by Joe Foster – Portfolio Manager and Strategist

Gold: Holding up well

Gold prices averaged around US$1,837.20 per ounce in June, trading as high as US$1,871.60 on June 10 before closing at its monthly low of US$1,807.27 on June 30 (a 1.64% loss for the period). Inflation, the US Federal Reserve Bank (the “Fed”) and gold were, once again, central figures in June’s macroeconomic story, as the tug of war between all three remains contentious, yet balanced. Year-to-date, gold stands firmly, generating losses of only -1.2%, despite an approximately 20% loss in the S&P 500 Index, a 9.4% increase in the US Dollar Index (DXY Index)1and a doubling of 10-year US treasury yields.

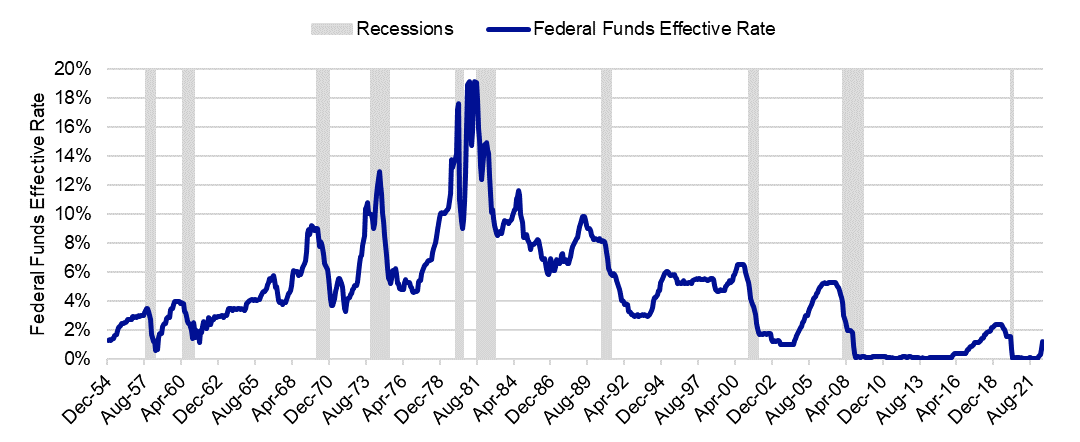

History’s lessons on rate hikes

While far from levels reached in August 2020, the price of gold has found support in the US$1,800 per ounce range. We believe this price reflects a benign economic outlook, where inflation starts to decelerate as the Fed increases its target fund rate and the economy does not go into a recession. While present conditions are different from those during previous rate hiking cycles, it is helpful to look back. One observation, as seen in the chart below, is that most rate hike cycles in the past have eventually driven the economy into a recession.

Figure 1: Rate hikes and recessions have typically gone hand-in-hand

Source: St. Louis Federal Reserve. Data as of May 31, 2022.

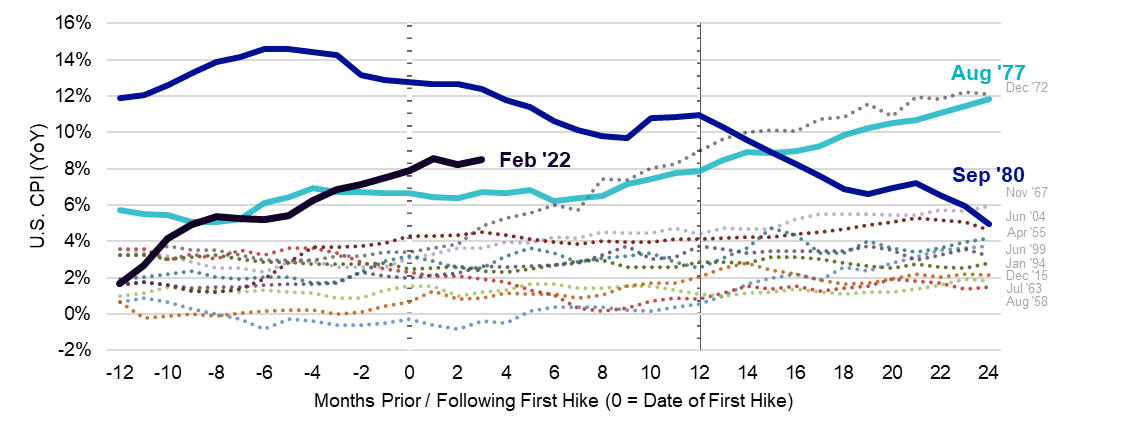

Another observation is that inflation is slow to respond to gradual increases in the Fed funds rate. The chart below shows the US Consumer Price Index (CPI)2before and after the beginning of the rate hiking cycles. The current cycle resembles the August 1977 to March 1980 cycle (Aug ’77 line), in terms of the levels of inflation at the start of the cycle. During that cycle, the Fed increased the funds rate from 6% to 20% in 31 months, hitting the brakes because of an economic recession, and all the while inflation just kept rising from about 6.5% to 14%. The one cycle that shows inflation coming down rapidly is the 1980 cycle (Sep ’80 line). In that cycle, rates went from 8.5% to 20% in eight months. Rates were at 0% at the beginning of the current tightening cycle. The Fed’s dot plot shows a median projection for a 3.25-3.50% federal funds target range at the end of this year. Inflation has kept rising. It is hard to be optimistic when looking at the past for guidance.

