The Mario Bros movie opened last week and it did big business, breaking box office records. But the biggest video games releases make far more money than biggest movies releases. The highest grossing video game of all time, Dungeon Fighter Online has grossed US$20 billion. Avatar, the highest grossing movie made $2.9 billion. Video games can be lucrative, so far in 2023 the companies that make up VanEck Video Gaming and Esports ETF (ESPO) have had a winning start.

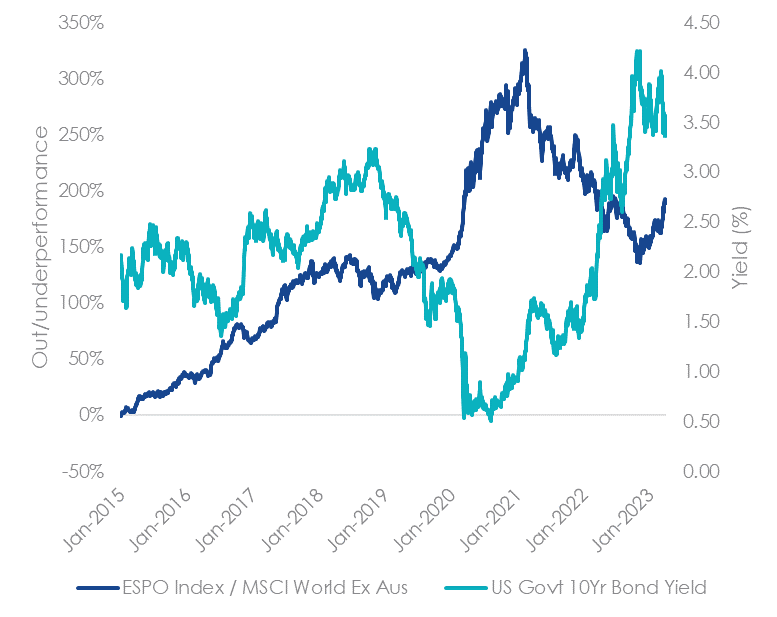

With macro headwinds in the market at the moment, communication services and information technology companies including esports and video gaming has quietly gone through a strong rebound following a drop in the US 10-year bond yields. You can see in Chart 1, when the dark blue line is rising, the companies in the MVIS Global Video Gaming and eSports Index (ESPO Index) are outperforming the MSCI World ex Australia Index. ESPO Index’s outperformance, in the past has correlated to a falling US 10-year bond yield.

ESPO, which tracks the ESPO Index, generated 23.83% for the past quarter, outpacing MSCI World Ex Australia Index (9.20%) and tech-heavy Nasdaq 100 (22.20%)[1].

Chart 1: ESPO Index outperformance and US 10-year bond yields

Source: Bloomberg as at 4 April 2023. Past performance is not indicative of future results. You cannot invest directly in an index. ESPO’s Index base date is 31 December 2014. ESPO Index performance prior to its launch on 14 August 2020 is simulated based on the current index methodology.

Goldman Sachs suggests a few key themes arising in the sector. Firstly, mobile gaming showed an upside surprise after 12-18 months of Apple privacy induced headwinds. On the other hand, consumer behavior around PC/console games became more volatile in December as more mature/scaled games outperformed inside a weaker spend environment. Probably because the uncertain environment, many companies such as NCSOFT, delayed their highly anticipated titles from 2022 to 2023. According to NewZoo’s estimates, the PC and console games worldwide generated $92.3 billion in revenue in 2022, 2.2% drop from the year before due to fewer console releases. While there is a correction from the pandemic highs, the market is in a healthy state and is on track to grow further.

There are also some bright spots. The US semiconductor names NVIDIA (+92.58% in AUD terms, quarter ended 31 March 2023) and AMD (+53.29% in AUD terms, quarter ended 31 March 2023) have run significantly in the past reporting season. In particular, Goldman Sachs says NVIDIA could see acceleration in growth and expanding margins supported by strong sequential growth in the Data Center business and cyclical strength in gaming, while AMD has attractive valuation, particularly on a growth-adjusted basis.

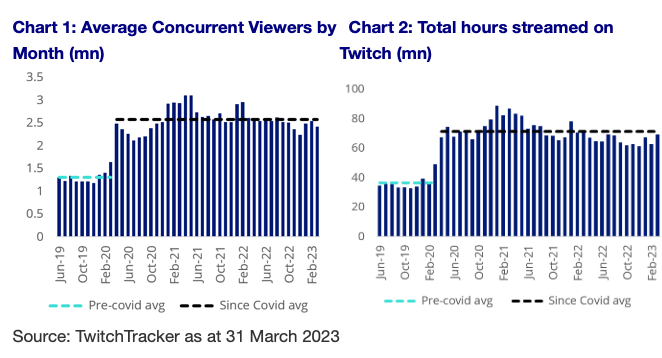

TwitchTracker data suggests that viewers of game streaming and total streamed hours remain above pre-pandemic levels. We think the esports industry will continue the secular growth trend in the years to come.

There is some good news coming from the Chinese gaming/tech companies as its regulatory environment Improves. Bilibili’s localised version of “Uma Musume: Pretty Derby” was given the green light in the latest batch of approvals for 27 imported games, according to a list published by China’s online gaming regulator. Tencent and NetEase also received approvals for one game each. According to Bloomberg, the latest batch of approvals for imported titles came just three months after the last one, as authorities ease constraints on the video-game sector.

Table 1: ESPO performance to 31 March 2023

| 1 Month (%) | 3 Months (%) | 6 Months (%) | 1 Year (%) | Since ESPO Inception (% p.a.) | |

| ESPO | 14.21 | 23.83 | 31.75 | 7.59 | 2.78 |

| NASDAQ 100 | 10.27 | 22.20 | 15.72 | 0.24 | 10.94 |

| Difference | +3.94 | +1.63 | +16.03 | +7.35 | -8.16 |

ESPO Inception date is 9 September 2020

Source: Morningstar Direct, VanEck. The above table is a comparison of performance of ESPO and a market capitalisation technology index. You cannot invest directly in an index. Results are calculated to the last business day of the month and assume immediate reinvestment of distributions. ESPO results are net of management fees and other costs incurred in the fund, but before brokerage fees and bid/ask spreads incurred when investors buy/sell on the ASX. Returns for periods longer than one year are annualised. Past performance is not a reliable indicator of future performance. The NASDAQ 100 is shown for comparison purposes as the market benchmark for non-financial securities listed on the NASDAQ Stock Market. The NASDAQ 100 is a modified market capitalisation index heavily allocated towards top performing industries such as technology, consumer services, and health care. ESPO tracks an index which aims to represent the overall performance of companies involved in video game development, eSports, and related hardware and software globally. Consequently ESPO has fewer companies and different sector allocations than the NASDAQ 100.

[1] Source: Morningstar Direct, quarter ended 31 March 2023. As always, past performance is not indicative of future performance.

Want to know more about ESPO or the video gaming and esports industry? Find out here.

Key risks

An investment in the ETF carries risks associated with: ASX trading time differences, emerging markets, financial markets generally, individual company management, industry sectors, foreign currency, country or sector concentration, political, regulatory and tax risks, fund operations, liquidity and tracking an index. See the PDS for details.