Copper’s price resilience over recent years is a reflection of sound market fundamentals. Demand is being driven by both traditional and new-age applications, whilst the supply-side reflects challenges around a market that’s heavily dependent upon ageing mines. The path of least resistance suggests a continuation of copper’s price strength that began back in late 2015, with prices close to a five year-high.

Copper’s price performance shows that it’s a metal that’s effectively been in a bull market since a broader commodity market low that occurred during late 2015/early 2016, coincident with a bottoming of negative sentiment related to a perceived Chinese economic slowdown and a somewhat sluggish world growth picture.

Figure 1: 3-year Copper Price Performance

Copper’s price recovery has significance too from a broader perspective, because of the metal’s value as a barometer of economic health more generally, representing a staple component of construction and infrastructure building. Its gains have coincided with increased optimism about the state of the world economy and more optimistic growth forecasts. As a result, copper’s strong track record can be seen in the context of a very healthy performance right across the commodity spectrum.

More recently we’ve seen a consolidation in copper’s price performance that isn’t in any way reflective of a deterioration in copper’s bullish thematic – rather it’s been a knee-jerk response to a modest recovery in the performance of the US dollar. The declining value of the US currency throughout 2017 had been broadly supportive of virtually all commodities, effectively making them cheaper in terms of other currencies. However, recent US rate increases have generated support for the US dollar.

What’s important to remember though is that physical markets (represented by the buyers who actually take delivery of commodities to meet real-world demand) tend to ignore concerns around growth, the dollar and rising interest rates. This is simply because the world doesn’t stop consuming important commodity staples simply because of factors that might sideline financial traders.

Nevertheless, the contrasting fortunes of copper versus the US dollar over the past 12 months are clearly evident in the graphic below. What it reflects is that whilst copper has experienced periods of selling, the lows continue to be higher, even with the rising US dollar over the past few months. If the US dollar were to resume its downtrend, copper could see more dramatic price upside.

Figure 2: 1-year Copper Performance v US$ Index

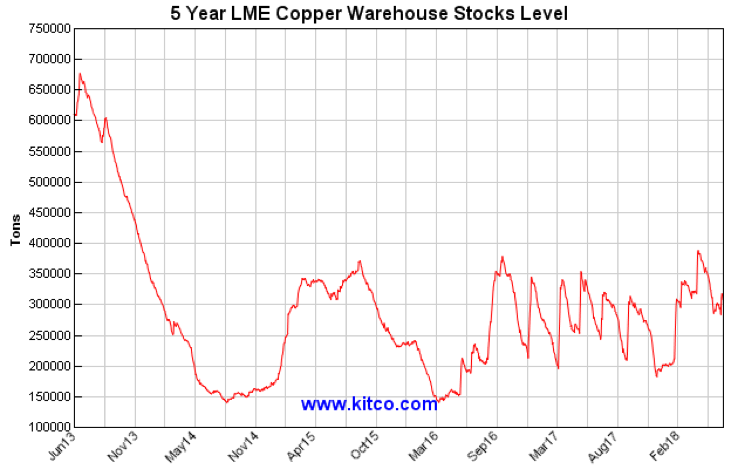

It’s also important to examine what’s currently happening with respect to copper stockpiles. The London Metals Exchange (LME) is the most liquid exchange for trading base metals and the level of warehouse stocks can influence the price of commodities when it comes to the supply and demand picture.

What the graphic below reflects is that the copper price recovery that took place from late 2015 onwards had its origins in the dramatic plunge in LME stockpiles that began in mid-2013. Since the recovery in copper prices, LME stockpiles have existed in a range between 150,000t at their low-point and just shy of 400,000t at their peak.

In this context, markets are increasingly nervous given the potential for strike action at the world’s biggest mine, Escondida in Chile, which now accounts for 5% of world output. The world is increasingly relying on ageing mines with falling grades, with higher operating costs. Higher prices are therefore a reality.

Figure 3: 5-year LME Copper Inventory Levels

There are strong demand factors that are positively impacting copper, with economic growth in the USA, China and elsewhere providing support. In the USA, unemployment remains at very low levels and economic activity continues to be buoyant. China’s growth rate has slowed somewhat to around the 6.5% level, but it must be remembered that this rate on the current level of GDP amounts to greater economic activity than when growth was at double-digit levels. The nominal amount of Chinese economic growth means that demand for copper and other industrial commodities remains strong. China drives the global copper metal market, accounting for more than two-fifths of world demand.

At the Chinese party Congress in Beijing during October 2017, President Xi pledged to increase the size of China’s middle class, which means the nation will continue to build infrastructure for its 1.4 billion citizens. At the same time, the leader of China promised to combat pollution by reducing smelting and refining of metals near major cities. A decline in the output of metals means that China will need to increase imports from around the world to meet the nation’s requirements in many commodities, including copper.

Summary

Copper’s price resilience over recent years, despite near-term uncertainty related to rising interest rates and the US currency, is a reflection of sound copper market fundamentals. Demand is being driven by both traditional and new-age applications, whilst the supply-side reflects challenges around a market that’s heavily reliant on ageing mines. All of these factors point to a continuation of copper’s impressive price performance that had its genesis back in late 2015. Realistically, producers are likely to need a base-case copper price of at least $3.00/lb and most likely $3.50/lb in order to maintain production and implement expansions to provide enough supply to satisfy growing world demand.