The value investment style is showing increasing signs of emerging from a long period of hibernation. We may now be seeing a sustained return to favour for many good quality companies previously shunned amid the momentum-driven mania of recent years.

It has been a long and frustrating wait, but there now appear to be clear indications that the sharemarket is increasingly beginning to value companies on the basis of their fundamentals, and we are beginning to see this play out for many of the companies in Investors Mutual’s portfolios. This is a very welcome development for the many investors who have been patient with us for a number of years as our quality-focused approach to investing has meant that the performance of our funds has lagged the market.

The Australian sharemarket has in recent years been driven by a momentum theme. As share prices for certain companies were bid up, this attracted attention from other buyers, leading to behaviour predicated on the assumption that the share prices for these companies would continue to increase indefinitely – as opposed to investing on the basis of sober analysis of the long-term fundamentals underpinning the companies.

The dislocation between the intrinsic value that can be assessed using fundamental analysis and the value that the market has ascribed to a number of companies has become very pronounced, and the prices for some companies became extremely difficult to justify on the basis of their fundamentals. This speculation was supercharged by the massive amounts of stimulus injected into the local and global economies as a result of the low interest rates which existed before the onset of the COVID-19 pandemic a year ago, and then by further central bank interest rate cuts and quantitative easing and government support payments and initiatives to boost economic activity.

As we have discussed on a number of occasions in recent years, it has been a tough period for a disciplined, fundamental investor like IML watching the market bid up prices for many of these speculative stocks, while many of the companies in our portfolios – solid, well-established businesses with track records of consistent earnings and leading positions in their industries – were overlooked. These included many long-held cornerstones of our portfolios such as Amcor, Brambles, Crown Resorts and Tabcorp.

(This dislocation between our assessment of companies’ intrinsic values and the value the market has been attributing to those companies in the form of lower share prices has however enabled us to use our in-depth research to buy in or increase our holdings in a number of very good quality companies at extremely attractive prices.)

As the local and global economies continue to reopen and life returns to some sort of post-pandemic normality, investors have become increasingly concerned about the prospect of inflation, and bond yields have risen accordingly. The US 10-year government bond yield – a proxy for interest rates around the world – has risen from an all-time low of 0.52% in July 2020 to around 1.6% at the time of writing. This has had consequences for the speculative companies, which have benefitted enormously from the justification of using all-time low discount rates to ratchet up valuations. Investors are now finally reassessing the risk in the market, and also re-evaluating the overinflated valuations which had previously been ascribed to many of these businesses on the basis of the perception of their high growth potential.

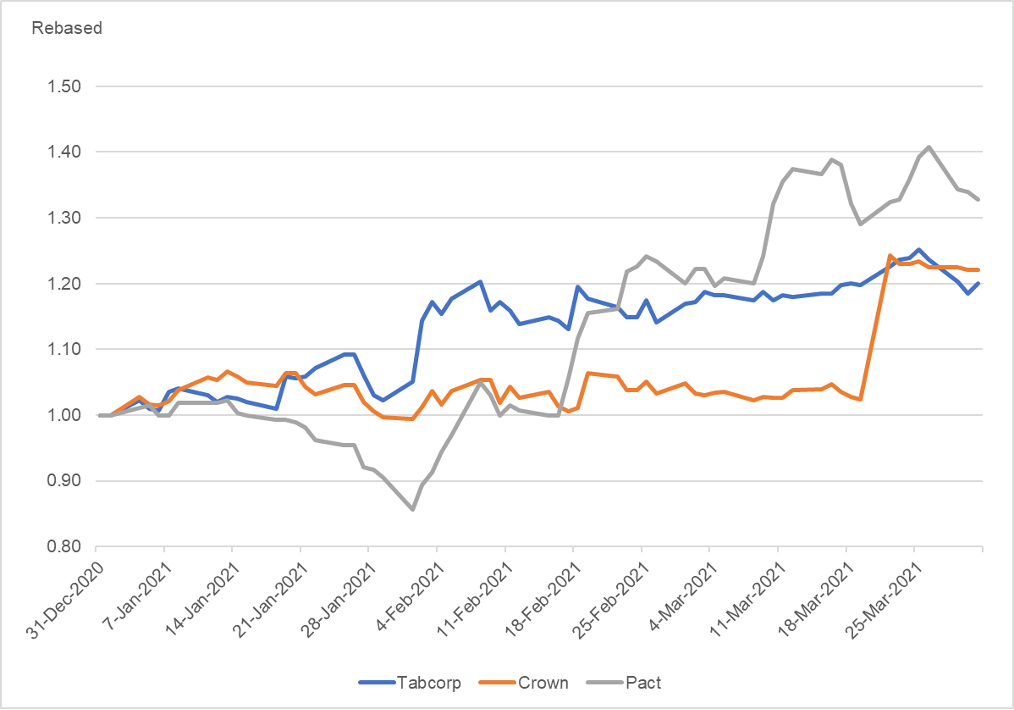

With bond yields rising, and by extension the equity risk premium increasing, the steam is coming out of many of the speculative leaders of recent years, and a number of companies in our portfolios are now benefitting from this return to a greater focus on fundamentals in investing. Many of these companies held were underappreciated going into the most recent profit reporting season, and as a result of announcing good results, have been re-rated by the market. The share price of Pact Group, for instance, rallied significantly on the back of a solid result.

This greater focus on company fundamentals has also led to an increase in the level of merger and acquisition activity, which has supported the share prices of a number of companies in our portfolios. Crown Resorts, for instance, rallied sharply off the back of the approach from private equity group Blackstone, while Tabcorp’s share price has similarly benefitted from the approach for its wagering business from Entain. The following chart shows the increases in share prices over the March quarter for Crown, Pact, and Tabcorp.

Chart 1: Increases in Share Prices of Crown Resorts, Pact Group, and Tabcorp, 1 January – 31 March 2021

Source: Iress, 16 April 2021. Share prices have been rebased to a nominal $1 starting point

Despite the rallies we have seen to date, many stocks in our portfolios still look undervalued and continue to offer attractive dividends.

As always, we continue to own and top up our holdings in good quality companies that are often out of favour in the short term but which we believe have an enduring competitive advantage, have track records of generating recurring revenues and earnings, are run by competent and honest management teams – companies like Orica and IAG. We believe these types of companies are significantly undervalued on a long-term basis, and that they should benefit from sizeable re-ratings of their share prices over the next three to five years as the turnaround in earnings occurs.

Although market conditions have not always been in our favour, focusing on the fundamental value and quality of companies has enabled us over our 23 years of existence to deliver reliable income and long-term capital growth to our investors, while achieving returns which are more consistent and less volatile than the overall sharemarket. We believe that our portfolios are well-positioned to perform well going forward, given the attractive valuations of many of the stocks we own, which we believe will do well over the next three to five years. We also continue to shun many of the high-flying stocks which will come down to earth very quickly at some stage when common sense returns.

While the information contained in this article has been prepared with all reasonable care, Investors Mutual Limited (AFSL 229988) accepts no responsibility or liability for any errors, omissions or misstatements however caused. This information is not personal advice. This advice is general in nature and has been prepared without taking account of your objectives, financial situation or needs. The fact that shares in a particular company may have been mentioned should not be interpreted as a recommendation to buy, sell or hold that stock. Past performance is not a reliable indicator of future performance.