Global market review

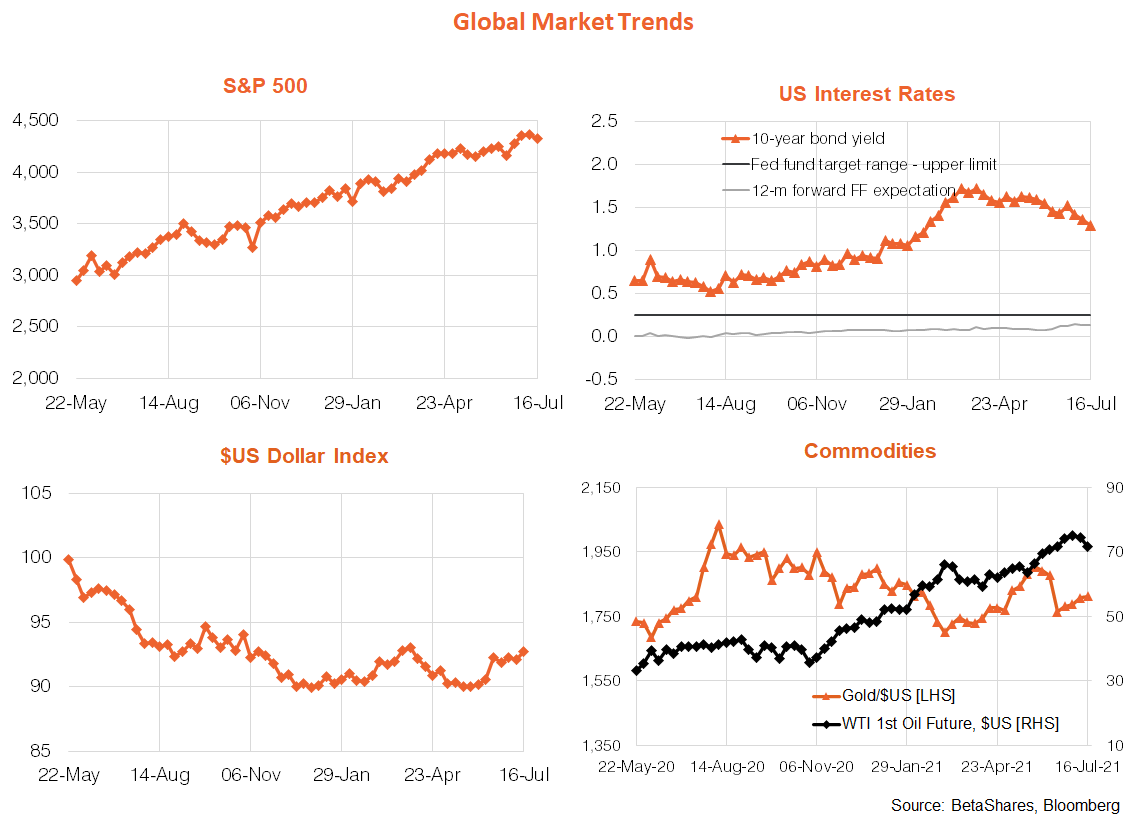

- U.S. stocks ended the week down after touching record highs earlier in the week, with some apparent concern on Friday that July U.S. consumer sentiment weakened on the back of a lift in inflation fears. Of course, that did not stop U.S. retail sales powering ahead in June as also reported on Friday. Earlier in the week, the market brushed off another higher than expected consumer inflation report, and for the same reason – namely much of the increase was concentrated in a few areas like used car prices, airfares and hotels. Further soothing market nerves was Fed chair Powell, who again reiterated that he’s in no hurry to tighten policy.

- Across global markets, oil edged lower while gold strengthened. Long-term bond yields eased further while the $US firmed.

- There’s little key global data for the week ahead, with U.S. manufacturing indices likely to remain firm when reported on Friday. That will leave markets to ponder further progress in the Q2 earnings reporting season – which at this very early stage (8% of S&P 500 companies have reported) is shaping up well, with major banks beating expectations last week.

- Markets will also be keeping a wary eye on the spreading delta COVID wave. Given high vaccination rates in the U.S. and Europe, however, what’s key is not the case count per se, but the extent to which we see a spike in hospitalisations and deaths, which could increase the risk of tighter U.S. restrictions.

