by Jordan Berta

As we enter the second half of 2020, it’s clear that the steady sharemarket rise of the last 10 years has ended, and we are in a new time of volatility and uncertainty. Following the historic market sell-off in Q1 and subsequent recovery in Q2, markets have largely laid flat and trended sideways for the past few weeks.

Asia’s battle with the virus

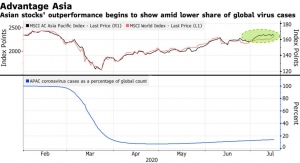

With fears that the continued spread of the virus will overwhelm government stimulus measures around the world, many markets have struggled to maintain and build on the returns of Q2. However, exceptions to this trend include the global technology sector and Asian equity markets, the latter of which have rebounded by ~40% from March lows1 and are now in positive territory year to date. Over the three months to 31 July, in $A terms the MSCI Asia Pacific Index (ex Japan) was up 5.2%, more than double the increase in the S&P 500 Index (up 2.5%) and the MSCI Europe Index (up 2.3%)2.

A great deal of this outperformance can be attributed to Asian economies’ ability to gain control of COVID-19 outbreaks relative to American and European counterparts. Since March 2020, reported virus cases in the region have made up less than 20% of the global count (according to John Hopkins data) allowing Asian economies to reopen 75% – 95% capacity, whilst the U.S. still stands at 45-60%3.

Source: Bloomberg, John Hopkins University

The Asian technology sector, similar to global tech industries, has been one of the most resilient and defensive parts of the Asian market. As many bricks and mortar businesses effectively shut up shop during lockdown periods, online companies saw a massive rise in the number of users of and subscribers to their services.

For example, Meituan Dianping (an online food delivery, consumer product and retail services business based in China), has seen the number of users of its platform jump by 8.9% year on year to ~450 million, doubling its share price from the start of the year to 19 June 20204, and joining the 10 most valuable companies on the Hong Kong Stock Exchange.

The two largest technology companies in Asia, Tencent (Chinese digital media and telecom conglomerate) and Alibaba (the Amazon of China), have seen their share price appreciate over the last two months by 27% and 32% respectively5.

The question for investors is: While Asian tech currently is thriving in the face of the COVID-19 panic, is this sustainable?

Asian upside post COVID-19

In addition to the ability Asia has demonstrated to slow down the virus’s infection rate, there are a number of fundamental characteristics which have made and should continue to make the Asian region, and particularly Asian technology, an attractive market for investors.

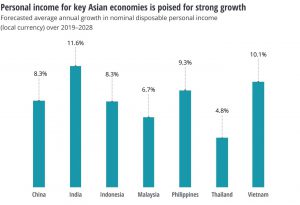

Favourable demographics – Since 1980, the GDP of emerging and developing Asian nations has grown on average by 7.2% p.a., outstripping the growth of advanced economies by three times6. Asia’s young and large population of 4.6 billion (which more than quadrupled over the 20th century7), coupled with the expansion of a strong middle class (which is expected to make up nearly 66% of the global middle-class population by 20308) should continue to bolster consumer spending domestically.

Source: Oxford Economics (Global economic databank), Deloitte Services LP economic analysis. Accessed 27 July 2020.Largest e-commerce market in the world – The Asia Pacific region has the largest number of internet users worldwide, reaching 2.3 billion in 20199. Already Asia represents the world’s largest e-commerce market, with China alone accounting for over 50% of global online transactions10. However, with internet penetration still below the global average, there is still a huge amount of growth to be had.

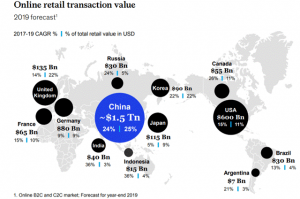

Favourable e-commerce landscape – Unlike the U.S., where e-commerce mainly connects stores with consumers to purchase goods, Asian manufacturers can sell directly to consumers without a physical store. Alibaba, for example, is a marketplace, which does not own the inventory of the merchandise sold, and merely connects buyers and sellers together. On the other hand, Amazon is a re-seller that owns the inventory and supply chain of its merchandise and sells directly to the customer. The factory to consumer supply chain has boosted e-commerce popularity with businesses and consumers alike, resulting in online retail transaction value growing by 24% CAGR in 2017-2019 to US$1.5 trillion in China alone, larger than the next ten markets combined11!

