Global markets

- What can stop the global equity market? Exhaustion? Global investors worried over the weekend before last about the spread of the delta COVID variant and sold down stocks last Monday. By Tuesday, however, they’d changed their minds and a ‘buy the dip’ mentality re-emerged. The S&P 500 rose 2% over the week, while the tech-heavy NASDAQ-100 rose 2.9%.

- Continued solid global economic growth – in both the U.S. and Europe – helped reassure investors, as did the the ongoing strong U.S. Q2 earnings reporting season. Technology stocks were popular last week, I suspect in anticipation of solid earnings reports from heavyweights such as Apple, Microsoft, Facebook, Alphabet and Amazon this week. So it would not surprise if we see these names pop higher when they announce results this week.

- Central banks also remain market-supportive, with most looking through the recent lift in inflation and pledging to keep policy accommodative. Last week the European Central Bank effectively edged its inflation target higher, which means it is even more likely to keep rates near zero for several more years and might even announce more bond buying in the next few months. While the Fed is inching closer to tapering its bond purchases, it won’t happen at this week’s Fed meeting – and when it does I expect the move will be constructed in a way to minimise market concern.

- This week the likely global focus will be the Fed meeting and tech earnings reports – though delta’s spread will also continue to be watched warily. There’s also Q2 U.S. GDP which is expected to be strong (8% annualised growth) and another likely high June consumer price deflator reading on Friday which the market will dismiss because the Fed is. Indeed, we’ve already have the high June CPI result which the market ignored.

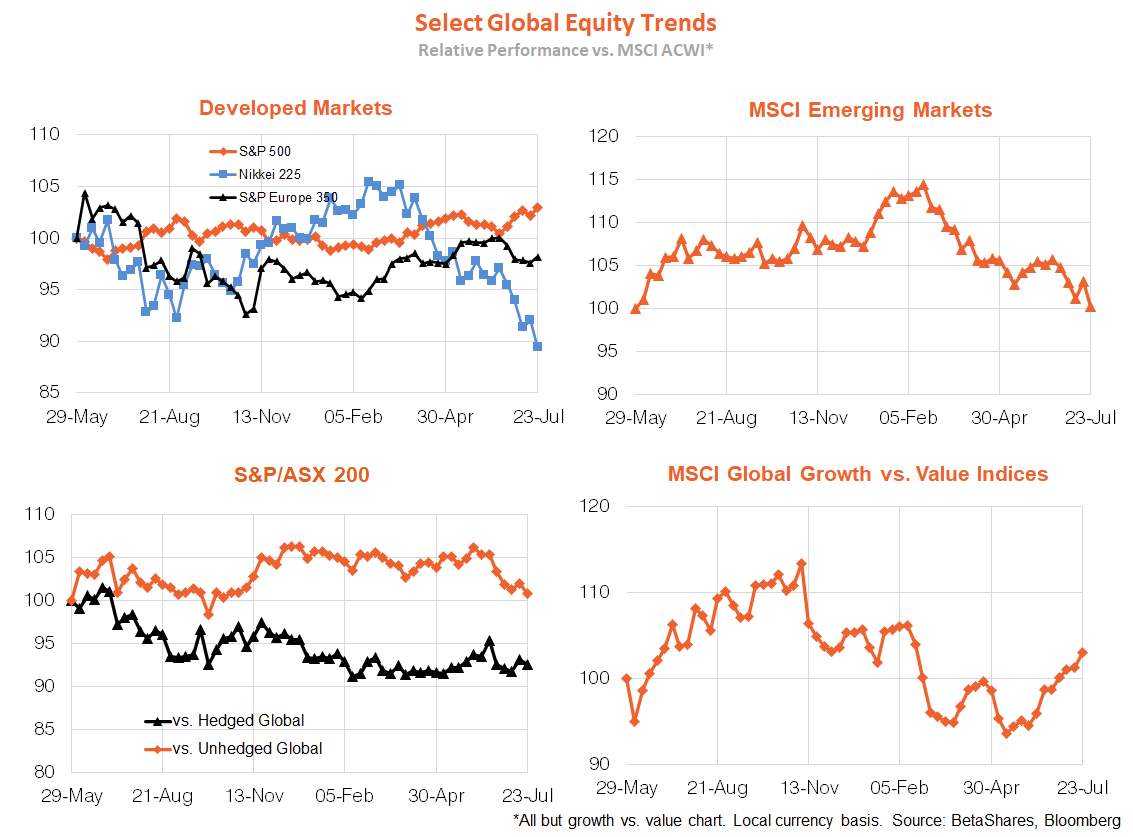

- In terms of major trends, the downtrend in bond yields remains in place which has supported a rotation back to growth over value, and developed over emerging markets. Despite the Olympics, Japan’s performance has taken a hit in recent months, thanks to the re-emergence of COVID.

Australian market

- The S&P/ASX 200 rose a more modest 0.6% last week though will likely benefit this morning from Friday’s gains on Wall Street – despite much of the country being stuck back in lockdowns. Indeed, Q3 GDP is now shaping up to be downright ugly, yet markets have learnt to look through the weakness and focus on the likely Q4 re-opening. Such sentiment will be supported by the fact that the RBA now seems even less likely to taper its bond purchases in September – though I really struggle to get excited over whether the Bank will buy $1 billion or less of bonds each week. At best, QE today is presentational window dressing designed to make the RBA look as if its doing something when it really can’t do much more.

- The good news is that states other than NSW could emerge from lockdowns within days if not a week or so. In NSW, where the virus has had more time to spread, the outlook remains bleak – zero community delta transmission and a ‘soft lockdown’ appear incompatible goals, and until either one is forsaken Sydney’s lockdown risks dragging on indefinitely.

- In terms of the week ahead, we get the Q2 CPI on Wednesday. While the headline annual rate is likely to spike higher due to higher energy costs (3.8% from 1.1%), the underlying trimmed mean measure should rise by a lot less (1.1% to 1.6%). Unlike in the U.S., local core inflation remains comfortably benign.