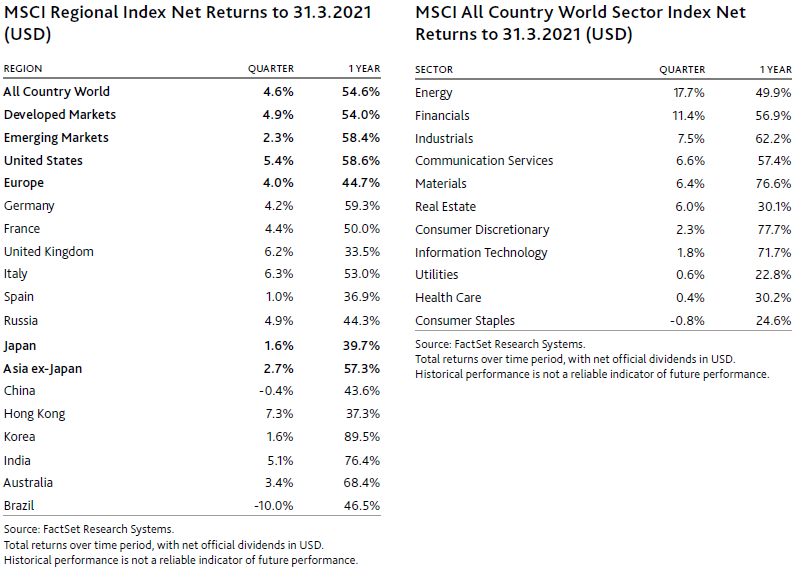

We are now one full year on from the COVID-19 outbreak and the subsequent initial lockdowns that resulted in a collapse in global economic activity and stock markets.

While the pathway of the virus has been one of rolling waves in response to lockdowns, reopenings and now the rollout of vaccines, since the March 2020 lows, economic activity has experienced a strong and steady recovery, as have stock markets. Indeed, many of the world’s major stock markets have comfortably surpassed their pre-COVID highs.[1] Fuelling this recovery in both economies and stock markets has been unprecedented (peace time) government deficit spending, funded through the printing of money.

The question is, where to now? It is highly likely that the global economy will continue its strong recovery path over the course of the next two years. In concert with this recovery, government bond yields will likely head higher, which will prove challenging for the speculative elements within stock markets.

Economic activity will likely continue to recover

There are numerous reasons to expect that global economies will continue to recover. The most obvious is the ongoing reopening of economies, as vaccination programs take us toward the post-COVID era. With current headlines focused on the failure of vaccination rollouts and the outbreak of new variants of the virus, this may seem an overly optimistic statement to many. However, the success of the vaccination programs in the US and the UK, where 32% and 46% of each population respectively has received at least one vaccine dose, shows what can be achieved once health systems swing into gear.[2] Where vaccination programs have been slow to start in some locations, such as Europe, an acceleration is likely, especially as the availability of dosages continues to improve. Variants in the virus are an expected setback, but fortunately the vaccines are being refined to address the variants, as they normally would with the annual flu vaccine.

Over the course of 2021, it is highly likely that we will move toward a situation where we return to freedom of movement across the world’s major economies. With this, we expect industries such as travel and leisure will continue their recovery, and with that, elevated levels of unemployment will continue to fall. With a light at the end of the tunnel on COVID and rising employment, consumer confidence has started to bounce back (see Fig. 1).

As such, a release of pent-up consumer demand across a range of goods and services should be expected. Indeed, households are well-positioned to increase their spending, as large portions of government payments last year were saved and not spent, resulting in unprecedented increases in savings rates (see Fig. 2).

Additionally, in the US, consumers’ bank accounts will be further inflated, with the recent passing of the US$1.9 trillion fiscal package. It is estimated that US consumers would need to spend an additional US$1.6 trillion dollars, or 7.5% of GDP,[3] just to return to trend savings levels. The recovery from the COVID-19 collapse is likely to be a very strong rebound that will play out over the next two to three years.

