Week in review

- Equities buckled under Fed tightening fears. The Fed policy meeting was of course the market highlight last week, particularly the increase in the number of Fed members who are now penciling in a rate hike in 2023 according to the ‘dot plot’ chart. Just over half (13 of 18) now see rate increases starting in 2023, while a chunky 40% (7 of 18) see the first move as early as next year. Markets were further pressured on Friday when Fed member Bullard again highlighted the risk of policy tightening next year.

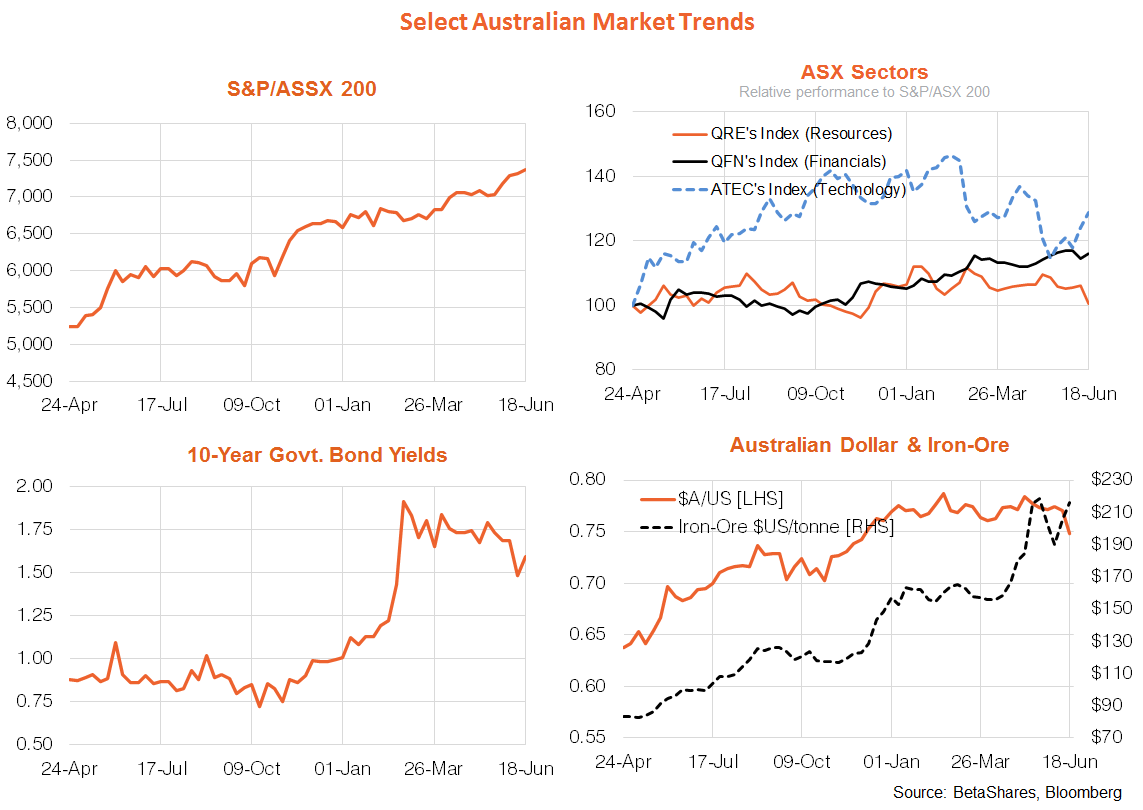

- In terms of market movements, U.S. long-term yields remained steady, however, though shorter-end bonds did sell off – causing the U.S. yield curve to flatten. Equities, gold and the $A weakened while the $US firmed. Value stocks solid off relative to growth.

- Locally, the bearish bias to bonds was further accentuated by a strong labour market report, with the unemployment rate dropping to 5.1% from 5.5%. Market chatter about a bring forward of RBA tightening from 2024 to potentially 2023 intensified.

Week ahead

- The Fed will remain in focus, with chair Powell fronting Congress on Tuesday. In a bid to appease markets, he may seek to play down Fed tightening fears. Indeed, last week he suggested the Fed’s dot plot “should be taken with a grain of salt”, as expectations can change as the economy evolves. That said, another four Fed members will also share their opinions over the course of the week, with Bullard again speaking tonight.

- A key U.S. inflation report is due on Friday, with the core private consumption expenditure (PCE) deflator expected to post another largish 0.6% gain after the 0.7% gain in April – taking the annual rate from 3.1% to 3.4%. As with the earlier consumer price index report (CPI), however, the market is already anticipating another high result – with debate now focused on how quickly supply-chain related price pressures ease in coming months.

- In Australia, May retail sales are released today and are expected to show another solid gain of around 0.5% – underpinning the solid economic outlook.

Summary

- Overall, monetary tightening fears are now the dominant market driver, which could see a further pullback in equities and strength in the $US. How the growth vs. value trade plays out remains to be seen, though the early market reaction suggests fear of the Fed is more negative for value stocks (to the extent to that lower long-term inflation/commodity price fears hurt energy stocks and yield curve flattening hurts financials through a squeeze on interest margins).

- Lets not forget, however, that we’re still talking about no lift in short-term rates for at least a year or so – and the surge in U.S. economic growth and inflation in recent months (due to the Biden stimulus and supply-chain bottlenecks) will likely moderate somewhat in coming months.

Have a great week!