Global markets

Global equities enjoyed a second successive week of gains, reflecting a good start to the Q3 U.S. earnings reporting season and a U.S. consumer price index report that was at least not a lot worse than feared. The S&P 500 bounced 1.8%, with the NASDAQ-100 up 2.2%, helped also by a small decline in U.S. 10-year bond yields from 1.61% to 1.57%.

As is usual, Wall Street’s major banks kicked off the reporting season and did not disappoint, helped by frenetic consumer credit card spending, financial market trading and M&A deals. The U.S. headline CPI was a touch higher than expected, rising 0.4% (market 0.3%), edging annual inflation higher to 5.4%. Core CPI inflation (i.e. excluding food and energy) was in line with market expectations, posting a 0.2% per cent gain, keeping the annual rate steady at 4.0%. U.S. inflation is high, but has it already peaked?

Despite talk of ‘stagflation’, other U.S. data was consistent with a hard-charging economy – weekly jobless claims plunged to 293k from 326k, while retail spending rose a much stronger than expected 0.7% (market -0.2%) in September. Indeed, it’s fairer to say that the so-called ‘supply chain bottleneck’ afflicting the U.S. economy is largely just a positive demand shock, fueled by the pandemic-related switch to goods over services and Biden’s huge and totally unnecessary fiscal boost earlier this year. The system just couldn’t cope with the surge in demand – which has led to shortages and pricing pressure. As supply belatedly responds, the fiscal sugar hit fades and demand switches back to services, these bottlenecks should resolve themselves – without ongoing pricing pressure – especially given the ongoing structural disinflation forces of globalisation and tech disruption. But we’ll see!

In other key news last week, the minutes to the recent (hawkish) Fed meeting suggest tapering will begin fairly quickly – in either November or December, with US$15b monthly reductions in bond buying such that the current US$120billion in monthly bond buying will be wound back to zero by mid-2022. That to me now seems fully priced by the market – and should not, in itself, place much extra upward pressure on bond yields (and hence downward pressure on equities). I’d note also the market has now also priced in two rate hikes by end-2022 – which to me seems the worst case scenario for rates next year. To my mind, that’s consistent with U.S. 10-year bond yields reaching 2-2.25% by end-22, though it need not happen this year. The challenges for the market in a rising yield environment were spelled out in my recent Market Trends report.

Key global highlights for the week ahead include China’s monthly ‘data dump’ today including Q3 GDP, which is likely to show annual growth slowing from 7.9% to 5.3%. There’s also a collection of Fed speakers which will keep taper talk alive. Friday sees the release of U.S. manufacturing and service indices, with a focus likely on the degree of delivery disruption and cost pressures. The persistence of cost pressures within the Fed’s Beige Book on Wednesday will also be closely scrutinised. Otherwise, the earnings season rolls on with key companies such as NetFlix, Intel and Tesla reporting.

