything because of clean up and rebuilding activity. But the real negative impact is the human cost, the potential loss of wealth caused by damage to property which could run into billions of dollars and a boost to inflation. It is through higher inflation that most Australians could feel the impact from Alfred and here the main threat is to fruit and vegetable prices (recall the banana effect from Cyclone Yasi) and yet another boost to insurance premiums. This is unlikely to impact what the RBA does with interest rates though as it will focus on underlying inflation which will strip out any extreme moves higher in things like fruit and vegetable prices or insurance premiums.

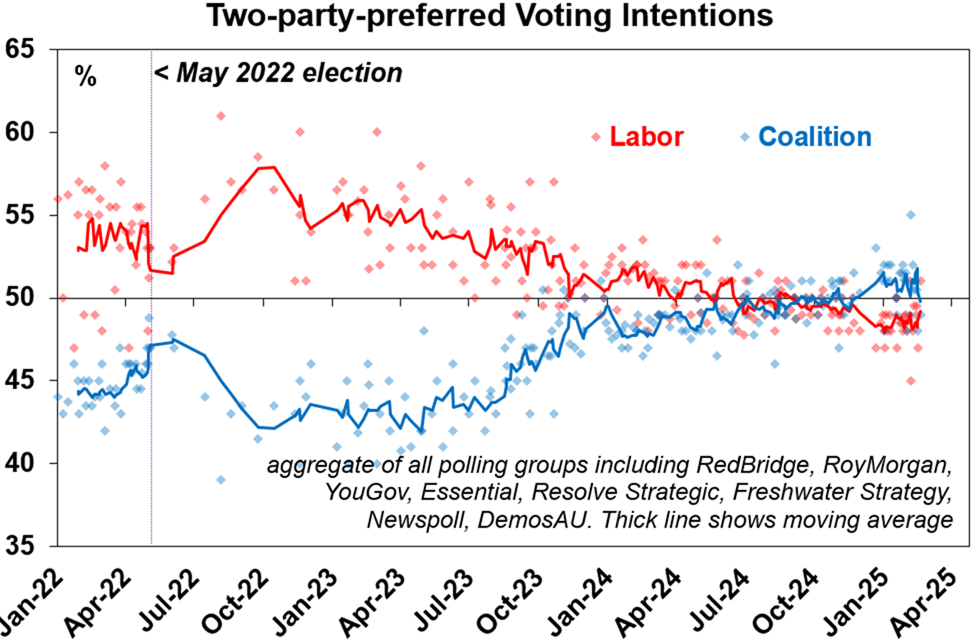

The next Australian federal election is due by 17 May. Labor is trailing in two party preferred polling averages although the gap may be narrowing with a YouGov poll having Labor ahead. Current polling suggests both parties may struggle to get a 76 seat majority raising the prospect of a hung parliament. The ALP currently has 78 seats and could easily lose three seeing it lose its majority, whereas the LNP gaining the 22 seats needed for a majority is a big ask. The main issue is the “cost of living” which has been exacerbated by excessive public spending. So far its not clear either side has fully learned the lesson from this although the LNP appears more focussed on constraining spending.

Source: Polls as indicated, AMP

Major global economic events and implications

US economic data continues to show the impact of tariff and policy uncertainty coming out of the Trump administration. The ISM business conditions indexes were mixed – down for manufacturing but up for services – with both showing higher prices and respondents comments referring to the impact of tariffs. The Fed’s Beige Book of anecdotal evidence also pointed to growing tariff driven uncertainty. Initial jobless claims fell but continuing claims rose again, and the Challenger survey showed a sharp spike in layoffs largely reflecting public workers. The Atlanta Fed’s GDPNow estimate of current quarter GDP growth fell to -2.4% annualised which will add to fears of recession but its worth highlighting that its mainly being driven by a surge in imports which looks to be front running tariffs. In good news though productivity growth was revised up to 2%yoy with the result that growth in unit labour costs is at 2%yoy consistent with the Fed’s inflation target.

In Japan, union wage demand heading into the annual Shunto wage negotiations average 6.1% which is up from 5.85% last year and adds to signs that wages growth has durably picked up.

Eurozone inflation fell to 2.4%yoy in February with core inflation falling to 2.6%yoy. Both were slightly higher than expected but remain consistent with further ECB rate cuts. Meanwhile unemployment was unchanged at 6.2% in January.