Australian market review

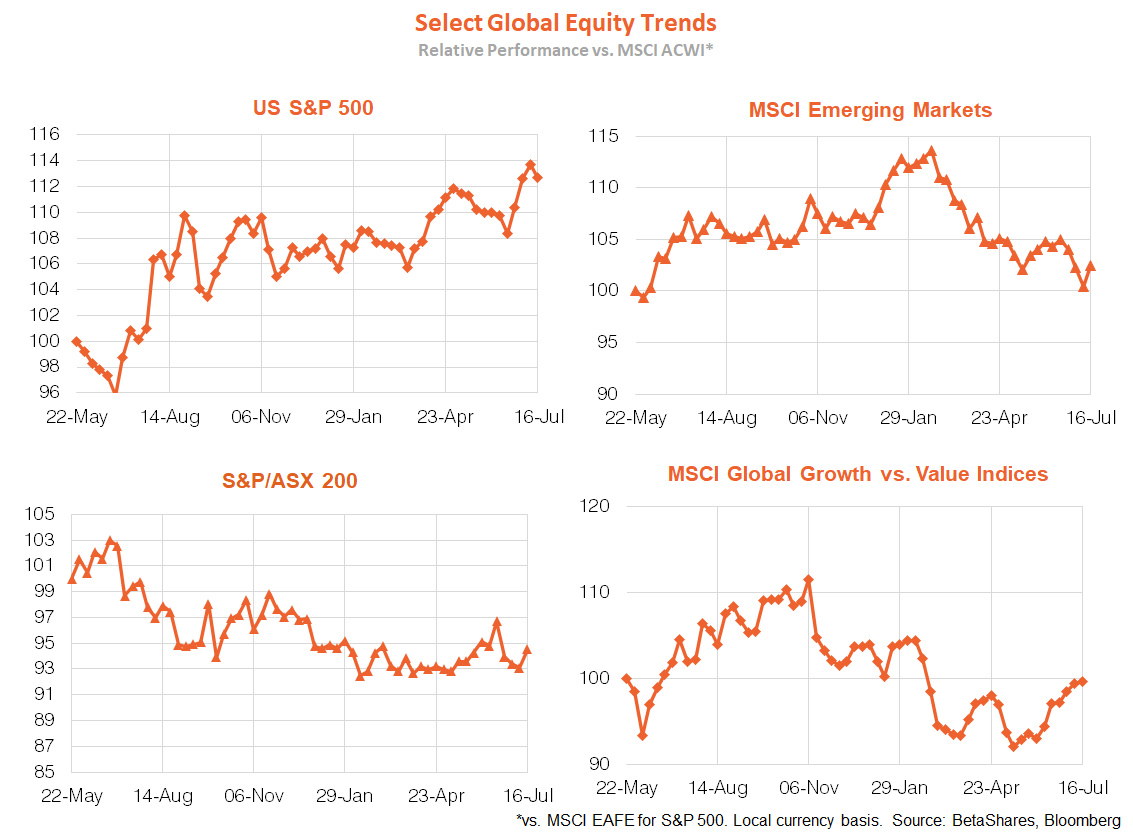

- The S&P/ASX 200 ended the week up 1% but will likely start the week down given Friday’s sell-off on Wall Street. The market has been grinding sideways in recent weeks after breaking higher in early June. Among key sectors, the relative performance of financials has eased back in recent weeks, though the relative performance of technology and resources has been choppy. Local long-term bond yields also continued to move lower, as did the $A – despite still relatively high iron-ore prices.

- As would be expected, there were signs of a lockdown-driven hit to both business and consumer confidence in the respective NAB and Westpac surveys last week, though both remain at high levels. Employment strengthened further in June (pre-dating the Sydney lockdown!) with the unemployment rate enjoying another impressive decline to 4.9% (from 5.1%).

- Of course, economic data is now taking a back seat to the lockdowns in Sydney and Melbourne. My estimates suggest lockdowns of both cities cost around 0.25% off national GDP for every week they continue (0.125% in NSW and 0.1% for Victoria), so a four-week lockdown in NSW and two weeks in Victoria (a likely best case scenario) would cost 0.7% off quarterly GDP or $3.7 billion – which would virtually wipe out most growth in the quarter. An eight-week NSW lockdown and four-week lockdown in Victoria (a worst case scenario?) would slice 1.4% off GDP, or $7.5 billion, which would imply negative growth in the quarter. At the margin, this will make the RBA even less likely to contemplate rolling back its bond buying program any time soon, though it would likely see little point in cutting the cash rate to zero from 0.1%. After all, we should expect growth to bounce back quickly in Q4 once the lockdowns end.

Have a great week!