Overview

Rising US interest rates and a strong US currency have continued to apply downward price pressure on gold, but the yellow metal’s resistance is growing. This has been helped by world stock market volatility, which has seen gold perform strongly over the past month due to its safe-haven status.

There are further indications that inflation is emerging, with trade tariffs and other factors likely to accelerate the inflationary process. There are real concerns now emerging about the impact that the trade war is having on market confidence and international trade.

The Trump administration is facing an uncertain future at the upcoming mid-term congressional elections, which could provide further market uncertainty. Domestically, enormous US debt levels and rising interest rates also provide concern, as the cost of servicing the debt escalates.

The recent gold sell-off is overwhelmingly a transient phenomenon, mostly decoupled from any intermediate or long-term fundamentals, thus representing a compelling buying opportunity. Central banks recognise this and have continued their buying spree, led by Russia and Hungary.

Gold equities are at their cheapest levels in almost eight decades when compared to equity markets and the underlying metal, which has likely led to an increase in mining stock acquisition deal-flow over recent months.

The Australian dollar gold price continues to go from strength to strength, continuing its consistent performance of the past 20 years. The incredible rise in the A$ gold price might surprise some investors and is providing strong margins for domestic producers.

Recent Activity

The price action in the gold market since April 2018 has left lots of market participants wondering if – and when – the yellow metal will recover, given the double-whammy of rising rates and a strong dollar. However, in our previous commentary we’d highlighted various factors that underlined exactly why I believed gold had reached a bottom.

The gold market is currently entering what has become over recent years – 2015, 2016, and 2017 – a seasonally weak time of the year. A seasonal pattern of lows during the final month of the year had corresponded with the actions of the U.S. Federal Reserve, as they have increased the short-term Fed Funds rates in each December since 2015, when the zero-interest rate environment in the United States ended.

The U.S. dollar is the world’s reserve currency, so the price of gold can be highly sensitive to moves in both the dollar and U.S. interest rates. Rising short-term U.S. rates, while those in Europe and Japan remain in negative territory, has put upward pressure on the dollar. The long-standing inverse price relationship between the U.S. currency and the yellow metal has been a bearish factor of the price of gold.

At the same time, rising interest rates tend to cause the cost of carrying commodities inventories (or long positions) to rise. In the gold market, higher real rates are a bearish factor, although higher rates that reflect mounting inflationary pressures on the U.S. and global economy can be supportive for the price of gold.

The price of gold fell to its lowest level of 2018 in mid-August at just above the $1160 per ounce level when the U.S. dollar index hit its high at 96.865 (refer to graphic below). As the dollar has moved back to the 95-pivot point on the index, the price of gold has recovered. From a trading perspective, in order for gold to experience a vibrant rally in the immediate term, the dollar index should break decisively under its nearest pivotal low at the 95.00 level. Interestingly, over recent sessions gold has displayed strength despite the move in the dollar index towards the mid-August high.

Many other factors are facing the gold market as we move into the final two months of 2018. Stocks have begun to show cracks in their bull market under the weight of rising rates, which has injected a dose of uncertainty and fear into markets across all asset classes. The current environment could drive some investors and traders into the gold market. At the same time, central banks remain net buyers of gold, adding to total official sector reserves.

At the same time, sanctions on Iran took effect on November 4, the trade dispute between the U.S. and China continues to escalate, and Saudi Arabia is under an international microscope after the murder of Washington Post journalist Jamal Khashoggi. President Trump has declared he is prepared to walk away from a nuclear treaty with the Russians. Many events will impact markets across all asset classes over the coming weeks and months, including the unknown, that could cause buying in the gold market.

Central Banks Buying Gold Aggressively

Hungary’s central bank recently announced it has increased its gold holdings ten-fold, from 3.1 metric tons to 31.5 tons. Hungarian central bank governor Gyorgy Matolcsy described the move as one of “economic and national strategic importance,” adding that the extra gold made the country’s reserves “safer” and “reduced risk.” This is the first time since 1986 that Hungary has increased its gold holdings, making it a significant event for Hungary and potential sign of things to come from other nations.

Hungary isn’t alone in its mission to diversify via increasing gold reserves. Poland recently became the first European Union (EU) member to increase its gold reserves in two decades. The National Bank of Poland (NBP) acquired gold in two batches: two tonnes in July and seven tonnes in August, according to IMF data. Poland’s gold bullion reserves now stand at the highest level since at least 1983.

In all, central banks have bought a total of 264 tons of gold this year, with Russia leading the way. The Russian central bank added 26.1 tons of gold to its hoard in July alone. Russian gold reserves increased by 224 tons during 2017, marking the third consecutive year of plus-200 ton growth. In all, Russia’s gold reserves have quadrupled since the 2008 financial crisis. This comes alongside a strategic divestment of U.S. Treasuries.

