by Kent Hargis and Sammy Suzuki – Co-Chief Investment Officers—Strategic Core Equities

During this period of economic uncertainty and market stress, investors may be surprised to discover how a strategy targeting stocks that lose less in a downturn can beat the market over time.

Most investors implicitly understand the concept of risk. The framework was famously laid out in the capital asset pricing model (CAPM) of the 1960s, which explained expected return as a function of both firm-specific risk and an asset’s sensitivity to the broader market. Fundamentally, however, it’s grounded in a simple concept: investors expect to be compensated for assuming more risk. If risk had no payoff, we’d all just keep our assets in cash and call it a day.

Relative vs. Absolute Risk in a Choppy Market

Too often, investment managers are consumed with relative risk—tracking their performance against a market-cap-weighted benchmark index. This can conflict with what really matters to investors—absolute performance and how well an investment addresses long-term financial goals.

The issue becomes especially thorny during bouts of market volatility. And lately, there’s been plenty of it.

Amid stubborn inflation and economic slowing this year, the stock market posted its worst first half since 1970, with the S&P 500 retreating by more than 20%. While stocks have recovered some of their losses in the third quarter, market choppiness has continued, as investors digest lowered earnings guidance and the prospects of additional monetary tightening.

This is where the rubber meets the road. It’s one thing to talk about sticking to a long-term investment plan but quite another to sit tight as your portfolio takes a drubbing.

Is It Possible to Realize Higher Returns with Less Volatility?

What if there were a way to generate long-term competitive returns without the need to endure extreme swings in volatility?

This would seem to contradict CAPM and the other maxims related to risk and return. But a growing body of research indicates that, with a carefully curated portfolio, investors can indeed assume less risk and still beat the market over time by investing in low-volatility stocks. By doing so, investors can gain confidence to stay invested in equities through turbulent times.

Low-volatility strategies can come in different forms. We believe an effective defensive strategy should be grounded in company fundamentals and focus on firms that exhibit characteristics of quality (consistent cash flows and measures of profitability like return on invested capital), stability (low volatility of returns relative to the market) and attractive pricing that make them less susceptible to wide market swings. We refer to this as the QSP universe. While companies in traditionally defensive sectors like consumer staples and utilities are good examples, the QSP universe includes firms with standout business models in every sector of the economy, which can be uncovered through fundamental research and thoughtful stock selection.

For example, companies that we call quality compounders have successful business models and sustainable earnings, backed by good capital stewardship and positive ESG behavior. Intangible assets such as brands, culture, research and development, and patents are also valuable features, particularly in times of stress. These attributes support compounding earnings gains from consistent growth drivers through market cycles.

Limiting the Ups and Downs Is Key

Companies like these can help low-volatility strategies limit downside capture—that is to say, exposure to falling markets—while still participating in market gains, but not fully. In the same way that climbing a hill is easier when you start halfway up, stocks that lose less in market downturns have less ground to regain when the market recovers. As a result, they’re better positioned to compound off those higher returns during subsequent rallies, resulting in better long-term performance.

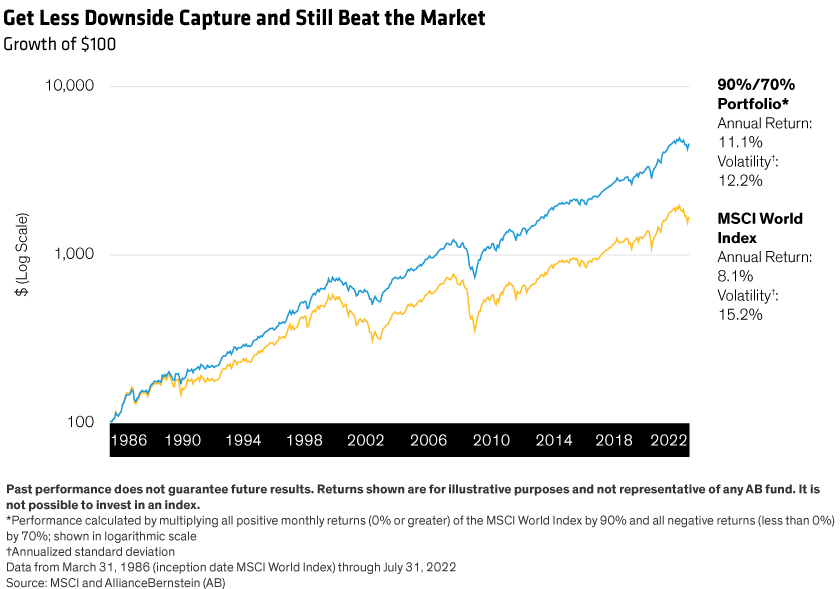

This concept can be illustrated by plotting a so-called 90%/70% portfolio against a global index of investment-grade stocks—in this case, the MSCI World Index (Display). This theoretical 90%/70% portfolio is so named because it would capture 90% of the market’s gains in rallies while falling only 70% as much as the market during downturns.

Using data from March 31, 1986 (index inception) through July 31, 2022, we found that our hypothetical 90%/70% portfolio would generate an annualized return three percentage points higher than the MSCI World Index over this period—with less volatility in the process.

