Global markets

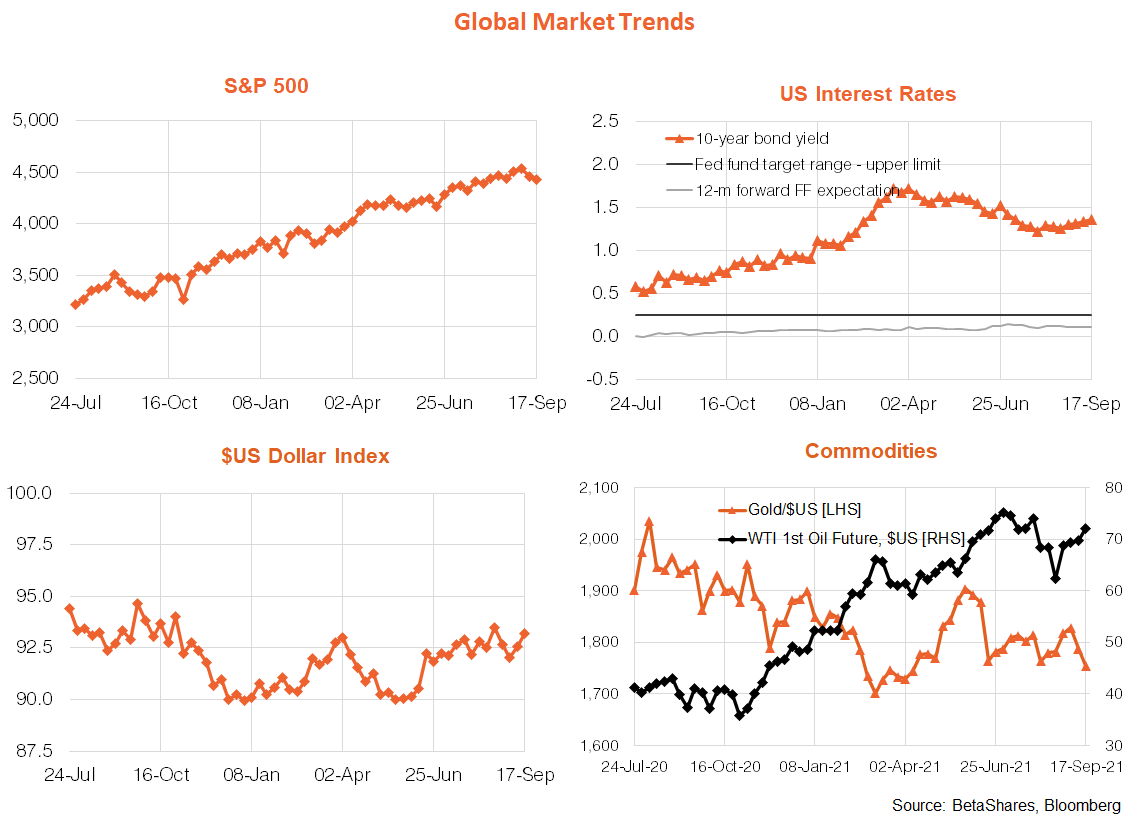

Global equities traded heavily last week, with Wall Street decidedly unwilling to rally even on good news. Indeed, the U.S. August consumer price index report came in a bit lower than expected, while retail sales were higher than expected – neither of which elicited much market positivity. Meanwhile, U.S. stocks slumped almost 1% on Friday, with some blaming a smaller than expected bounce back in consumer sentiment!

Methinks the market is not really focusing on the data at present, but rather this week’s impending Fed meeting and the still uncomfortably high rate of U.S. COVID deaths and hospitalisations, even though the latter are regionally concentrated and largely affecting those still stubbornly unvaccinated. Just for the record, around 2,000 Americans are now dying each day from COVID, which is still below the peak of 3,000 in January but in line with the peaks when COVID first struck in early 2020. On a per capita basis, that would be like 200 Australians dying each day – or 20 times what we’re currently experiencing.

All up, U.S. stocks were down for the second week in a row, with the pullback in the S&P 500 now just over 2% from recent record highs. Yes folks it’s still only 2%!

As for this week’s Fed meeting, most economists don’t expect the Fed to formally announce and begin bond tapering – this still seems more likely in November. That said, another potential jolt from the meeting could come from the revised ‘dot plot’ of voting Fed member expectations for the Fed funds rate over the new two years. At present, only 7 of 18 members have pencilled in a rate hike next year (the rest are in 2023), but – given the recent uplift in inflation – there’s a risk that a majority could move into the 2022 camp next week, which could undermine Powell’s pledge to keep interests rates low for a long time. One potentially confusing market outcome next week would be the dot plots suggesting a rate hike next year, with Powell again playing down the significance of the plots in his press conference.

The other issue simmering in global markets is the slowdown in the Chinese economy and exposed vulnerability of debt-laden property companies such as Evergrande. The issue this week is whether Evergrande will manage to meet scheduled interest payments, formally default, of somehow be bailed out by the Government. So far at least, global financial contagion remains contained – helped by the fact it is mainly Chinese creditors at risk.

Australian market

The most notable local market development last week was the further slump in iron-ore prices on the back of China’s continued clamp down on steel production and mounting concern over the property sector. In turn, that has seen local resource stocks underperform relative to financials. RBA Governor Phil Lowe notably chastised the market for pricing in rate hikes in 2023 – he still reckons it will take until 2024 for decent gains in wages and prices.

We also learnt that lockdowns over August saw the loss of 143k jobs, though as most did not bother looking for alternative work they were not treated as unemployed! In fact, the unemployment rate bizarrely slumped to 4.5%. Meanwhile, the latest reports on business and consumer sentiment held up impressively well, with everyone still hoping the lockdowns will end soon.

There’s little local data this week and even the RBA policy minutes should not throw up any surprises. Instead local investors will be watching developments in China and the U.S. with keener than usual interest.

Have a great week!