Copper is a crucial commodity because it’s utilised in an enormous variety of applications – from the construction industry to motor vehicles, from household electrical goods to energy transmission. Hence, it’s the world’s key industrial metal in terms of both volume and its influence on world markets.

Recent Price History

Let’s firstly examine the price action with respect to copper over the course of recent years.

As the graphic below clearly shows, copper found a bottom around $1.94 a pound on COMEX during January 2016. Coincidentally, this was when most industrial commodities were consolidating before a major rally.

The key catalyst that was to stoke the resurgence was government-implemented stimulus in China, the metal’s biggest consumer. Copper, as one of the primary barometers of global economic growth, then went on a major run, registering increasingly higher lows and higher highs before reaching a peak around $3.32 during December 2017.

When we focus more specifically on what’s happened so far in 2018, we see that for the majority of H1 2018 copper traded comfortably above the $3.00 per pound level.

The metal’s price performance therefore reflected what I consider to be its long-term incentive price. In other words, the price that producers require in order to incentive long-term supply. My view is that a copper price of at least $3.00 a pound is necessary for miners to justify bringing on-stream the massive new high-capex developments that are necessary to satisfy future copper demand.

From the middle of this year however (as the graphic below clearly reflects), fundamentals in the copper market went out the window and fear/speculation took hold. And we can probably use this as a metaphor for the resource sector as a whole.

Markets pre-empted any tangible impacts from Trump’s trade imbroglio with China by selling out of key commodities, copper included. The situation was further exacerbated by a ‘flight to safety’ with the US dollar, which further impacted commodity prices. The rise in the dollar has also been driven by rising interest rates.

The impact of a strong US dollar is that it makes all commodities – copper included – more expensive with respect to other currencies. Commodities are traded and quoted in US dollars on the majority of the world’s metal exchanges, so when the value of the US dollar rises, it automatically makes them more expensive for buyers in other currencies that have to convert their currencies – whether it be yuan, yen or whatever – into US dollars to purchase.

Copper has therefore copped a double-whammy – with the metal becoming more expensive in terms of other currencies (thus providing a temporary disincentive for industrial end-users), whilst speculators/funds have sold down their positions or boosted their short positions.

Copper not surprisingly began what became a quite dramatic price slide from about mid-year. The strong dollar, rising US interest rates and concerns over the escalating trade dispute between the USA and China weighed heavily not only on copper, but also other nonferrous metals and industrial commodities. Copper slid to a low of $2.60 in-mid-August as the dollar index hit fresh highs.

Outlook

My view on copper is that it’s a market being driven by fear and sentiment, rather than pure fundamentals. Whenever you have such a situation in markets, there is the potential for a significant reversal. Accordingly, I believe there are several strong reasons why the copper market (and copper equities) can recover solidly during 2019.

Reason One – Falling Inventories

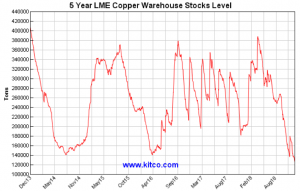

Let’s firstly examine the situation with copper stockpiled in warehouses around the world. Despite price weakness in the copper market since its June peak around $3.35 a pound, stockpiles on the London Metals Exchange (LME) and COMEX have been falling – and rapidly. LME inventories of copper reached the highest level since 2013 in March 2018 at over 388,000 metric tons. Since then, stocks have dropped dramatically.

As the five-year chart clearly underlines, inventories on the world’s leading copper exchange have declined steadily since early 2018 and are currently around lows of 130k tons – almost 258k tons or more than two-thirds below their level just nine months ago.

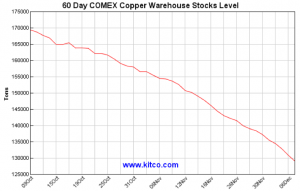

At the same time, stockpiles in COMEX warehouses too have been falling, with the 60-day graphic below highlighting that inventories have declined from 170k tons to the 135k ton level – a drop of more than 20% over the past two months.

What all of this tells us is that demand for copper remains robust, with inventories painting a very different picture of the copper market than simply looking at price action alone. Market sentiment therefore isn’t a very good guide.

This is backed up by the fact that LME copper inventories are currently at their lowest level since at least 2014. Less metal in warehouses is a bullish indicator from a fundamental perspective.

Factor Two – China Remains Dominant

China remains the world’s biggest copper consumer as it continues its massive infrastructure build. The health of its economy therefore remains an important factor in the outlook for copper. Which is why all eyes are currently on progress with respect to trade negotiations underway between the U.S. and China.

Both parties have agreed to enter a period of negotiation that will lead to a trade deal within 90 days from the beginning of 2019. The stakes are high. An ongoing trade dispute between the U.S. and China could send the global economy into a recession, as protectionism interferes with growth. Therefore, the odds favour a trade deal between the nations, as it is in the best interests of both countries.

Should a trade agreement be forthcoming, conditions will favour a higher copper price, as well as other industrial commodities.

Factor Three – Dollar Less Dominant

The graphic below is informative because it shows that copper has been making higher lows since mid-August’s low around $2.55 a pound. The current technical position of the copper market suggests that it will continue to consolidate above technical support and below resistance.

Evidence for this is provided by the recent performance of the US dollar index. The US dollar index rose to a high in mid-August that coincided with the copper low referred to above. Meanwhile, in mid-November the dollar index climbed to a higher high at 97.53, but copper fell to a low of $2.66 a pound – above its August low.

Despite the inverse relationship between the US dollar and commodities prices, the copper market has proven itself to be resilient in the face of a rising dollar. When a market does not move lower in the face of a traditionally bearish influence, it tends to be a sign of fundamental strength.

According to chartists, the critical level of resistance for the COMEX copper futures market currently stands at $2.8750 a pound. Perhaps a US-China trade deal will provide the fillip that copper needs in early 2019. Perhaps maybe even before that, the prospect of a pause in the US rate cycle as suggested by recent dovish Fed talk could take further heat out of the dollar, which in turn will provide more support for key commodities like copper.