Global equity themes

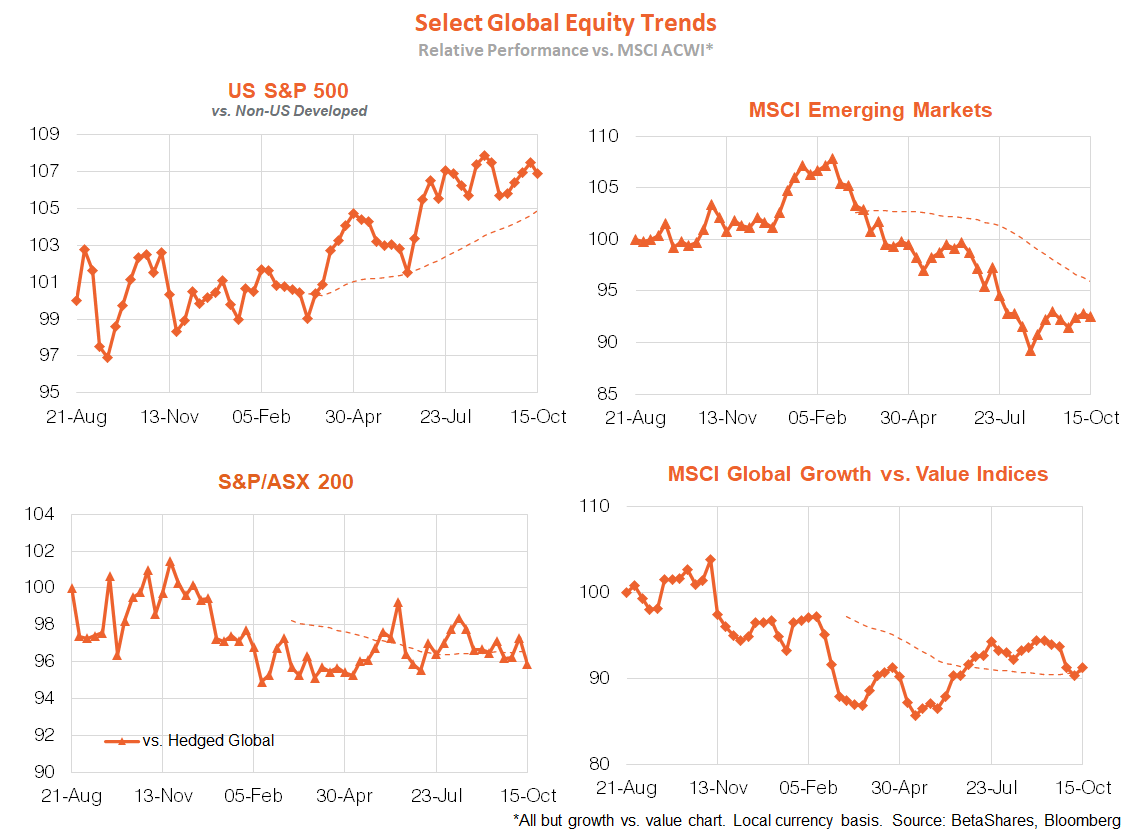

Growth enjoyed a bounce back over value last week, helped by the decline in bond yields – though the trend still appears to favour value. And while the U.S. relative performance trend is still up, Japanese and European equities enjoyed a stronger bounce than U.S. equities last week. The trend decline in emerging market relative performance appears to be bottoming out, and it’s now broadly tracking sideways. Australian performance remains choppy, with a slight downside bias.

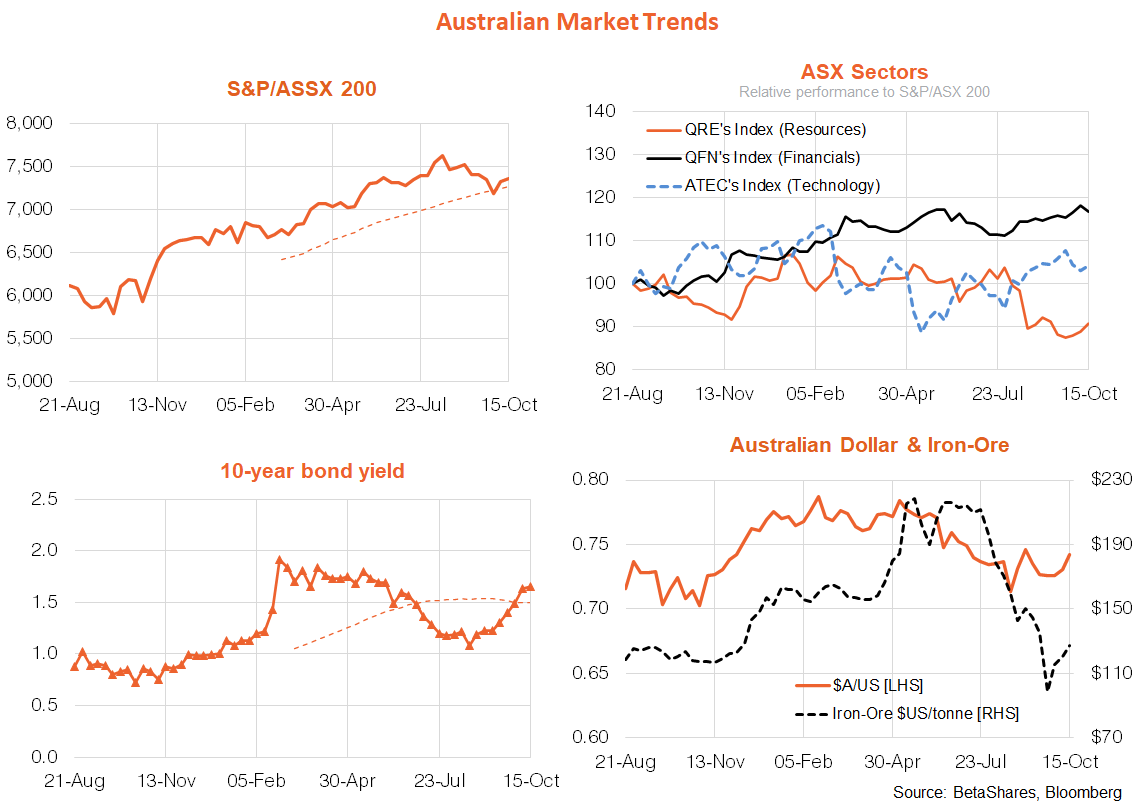

Australian market

Australian equities have yet to benefit from Friday’s bounce on Wall Street, constraining last week’s gain in the S&P/ASX 200 to 0.6%. The range of data released last week was broadly as expected, with a lockdown-related slump in both employment and the NAB index of business conditions. That said, business and consumer confidence are still holding up fairly well – at or above long-run average levels – suggesting the economy is poised to bounce back solidly once the NSW/Victoria lockdown ends.

Also of note, and despite the protestations of RBA Governor Lowe, the local bond market is now pricing in two rate hikes by end-22. Indeed, local 10-year bond yields have lifted a little more than than those in the U.S. since the bottom in yields in late July – the yield spread has widened – with the market simply not believing the RBA won’t follow the Fed! That suggests local fixed-rate bonds seem to offer reasonable value – especially compared to U.S. bonds. Higher local yields, along with an (oversold?) bounce-back in iron-ore have supported the $A.

There’s little local data this week, though RBA minutes are due tomorrow and Governor Lowe speaks on ‘Independence, Mandates and Policies’ on Thursday.

Have a great week!