Source: iResearch and MOFXOM for China; eMarketer; McKinsey China Digital Consumer Trends 2019.

Diverse revenue streams – Asian tech is cushioned by diversity, as these companies drive revenue and earnings across multiple platforms and sectors. For example, advertising slumped on Tencent’s WeChat network, but its videogaming franchise surged during quarantines. Alibaba offset slumping consumer spending with rising demand for its cloud services.

Relative valuations to U.S. counterparts – Despite their growth, Asia’s tech stocks are not currently trading at demanding valuations by the standards of the other global players. As at end-June 2020, the average price-to-forward earnings (PE) ratio for leading Asian technology companies was around 23.6, compared to around 30 times earnings for companies within America’s tech-heavy NASDAQ-100 Index.

How to get exposure

Investors looking to gain exposure to many of the companies that could be best positioned to benefit from long-term demographic trends and capitalise on the structural growth of the technology sector in Asia can consider an ETF such as the BetaShares Asian Technology Tigers ETF (ASX: ASIA). ASIA currently holds the 50 largest Asian technology companies (ex-Japan), including Tencent, Alibaba and Meituan Dianping. From inception (18 September 2018) to 31 July 2020, ASIA has returned 27.8% p.a., and 28.6% year to date (as at 31 July 2020).

There are risks associated with an investment in ASIA, including information technology risk, concentration risk, emerging markets risk and currency risk. For more information on risks and other features of ASIA, please see the Product Disclosure Statement, available at www.betashares.com.au

ENDNOTES

- Strobaek, Michael, and Burkhard Varnholt. “A Year like No Other.” Credit Suisse – Investment Monthly, July 2020, p. 9.

2. Source: Bloomberg

3. “Global Economy Reopening Tracker | Insights.” Cushman & Wakefield, 13 July 2020, www.cushmanwakefield.com/en/insights/covid-19/global-economy-reopening-tracker.

4. Smith, Greg. “Meituan Dianping Thrives on Food Deliveries in Lockdown.” Australian Financial Review, 19 June 2020, www.afr.com/wealth/personal-finance/meituan-dianping-thrives-on-food-deliveries-in-lockdown-20200617-p553oa.

5. Perspective, Alt. “Tencent: Game-Changing Moves.” Seeking Alpha, 20 July 2020, seekingalpha.com/article/4359398-tencent-game-changing-moves.

6. “Real GDP Growth.” IMF Data Mapper, IMF, www.imf.org/external/datamapper/NGDP_RPCH@WEO/ADVEC/DA. Accessed 18 July 2020.

7. “Asia Population 2020 (Demographics, Maps, Graphs).” World Population Review, worldpopulationreview.com/continents/asia-population. Accessed 19 July 2020.

8. “Asian Consumers.” Deloitte Insights, Deloitte, www2.deloitte.com/us/en/insights/economy/asian-consumer-spending-growth.html. Accessed 18 July 2020.

9. “Internet Penetration in Asia-Pacific 2019.” Statista, www.statista.com/statistics/265153/number-of-internet-users-in-the-asia-pacific-region. Accessed 23 July 2020.

10. Godoy, Katelyn. “The Impact of E-Commerce: China versus the United States.” Cornell SC Johnson, 24 Feb. 2020, business.cornell.edu/hub/2020/02/18/impact-e-commerce-china-united-states.

11. “Tencent: Game-Changing Moves.” Seeking Alpha, seekingalpha.com/article/4359398-tencent-game-changing-moves. Accessed 21 July 2020.