Global markets

- Global equities continued to grind higher last week reflecting ongoing solid corporate earnings and still relatively benign bond yields. Indeed, lingering fears with regard to the potential impact of delta on economic growth are likely helping offset fears which may otherwise have arisen from strong U.S. economic growth and associated interest rate fears.

- The lower than feared U.S. core CPI result last week helped support sentiment and was consistent with the emerging view that inflation fears have peaked. That said, Fed speakers again flagged a likely tapering announcement late this year, which must by now be close to fully priced into the market. Talk of further U.S. fiscal stimulus also remains the ‘gift that keeps on giving’ with the Senate passing a US$500m infrastructure bill, only for the Democrat-controlled lower house to hold back on agreeing – in the hope of forcing the Senate to agree on an even larger US$3.5 trillion budget package.

- As evident in the chart set below, U.S. stocks are trending up and U.S. long bond yields and the US dollar are still trending sideways/down. Gold remains in a downtrend and oil has pulled back from highs in early July.

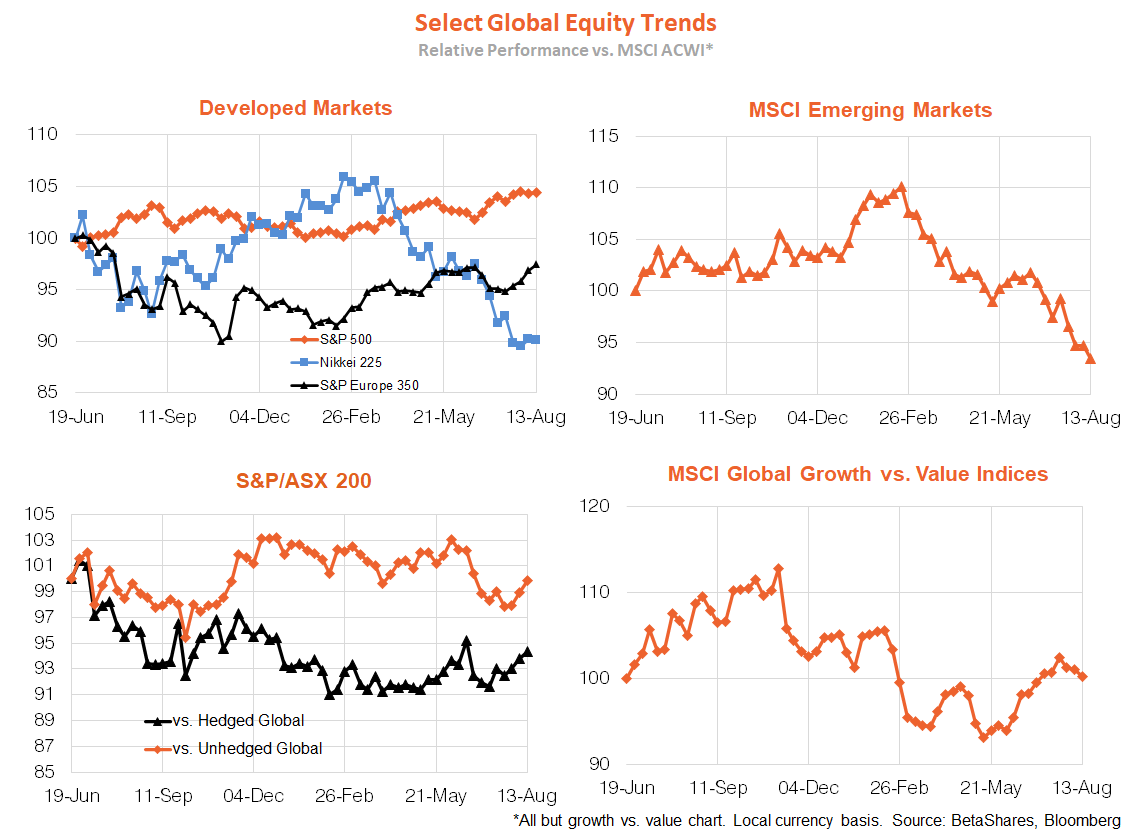

- In terms of global equity trends, emerging markets remain on the nose while Europe’s outperformance since late February has come at the expense of Japan. U.S. relative performance continues to grind on, while Australian relative performance is fairly flat. Value has staged a mini comeback versus growth in recent weeks perhaps reflecting easing fears with regard to delta.

Australian market

- The S&P/ASX 200 lifted further last week, confirming a break higher in the past two weeks after several weeks of sideways consolidation. At the same time, local bond yields remain contained and weaker iron-ore prices have helped push down the $A. Relative key ETF sectors performance (financials, resources and technology) remains quite mixed.

- The local equity market strength is admirable in the face of lockdowns across the country and also notable drops in both business and consumer sentiment last week. This is another example of the market looking forward and remaining focused on a Q4 re-opening bounce-back in the economy once vaccination rates are high enough. It also helps that we are moving through a bumper earnings reporting season with major corporate dividend and share buyback announcements.

Week ahead

- Global markets will on Wednesday digest minutes from the July Fed meeting, which is expected to keep Q4 tapering talk simmering along. Washington stimulus talks will also remain in focus – note no deal is likely neutral for the market, while a deal would be great news. Major U.S. retailers also report earnings which are likely to be strong.

- In Australia, the Q2 wage cost index on Wednesday is likely to show still only tepid wage growth. Reflecting lockdowns, the July labour market report on Thursday should show a major slump in employment – market consensus is a decline of 50k! Much, however, will depend on the extent to which the hit is taken through lower working hours instead of jobs shed.

- Today China will release its monthly ‘data dump’ covering retail sales and industrial production. Amid renewed talk of China slowing, a weak set of numbers could put further near-term downward pressure on iron-ore prices and the $A.

- Last but not least, the Reserve Bank of New Zealand is widely expected to lift rates by 0.25% on Wednesday – the first major developed economy to do so since the COVID crisis – reflecting surging house prices and its strong economic bounce back.

Have a great week!