Figure 2: Rate hikes haven’t always slowed inflation…

Source: NDR, St. Louis Federal Reserve. Data as of May 31, 2022.

Priced just right?

Gold may trade around the US$1,800 level for the short term. There is risk that at these levels as gold is vulnerable to market action by speculators and short sellers that could drive it lower. We have seen such activity in the past, and it can be damaging. However, at US$1,800, most of the “gold negative” news (higher rates, strong dollar, stable economy, under control inflation) appear to be priced-in, allowing gold to form a new and stronger price base around this level. This positions gold favourably to respond to a number of potentially “gold positive” news in the longer term (recession, persistent inflation, continued weakness in financial markets, a pause in Fed tightening) which could drive gold and gold miners much higher.

Higher costs still a drag on miners

While the price of gold is holding up well, the performance of gold miners has disappointing. Year to date, the NYSE Arca Gold Miners Index3is down 9.77%. Gold miners carry leverage to the gold price and that works in both directions, so any moves in the gold price are expected to be amplified for the miners. However, with gold down just 1.2% in the first half, the miners’ leverage to the metal can only partially explain the recent underperformance.

Another factor affecting performance is the broader equity markets selloff, which has also dragged down gold miners. In addition, the first quarter earnings reports for the gold miners were generally below expectations, with cost inflation and COVID-related interruptions negatively affecting results. Higher operating costs are impacting margins. We now estimate average all-in sustaining costs for the sector of about $1,200 per ounce in 2022, which is more than a 10% increase over 2021.

Nonetheless, at US$1,800 per ounce, free cash flow generation for the gold producers remains strong and should be supportive of gold miners. Gold producers are to a certain extent naturally hedged against cost inflation in that higher inflation has historically supported higher gold prices. We should see gold miners outperform if this historical correlation plays out in this cycle.

Only part of a bigger challenge, though…

At present, the gold mining sector faces a particularly daunting challenge: establishing itself as an investable sector through all market cycles in order to attract a broader investor base. We view this as a work in progress. A lot of the hard work has already been done. The transformation of the sector began in the second half of 2012 with widespread management team changes across the industry. This was followed by a decisive shift in strategy. The message was clear and consistent across the sector: growth was no longer the single priority; instead, the new focus was on controlling costs, meeting expectations and generating attractive returns to shareholders. The result is companies with little debt, a lot of free cash flow, attractive dividends and share buyback programs and a disciplined approach to growth.

In order to keep generating cash that can be returned to shareholders (the market’s main focus), companies must grow – and while the focus has been, and rightfully so, on growing margins and increasing returns instead of growing production – companies also have to replace their reserves and resources. On average, we estimate the life of the sector’s existing mines at approximately 15 years. To be able to sustain production beyond the next 15 years, companies have to find more gold; they have to grow their resources. They can do this organically through exploration around existing operations (brownfields) or in new properties (greenfields), or they can acquire the gold already discovered by others. Organic growth is cheaper than acquired growth, but all growth comes at a cost: The cost to find the gold and the cost to develop that gold deposit into a producing mine.

“Do everything but do nothing”

Which brings us to the next phase of the larger challenge faced by the industry. Gold producing companies are financially strong and able to fund their growth plans. However, the markets do not seem to like companies spending to find, develop and build mines. Whether it is through an acquisition of an asset or another company or through the development of one of the company’s assets, the market seems to generally punish gold miners on announcements of significant spending towards growth.

We understand there is reason for skepticism. It may be tough to forget the value destructive acquisitions, over spending and excessive indebtedness of the last gold bull market. However, companies, over the past 10 years, have demonstrated their continued discipline, focus on profitability, defending margins and increasing shareholder returns. Since mid-December 2015, the gold price has increased by 60%, and positively this has not resulted in the excesses of the past.

For companies to continue to create value, they must invest in growth. Growth-at-any-cost is a thing of the past, but growth-at-zero-cost is fantasy. The current inflationary environment is complicating things further for the gold sector. Building a mine requires a lot of materials, energy, labour and capital. Capex estimates for new projects are being revised up 20-30% due to cost inflation. The market is naturally spooked by such news, so miners generally drop when the revisions are announced. But in reality, in their quest to demonstrate that they can run a profitable and sustainable business with good returns through the economic cycles, gold companies have no choice but to explore, build and expand/upgrade mines even during periods of high inflation. It takes a long time (typically 10 or more years) to discover, permit, develop and put a gold deposit in production. Those companies that can manage to do so while maintaining attractive returns should outperform.

A work in progress

Gold miners appear to be in a transitional stage. The market may recognise the health of the industry, but it could take more time to demonstrate that the sector can continue to deliver good, sustainable results over the longer term, and despite the movements in the gold price. During this transition, it is imperative that companies meet their targets in order to continue to build credibility. Eventually, this disciplined approach should lead to gold companies earning their place as attractive investments within the broader equity universe.