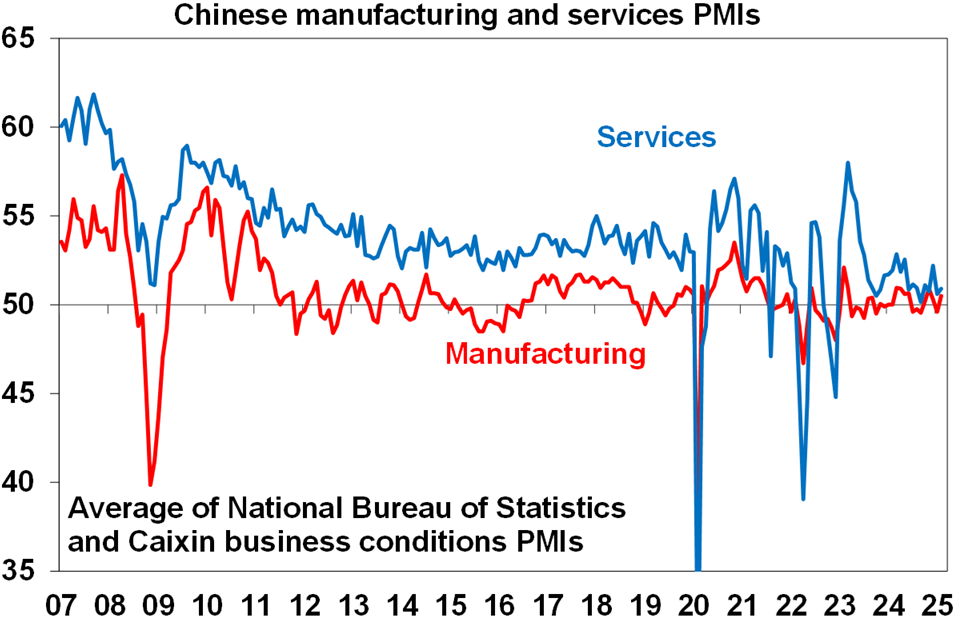

Chinese business conditions PMIs rose slightly in February after the earlier than usual Lunar New Year depressed them in January. They still remain relatively soft. Meanwhile Chinese export growth slowed to just 2.3%yoy in January and February & imports fell 8.4%yoy consistent with weak domestic demand growth.

Source: Bloomberg, AMP

Australia economic events and implications

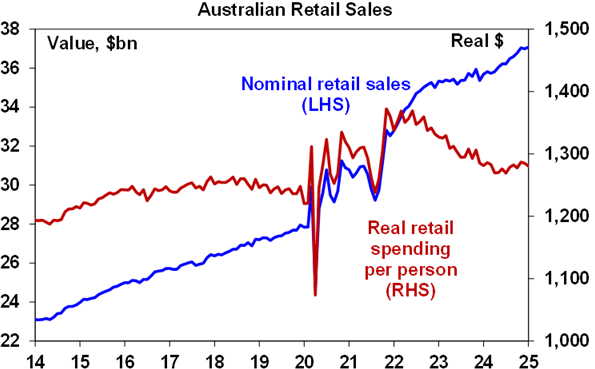

Apart from the pick-up in GDP growth, other Australian economic data was mostly positive. January retail sales rose 0.3% and are up 3.8%yoy suggesting a gradual improving trend with tax cuts and rate cuts providing support. However, the rise was narrowly based around food and hospitality which was boosted by strong attendance at outdoor events. Related to this the ABS’ household spending indicator slowed in January to 2.9%yoy with weaker discretionary spending after a boost from discounting and a return to reliance on spending on essentials to maintain growth. In other words, underlying consumer spending growth still looks like it will remain sluggish in the absence of more rate cuts.

Source: ABS, AMP

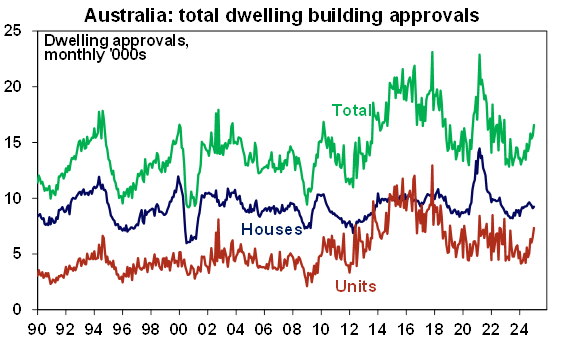

Building approvals surged 6.3% in February driven mainly by a 12.8% rise in unit approvals. Unit approvals are very volatile but its clear the trend is now up and lower interest rates should help this over time. Approvals are currently running around 190,000 a year which is below the Housing Accord objective of 240,000 dwellings a year – but at least they are going in the right direction and if we are to meet the objective it has to come from more units.