Given the levels of fiscal and monetary stimulus across the globe during 2020 and 2021 to date, the US will be at the epicentre of the recovery. The ongoing stimulus efforts in the US, including a potential additional US$3 trillion of spending on infrastructure and healthcare over the next decade, make the rest of the world’s efforts pale into insignificance. Indeed, China appears to be stepping back from stimulus programs, having already achieved a strong economic recovery.

Nevertheless, the US stimulus will help growth in Asia and Europe via the trade accounts, as is already apparent in the strong recovery in China’s trade surplus (see Fig. 3).

Long-term interest rates will likely move higher with the recovery

As a result of the strong rebound in economic activity, interest rates will likely rise and indeed, they already have. The reference here is to long-term interest rates, such as the yield on the US 10-year government bond, rather than short-term interest rates set by central banks (e.g. the Reserve Bank of Australia). In the fastest-recovering economies, US 10-year government bond yields have increased from 0.51% in August 2020 to 1.74% at the end of March, while Chinese 10-year government bond yields have risen from their April 2020 lows of 2.50% to 3.21% at the end of March (see Fig. 4). In both cases, these yields have returned to pre-COVID levels. It is not surprising that yields on government bonds are rising, as this is generally the case during a recovery. The issue is just how much further they may rise, given expectations for a very robust growth environment in 2021, the substantial amount of new bonds that will be issued in the months ahead and nascent signs of inflationary pressures.

Daily readings of consumer prices already show inflation heading back to levels last seen in mid-2019. As we discussed in our December 2020 quarterly report,[4] markets in a broad range of commodities and manufactured goods are seeing shortages in supply, resulting in significant increases in prices. One high-profile example has been the auto industry having to cut production due to shortages in the supply of components. Given the complexity of supply chains and the various factors that have been impacting them in recent years, such as the trade war and then the sudden collapse and recovery in demand in 2020, predicting how long such shortages will persist is difficult. However, it is interesting that these price rises, usually associated with the end of an economic cycle, are occurring at the start of the cycle instead.

Beyond the current supply shortages and associated price rises, the longer-term issue for inflation is how governments will finance their fiscal deficits. As we have discussed in past quarterly reports, when governments use the banking system (including their central banks) to finance deficits, it results in the creation of new money supply. The idea that the creation of money supply in excess of economic growth is inflationary, has lost credibility in recent years, as inflation didn’t arrive with the quantitative easing (QE) policies of the last decade. However, the mechanisms by which banking systems are funding current fiscal and monetary policies of their governments are clearly different to what was applied during QE. Rather than delve into a deep explanation, we would simply point to the extraordinary growth in money supply aggregates, where in the US, M2[5] increased by a record annual rate of 25% almost overnight in mid-2020. These types of increases did not occur during the last decade of QE policies. Further growth in M2 awaits in the US, following the latest rounds of fiscal stimulus, though the percentage growth figures will at some point fall away as we pass the anniversary of last year’s outsized increases.

So, we have a strong economic recovery from the ongoing reopening post COVID, fuelled by fiscal stimulus, already tight markets in commodities and manufactured goods, plus excessive money growth. Given that we also have central banks committed to keeping short-term interest rates low for the foreseeable future and allowing inflation to exceed prior target levels, it is hard to see how we can avoid a strong cyclical rise in inflation. It is an environment where there is likely to be ongoing upward pressure on long-term interest rates. To see US 10-year Treasury yields above 3%, a level last seen in only 2018, would not be a surprising outcome.

Rising long-term interest rates will represent a challenge for the bull market in growth stocks

In recent years, we have emphasised the two-speed nature of stock markets globally. As interest rates fell and investors searching for returns entered the market, their strong preference was for ’low-risk’ assets. At different times they have found these qualities in defensive companies, such as consumer staples, real estate and infrastructure, and at other times, in fast-growing businesses in areas such as e-commerce, payments and software. At the same time, investors have been at pains to avoid businesses with any degree of uncertainty, whether that be natural cyclicality within their business or exposed to areas impacted by the trade war. Last year, this division was further emphasised along the lines of ‘COVID winners’, such as companies that benefited from pantry stocking or the move to working from home, and ‘COVID losers’, such as travel and leisure businesses.

