Silver has become increasingly interesting to many investors. Not only does it exhibit similar properties to it more popular brother, gold, but it also has a much wider application in industry which gold doesn’t have.

As such, for strictly investment purposes, silver has historically performed in a similar way to gold, but also has further support from industrial manufacturing demand and applications. Investors should consider this precious metal if they want exposure to an asset that, historically, benefits from both investment and non-investment demand.

Non-Investment Demand

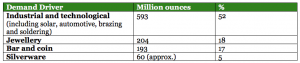

Non-Investment demand comprises about 50% of silver demand. This can be split into four categories, seen in the table below. For this note we focus on the industrial and technological aspects. Additionally, we briefly look at the supply deficit in silver, which should provide a support for silver prices.

Source: GFMS, Refinitiv/Silver Institute, 31 July 2019

Industrial and Technological Demand

The industrial and technological use of silver is integral to many of the current processes used in manufacturing. Crucially, it is expected to grow significantly over the next decade. David Holmes, a senior precious metals analyst from Heraues, made this comment on the growth in a conference held in London at the LBMA in late 2018.

Silver’s “long-term fundamentals as industrial demand within the electronics’ sector is expected to double over the next 15 years.”

Of the industrial demand drivers for price, the use of solar energy is probably the most interesting aspect. Moving forward, increased demand for silver is expected to come from the solar energy sector, since the precious metal is a great conductor of both heat and electricity, making it perfect for use in solar panels. Solar currently accounts for 2% of the world’s generated power that is expected to grow to 7% by 2030.1

Additionally, the progressive move towards electrical vehicles will increase the use of silver in cars too. Last year, around 36 million ounces of silver were used in automobiles. Each car itself uses about half an ounce of silver but the continuing electrification of cars is set to see that increase to one ounce. To put this in context, every electrical action in a modern car is activated with silver-coated contacts. Basic functions such as starting the engine, opening power windows, adjusting power seats and closing a power trunk are all activated using a silver membrane switch.

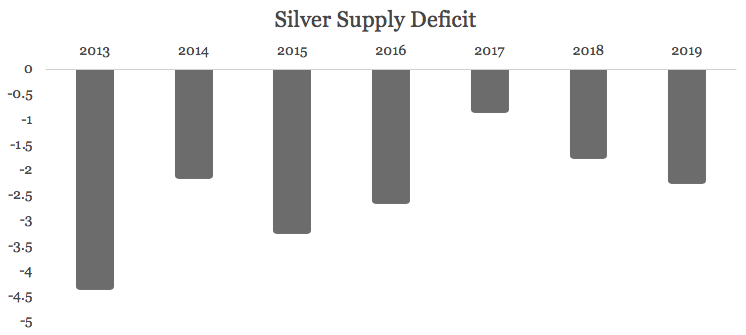

Demand Deficit

Further bolstering the positive tailwinds for the silver price is the supply shortage. Until recently, this had little effect on price but, as non-investment demand makes up about 50% of silver’s overall demand, it’s hard to avoid the impact of this continuing trend of demand not being met.

Source: Societe Generale, 2019

Investment Demand

Silver’s investment demand is based on a combination of fundamental drivers but also impacted by momentum.

Fundamental

Fundamentally silver’s investment demand profile is almost identical to gold. Currently this is primarily based on the desire to avoid currency debasement and the need for protection from threats to investment returns like trade wars and the end of the equity cycle. As much has already been written on this in regard to gold, this note will assume good knowledge of this from the reader.

Momentum

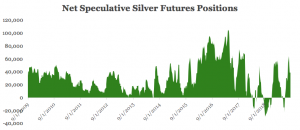

Momentum is also a driver of silver. Often increased interest begets further interest, and this can either help the price of silver move up further than expected short term or serve as a strong support when there is a correction. On this, the futures market gives a good indicator of momentum via the “net speculative positions” charts.

Below you can see that silver is currently net long in terms of its futures positioning, meaning that there are more buyers than sellers. On the short-term chart one can see that the positioning has risen up very rapidly lately, however, crucially, it doesn’t look extended versus other periods – especially versus 2016. Furthermore, the current positioning is off the back of a period (2018 – Q1 2019) where, on several occasions, silver was in a net short position i.e. investors were betting that silver was going down. As you can see, this was the only time this was the case since 2009 and serves to reinforce the current position as not overbought.

Source: Bloomberg as at 22 August 2019

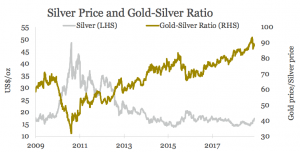

Gold/Silver Ratio

Finally, there is the gold/silver ratio. Many look at this as an indicator as to whether gold is expensive relative to silver or vice versa. Currently, based on this measure, silver currently appears undervalued. For those who believe the relationship should reinstate itself, many are buying silver as well as gold.

Our view at ETF Securities is that it is not entirely clear whether this relationship stands anymore, or, at least, is as strong as it once was. This is because the use of silver in a non-investment capacity has grown so much over the last decade that it is becoming equally as meaningful as the investment demand. This is in contract to gold which is much more driven by investment demand. Nonetheless, we are not saying the ratio has no value. Only that it should not be a primary driver of silver investment.

Source: Bloomberg as at 15th August 2019

Summary

In summary, silver’s price is dictated by both investment and non-investment demand. Silver shares many of the same fundamental characteristics for investment demand as gold but, because it is used far more widely in manufacturing for industry and technology, its price is also dictated by non-investment demand too.

Taking both into consideration in the current environment, silver’s prospects look attractive and we encourage investors to looks at this in more detail.