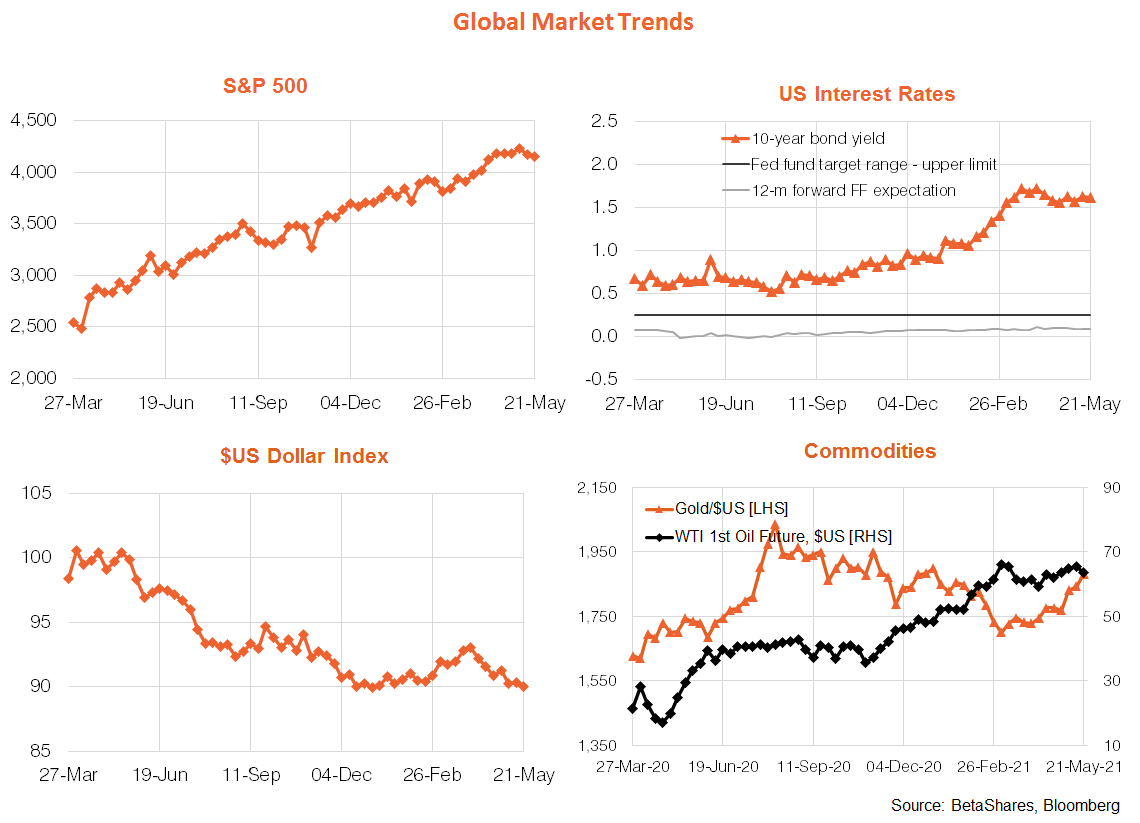

Global markets

Overall it was a week of further consolidation for global equity markets, with the S&P 500 down modestly for the second week in a row. With real activity data remaining unquestionably strong (the U.S. Markit composite PMI index hit a record 68.1 in May), market concern is focused on the degree to which current price/commodity pressures persist, and how central banks may react. Accordingly, the market weakened somewhat on hints in last week’s Fed minutes that a few more voting members want to talk about tapering the current monthly bond buying program “at some point”. That said, Wall Street saw fit to bounce back strongly on Thursday – reportedly due to a further notable drop in weekly jobless claims.

Of course, the big story last week was the slump in cryptocurrencies, with Bitcoin down a lazy 30% from the previous Friday. It’s now down 47% from its recent peak in mid-April, confirming its questionable role as a store of value! Why the slump? Its role as a medium of exchange has recently come under question, first with Tesla backing down on its earlier pledge that it will be accepted as a means of payment (on environmental grounds) and then Chinese authorities also last week clamping down on its use in financial transactions. Where will Bitcoin go from here? Don’t ask me – I’ve got no idea. Either way, one apparent beneficiary of the crypto crash has been gold, which was up 2.1% in the past week and 10% in the quarter so far.

In terms of major global trends, overall U.S. equities have only pulled back modestly to date, while bond yields and oil prices are tracking sideways and the $US remains weak. As noted above, the major new trend is a rebound in gold prices.

There’s a smattering of U.S. economic data this week which is likely to confirm the world’s largest economy continues its strong recovery. That said, such is the market at the moment, weak data could actually benefit equities if it reduces fears of higher inflation and interest rates. Of potentially more interest this week will be the core consumer price expenditure deflator (PCE) on Friday – which is expected to mimic the recent CPI report in showing an upsurge in consumer prices during April. This time, however, the market seems prepared – with the annual core PCE rate expected to lift from 1.8% to 3%. The market will also remain attentive to the gaggle of Fed speakers, and the degree to which any of them think it’s a good time to talk about tapering.

Global equity trends

Growth, Japan and emerging markets enjoyed a small relative performance bounce back last week, though trends still appear to favour the U.S. market and value. While the U.S. and Europe have been outperforming since mid-February, with Japan slowly but surely getting on top of its latest COVID outbreak we may well see a re-emergence of Japanese outperformance in the weeks ahead.

Australian market

The Australian market also continued to consolidate last week, with mixed economic reports and some emerging frustration with the pace of vaccine rollouts.

Despite a 30k drop in employment in April, the unemployment rate also dropped from 5.7% to 5.5% as most losing their jobs apparently decided to leave the labour force rather than look for alternative work. Popular commentary attributes the job losses and reduced labour force participation to a higher than usual number of casual workers deciding to take holidays in Easter! Really? I’m not so sure, and suspect the ending of JobKeeper played a role. Either way, however, I suspect any lost jobs will quickly be made up given the currently high level of labour demand.

In other news, the wage price index rose a very modest 0.6% in the March quarter, to be up only 1.5% over the year. Consumer confidence also dropped back from the very high levels reached in April.

Iron-ore prices pushed further into the stratosphere, though there are tentative signs that a peak may be in sight, especially as China’s post COVID breakneck pace of growth starts to moderate somewhat.

In terms of the week ahead, we get a few key Q1 GDP growth building blocks in the form of construction work done and private capital spending. Construction should be solid, underpinned by the housing boom. Business investment should also lift, supported by equipment spending thanks to the accelerated asset write-off policy. Perhaps even more important, it would be surprising and disappointing if year-ahead business investment plans did not also enjoy a solid upgrade due to the better than expected economic rebound.

Have a great week!