But here’s the catch: to realize these long-term excess returns, investors would need to accept that a 90%/70% portfolio does not behave in the same way as the broader market.

That’s an easy pill to swallow when the market is whipsawing the way it has this year. After all, in market downturns, this low-volatility strategy would only expose investors to 70% of the market’s downside. The real test comes during rallies, when the 90%/70% would underperform the market. This is the price to be paid for market-beating long-term returns.

Putting Low Volatility to the Test: Recessions and Inflation

So how would a low-volatility QSP strategy fare in bear markets, or even recessions? While gross domestic product declined in both the first and second quarters of 2022—meeting the technical definition of a recession—economists differ as to whether the US is really in recession, particularly given strong consumer spending and historically low unemployment. Regardless, recessionary concerns remain.

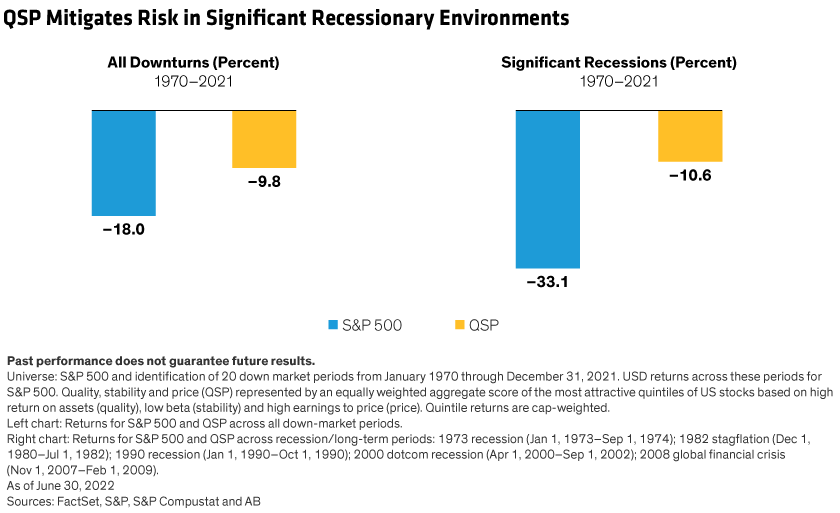

By identifying 20 market downturns between January 1970 through December 31, 2021 (Display), we found that S&P 500 stocks segregated into the highest quintile for QSP characteristics fared relatively well during market downturns. During significant recessions, the QSP portfolio did particularly well, outperforming the S&P 500 by more than 20 percentage points.

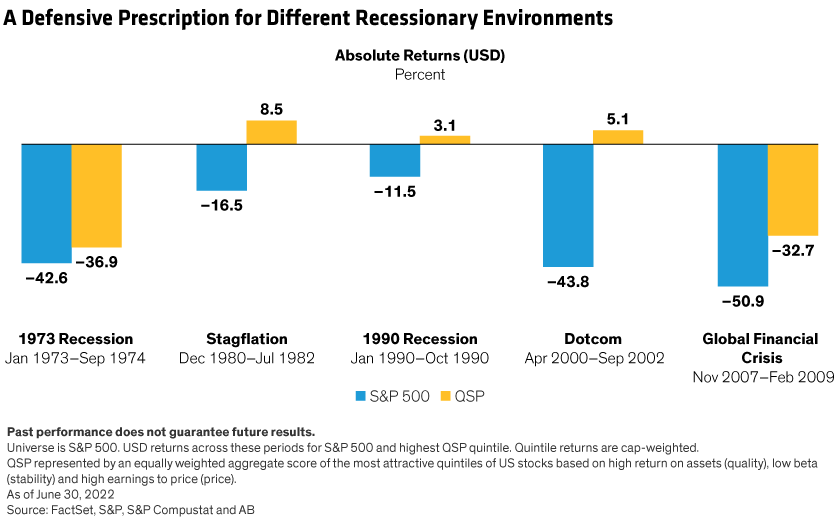

Looking closer at these deep recessions (Display), we can see that the top quintile of the S&P 500 based on quality, stability and price fell by 36.9% during the 1973–1974 recession triggered by the OPEC oil embargo—less than the S&P 500’s 42.6% decline. And during the recession of 1980–1982, QSP stocks actually gained 8.5%, while the market fell by 16.5%.

Performance was also strong during periods of rapidly rising prices. This is particularly prescient today, given that inflation reached a 40-year high in June, and the Fed’s inflation-fighting efforts have cast a pall over the financial markets.

Low-Volatility Strategies Can Be Tailored

In any market or macroeconomic environment, a low-volatility strategy can be paired with other active strategies to meet an investor’s individual risk tolerance, time horizon and investment goals. And while it’s not easy to construct a perfect 90%/70% portfolio, the main idea is to reduce exposure to market swings that can erode long-term returns.

Through fundamental research, we believe it’s possible to construct a portfolio of attractively valued companies with important indicators of quality and stability that can prosper in rallies, while withstanding periodic bouts of volatility. In times like these, a smoother ride may be just what investors need.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.