During February 2018, Russia overtook China to become the world’s fifth-largest gold-holding country. China has not officially announced any additions to its reserves since 2016, but many speculate the Chinese might secretly stockpiling the yellow metal as well.

Escalating Debt

Fiscal policy initiatives by the Trump administration have increased the level of U.S. debt. While the jury is still out on the impact of the aggressive and protectionist trade policies, corporate and individual tax reform have caused lower revenues to flow into the government’s coffers. While economic growth is increasing the overall tax base, the rate of taxation has declined. However, rising interest rates mean that it is becoming a lot more expensive to finance the debt. Before the initial rate hike in December 2015, the Fed Funds rate was at zero-percent, which took the pressure off financing debt. A 2.25-2.50% band on the Fed Funds rate at the end of 2018 dramatically increases the funding costs for the expanding level of debt.

Gold is both a commodity and a financial asset. As the U.S. debt eats away at the value of the dollar and rises to levels that could prove unmanageable in the coming years, the limited supply of gold in the world could become more valuable.

Rising Inflation

At their most recent meeting, the Fed told markets that the rate of inflation is now at the central bank’s 2% target rate. Higher real interest rates are bearish for gold, but when they rise because of inflation, which eats away at the value of money, the price of gold tends to appreciate. Gold is a barometer of inflation, and the economic condition continues to increase. While the Fed has not sounded any inflationary alarm bells, crude oil is at its highest price since 2014, and the trade dispute between the U.S. and China is likely to cause the prices of consumer goods to rise. Rising prices that increase inflationary pressures is bullish for the price of gold. Moreover, after a decade of central bank accommodation and cheap money, inflation could be the price for the stimulus that lifted the world out of the global financial crisis of 2008.

Political Uncertainty

We could be entering a period where the fear factor rises in markets across all asset classes. The mid-term elections in the United States could further divide the nation along political ideologies. A victory by the Democrats would put roadblocks in front of the Trump administration’s initiatives and may even threaten the President’s continuation in office. Harsh sanctions on Iran that take effect in November will increase the temperature in the Middle East and could lead to even more conflict in the region. The trade dispute between the U.S. and China continues to escalate and could deteriorate into a trade and currency war which would increase fear and uncertainty in markets across all asset classes. These issues, and many more, that face markets could increase the demand for gold and other safe-haven hard assets in the coming weeks and months.

Gold Mining Stocks Undervalued

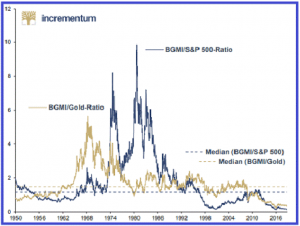

Gold mining stocks are undervalued relative to the gold that they mine. The HUI/gold ratio is currently at 13, versus an average closer to 35 over the past 16 years. The ratio traded above 60 briefly in 2003 and above 50 for much of the bull run from late 2003 to 2008. With the HUI/gold ratio so low, it increases the odds that mining stocks will offer leveraged gains versus gold into the future.

The chart above, sourced from Incrementum (the October 2018 chartbook update to the “In Gold We Trust” 2018 report), shows the ratio of Barron’s Gold Mining Stock Index (BGMI) to the price of gold (gold line) and the S&P 500 (blue line) going back to 1950. As you can see, gold mining stocks are trading at their lowest level relative to gold and the broad stock market in 78 years. The two dotted lines show the median level for each ratio since 1950.

The chart implies that now is one of the best times since World War Two to buy mining shares. Not surprisingly, industry insiders must agree with that assertion, as mining stock acquisition deal-flow has picked up considerably in the last few months. Most of the deals have been concentrated in the junior mining stocks. But Barrick’s acquisition of Randgold, announced in September is the largest precious metals merger in history.

Gold Prices Strengthen in A$ Terms

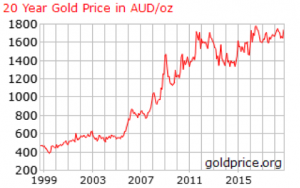

The graphic below highlights the strong and consistent performance of the gold price in Australian dollar terms over the past 20 years. The incredible rise of gold in A$ terms might surprise some investors. Of course, our domestic miners are continuing to benefit from this very strong pricing environment, allowing them to generate strong margins and accumulate significant war-chests to engage in growth opportunities.

Conclusion

I view gold’s current period of consolidation as a positive for the future path of least resistance of the price for the yellow metal, even though we are entering a time of the year where gold has made seasonal lows over the past three years due to rate rises. I believe the specter of trade and political uncertainty will help drive a recovery in gold prices. I anticipate gold will recover to trade between $1250 and $1350 over the next 12 months.