Source: ABS, AMP

The trade balance improved to $5.6bn helped by a rise in exports and a slight fall in imports. However, the rise in exports was mostly driven by a surge in non-monetary gold, particularly to the US where there was also a surge in pharmaceutical exports both of which look like front running ahead of Trump’s tariffs.

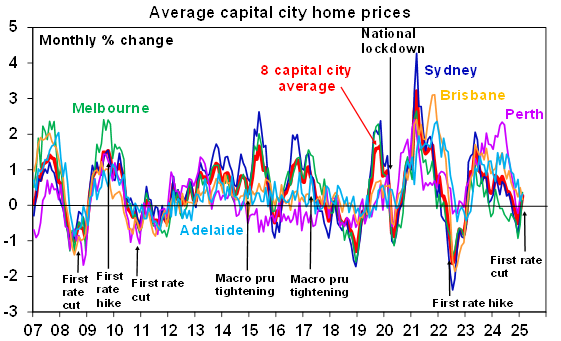

Home prices rose in February helped by all the talk about rate cuts. Rate cuts against the backdrop of the ongoing housing shortage are likely to drive further gains this year but the upswing is likely to be modest as affordability remains very poor, interest rates are only likely to fall modestly and population growth is slowing taking some pressure off the rental market.

Source: ABS, AMP

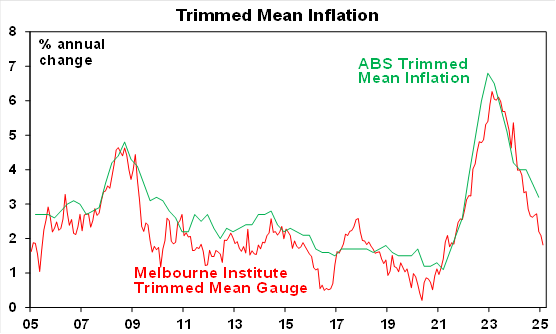

Finally, the Melbourne Institute’s Inflation Gauge for February fell to 2.2%yoy with trimmed mean inflation falling to just 1.8%yoy pointing to a further fall in the ABS’ measures of inflation.

Source: ABS, AMP

What to watch over the next week?

In the US, the 25% steel and aluminium tariffs are due to start on Wednesday and Congress needs to pass a continuing resolution by Friday to avoid a Federal Government shutdown. In terms of the latter the House Republicans can only afford to lose one GOP vote as the Democrats won’t provide support. If it fails it could be a long shutdown. Historically they have not had much impact on GDP or share markets, but this time could be different given the huge uncertainty swirling around Washington. Apart from this the focus will be back on inflation with February CPI data on Wednesday likely to show inflation remaining sticky at 0.3%mom or 3%yoy with core inflation also at 0.3%mom/3.2%yoy. Job openings data for January (Tuesday) are likely to show a further slowing and consumers’ inflation expectations data (Friday) will be watched for any further rise on the back of tariffs.

The Bank of Canada (Wednesday) is expected to cut its cash rate by another 0.25% taking it to 2.75%.

In Australia, the Westpac/MI consumer sentiment survey and NAB business conditions survey (Tuesday) will be watched for signs of any impact from the RBA’s first rate cut

Outlook for investment markets

After the double digit returns of 2023 and 2024, global and Australian shares are expected to return a far more constrained this year. Stretched valuations, the increasing risk of a US recession, Trump’s trade war and ongoing geopolitical issues will likely make for a volatile ride with a 15% plus correction somewhere along the way highly likely. But central banks, including the RBA, still cutting rates, prospects for stronger growth later in the year supporting profits, and Trump’s tax and deregulation policies ultimately supporting US shares, should still mean okay investment returns.

Bonds are likely to provide returns around running yield or a bit more, as inflation slows to target, and central banks cut rates.

Unlisted commercial property returns are likely to improve in 2025 as office prices have already had sharp falls in response to the lagged impact of high bond yields and working from home.

Australian home prices have likely started and upswing on the back of lower interest rates. But it’s likely to be modest given poor affordability. We see home prices rising around 3% in 2025.

Cash and bank deposits are expected to provide returns of around 4%, but they are likely to slow as the cash rate falls.

The $A is likely to be buffeted between changing perceptions as to how much the Fed will cut relative to the RBA, the negative impact of US tariffs and a potential global trade war and the potential positive of more decisive stimulus in China. This could leave it stuck between $US0.60 and $US0.70, but with the risk skewed to the downside as Trump ramps up tariffs.

Ends

Important note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.