In the current macroeconomic environment, identifying an investment with consistent returns can be difficult to pinpoint. Markets remain volatile, with the recent banking crisis adding to the looming risk of a US recession.

Backed by the full faith and credit of the US government, treasuries are considered among the safest investment assets on earth. US Treasury Bills, also known as T-Bills, are US government debt obligations with maturities of one year or less.

Savvy Australian investors are using T-Bills to diversify their portfolios, reduce risk and gain exposure to the US dollar.

Investing in T-Bills

Investing in T-Bills is essentially a loan between an investor and the US government. The investor, in this instance, is lending to the US government. For the length of the term, the investor is agreeing to lend the US government money in the form of the T-Bill.

Since they offer such short maturities, T-Bills don’t pay interest in the form of coupons like other bonds. Instead, they’re called ‘zero-coupon bonds,’ meaning that they’re sold at a discount and the difference between the purchase price and the par-value at redemption represents the interest.

Investors can also sell T-Bills before they mature and there is a huge market for these because of the market’s confidence in the issuer and their short-term profile. According to the most recent1US Treasury Monthly Statement of the Public Debt, there were US$3.9 trillion worth of T-Bills outstanding. For investors who value liquidity this is a key selling point.

T-Bills are a popular investment right now because of recent notable jumps in their yields following several rate hikes by the US Federal Reserve. Currently, T-Bills’ yields are higher than longer-term yields due to an inverted yield curve. Many market participants expect the US Federal Reserve to continue to raise rates while inflation remains high.

In fact, many T-Bills are currently offering yields in excess of 5%, high for a defensive asset and a difficult return to beat in current market conditions. We believe yields should continue to remain high while inflation persists.

But don’t take our word for it, the bulk of Berkshire Hathaway’s cash – more than US$100 billion – sits in T-Bills. According to Barron’s, Berkshire Hathaway CEO Warren Buffett likes the security of T-Bills versus other short-term investments. Buffett says that Berkshire Hathaway is now earning US$5 billion annually on its cash, up from US$40 million when rates were near zero.

What about the US debt ceiling issues and the chance of default?

President Biden cancelled his scheduled trip to Australia and Papua New Guinea to negotiate the US debt ceiling.

There has been a lot of noise about this. Mostly political.

Noted bond investor, Bill Gross recently advised investors buy T-Bills to bet the current US debt-ceiling issues will be resolved. “It’s ridiculous. It is always resolved, not that it is a 100% chance, but I think it gets resolved,” Gross said on Bloomberg Television’s ETF IQ. “I would suggest for those who are less concerned, similar to myself, that they buy one-month, two-month Treasury bills at a much higher rate than they can get from longer-term Treasury bonds.”

So, while a ‘default’ is not out of the question. Let’s look at the ‘default’ properly. This episode, should it eventuate, will not be like the Greek Default or an Argentinian Default, where bond values are written down to be close to zero. The US is not insolvent.

There is a precedence for this US ‘default’. The US defaulted in 1979 when Congress didn’t legislate in time to raise the debt ceiling. This resulted in three late payments, not outright defaults:

- 26 April 1979, the US Treasury defaulted on US$41 million of maturing T-Bills. They were paid 20 days late on 17 May 1979.

- 3 May 1979, the US Treasury defaulted on another US$40 million of maturing T-Bills. These were paid 14 days later.

- 10 May 1979, the US Treasury defaulted on yet another US$40 million of maturing T-Bills. These were paid 7 days late on 17 May 1979.

The result of these ‘temporary’ defaults did shock many investors who, up until that time, believed that the US government would always pay its debts on time. It is important to differentiate between a full debt default and failing to meet a payment when it is due.

The US still has plenty of money and the US dollar remains the dominant trading currency. The primary problem appears to be politics.

Why T-Bills are considered a safe haven asset

The US Government remains highly rated by Fitch, S&P and Moody’s. Historically, when confidence has eroded or when volatility has spiked in financial markets, investors have gravitated towards short-term US T-Bills.

Currently many investors are looking for portfolio defence as inflation remains high and markets are volatile. Improving the credit quality of the fixed income allocation of an investment portfolio can help build a more defensive portfolio structure.

Gain exposure to the US dollar

For Australian investors, exposure to liquid US T-Bills offers exposure to the US dollar and a potential hedge against systemic or market episodes.

Last week, VanEck launched a short-term US T-Bill ETF on ASX. It has the ticker TBIL. TBIL is Australian dollar unhedged and has been specifically designed this way with local investors in mind.

The fund is $A unhedged to give investors exposure to the US dollar (USD). The USD exposure offered in TBIL may provide Australian investors with capital appreciation during periods of economic weakness. Historically, during periods of economic uncertainty or weakness the Australian dollar has lost value relative to the US dollar because it is considered a “risk on” currency while the USD is considered “risk off.”

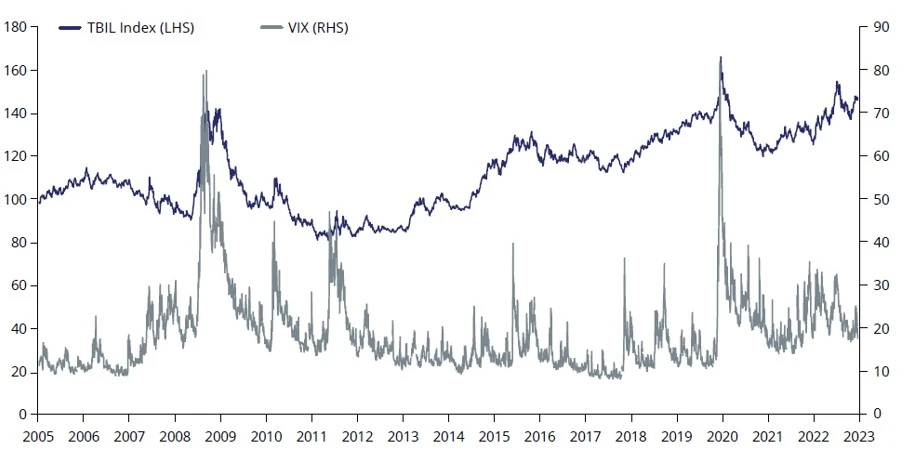

You can see this in the chart below which shows that an unhedged AUD exposure to T-Bills has experienced positive returns when market volatility increases, as represented by the VIX index. The Chicago Board Options Exchange’s CBOE Volatility (VIX) Index is a measure of the stock market’s expectation of volatility based on the S&P 500 index.

Source: Bloomberg, VanEck Source: VanEck, Bloomberg. Chart shows performance of Bloomberg U.S. Treasury Bills: 1-3 Months Unhedged AUD Index (TBIL Index) compared to VIX Index. You cannot invest in an index. Past performance is not a reliable indicator of future performance of the index or TBIL.

TBIL gives investors access to short-term US treasury bonds via the efficiency of an ETF. TBIL pays dividends monthly.

Key risks: There are risks associated with an investment in TBIL. These include but are not limited to interest rate movements, currency, bond markets generally, issuer default, credit ratings, country and issuer concentration, liquidity, tracking an index and fund operations.