Over the last three years, these trends within markets created unprecedented divergences in both price performance and valuations within markets. However, as we noted last quarter, this trend started to reverse at the end of 2020, as a combination of successful vaccine trials and the election of US President Biden pointed to a clearly improved economic outlook. The result was ‘real world’ businesses in areas such as semiconductors, autos and commodities started to see their stock prices perform strongly and this has continued into the opening months of 2021.

Meanwhile, the fast-growing favourites continued to perform into the new year, though these have since faded as the rise in bond yields accelerated. Many high-growth stocks have seen their share prices fall considerably from their recent highs, with bellwether growth stocks such as Tesla (down 27% from its highs), Zoom (down 45%) and Afterpay (down 35%).

Theoretically, rising interest rates have a much greater impact on the valuation of high-growth companies than their more pedestrian counterparts. As such, it is not surprising to see these stocks most impacted by recent moves in bond yields and concerns about inflation.[6]

Many will question whether this is a buying opportunity in these types of companies. While they may well bounce from these recent falls, we would urge caution on this front, as for many (but not all) of the favourites of 2020 we would not be surprised to see them fall another 50% to 90% before the bear market in these stocks is over. If our concerns regarding long-term interest rates come to fruition, this will be a dangerous place to be invested, and as we concluded last quarter, “when a collapse in growth stocks comes, it too should not come as a surprise”.

If there is a major bear market in the speculative end of the market, how will companies that investors have been at pains to avoid in recent years (i.e. the more cyclical businesses and those that have been impacted by COVID-19) perform? While these companies have seen good recoveries in their stock prices in recent months, generally they remain at valuations that by historical standards (outside of major economic collapses) are attractive. It should be remembered there are two elements to valuing companies: interest rates and earnings. Of these, the most important is earnings, and these formerly unloved companies have the most to gain from the strong economic recovery that lies ahead. As such, we would expect good returns to be earned from these businesses over the course of next two to three years.

For many, the idea that one part of the market can rise strongly while the other falls, seems contradictory, even though that is exactly what has happened over the last three years. In this case, for reasons outlined in this report, we are simply looking for the relative price moves of the last three years to unwind. We only need to look to the end of the tech bubble in 2000 to 2001 for an indication of how this may play out – when the much-loved ‘new world’ tech stocks collapsed in a savage bear market, while the out-of-favour ‘old world’ stocks rallied strongly. This was a period where our investment approach really came to the fore, delivering strong returns for our investors.

ENDPOINTS

[1] Source: FactSet Research Systems.

[2] Source: https://ourworldindata.org/covid-vaccinations#what-share-of- the-population-has-received-at-least-one-dose-of-the-covid-19-vaccine

[3] Source: S&P Global Market Intelligence

[4] https://www.platinum.com.au/PlatinumSite/media/Reports/ptqtr_1220.pdf

[5] M2 includes M1 (currency and coins held by the non-bank public, checkable deposits, and travellers’ cheques) plus savings deposits (including money market deposit accounts), small time deposits under $100,000, and shares in retail money market mutual funds. Source: https://fred.stlouisfed.org/series/M2SL

[6] Growth companies tend to rely on earnings in the more distant future. When valuing a company, future earnings are discounted back to a present value using a required rate of return, which is related to bond yields. As bond yields rise, the discounting process leads to a lower value in today’s dollars, for the same level of future earnings.

DISCLAIMER: This article has been prepared by Platinum Investment Management Limited ABN 25 063 565 006, AFSL 221935, trading as Platinum Asset Management (“Platinum”). This information is general in nature and does not take into account your specific needs or circumstances. You should consider your own financial position, objectives and requirements and seek professional financial advice before making any financial decisions. You should also read the relevant product disclosure statement before making any decision to acquire units in any of our funds, copies are available at www.platinum.com.au. The commentary reflects Platinum’s views and beliefs at the time of preparation, which are subject to change without notice. No representations or warranties are made by Platinum as to their accuracy or reliability. To the extent permitted by law, no liability is accepted by Platinum for any loss or damage as a result of any reliance on this information.

MSCI Disclaimer: The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)