by Adam Kibble – Fund Manager

Unlike the popular video app TikTok, investing is a long term endeavour that rarely provides instant gratification. We need to keep reminding ourselves that monetary policy operates with long and variable lags as we wait patiently for the cumulative effects of the fastest monetary policy tightening cycle since the 1970’s to impact economic growth.

Patience is a virtue! How many times was I told that in my youth? Well, patience in investing is a very important discipline to maintain. Never more so than now, as we wait patiently for the cumulative effects of the fastest global monetary policy tightening cycle since the 1970’s to impact economic growth. The Reserve Bank of Australia is well aware of the long and variable lags of the impact of previous monetary policy decisions; that’s why, after a cumulative 3.5% lift in official rates since May last year, they paused the tightening cycle and kept rates stable in April. Upon reading the RBA meeting minutes about that decision, the pause looked to be temporary as they stressed the desire to wait and assess more economic data for signs of the impact of their previous decisions.

Well apparently, one month of patience is enough and despite the March quarter inflation data confirming that Australian inflation has likely peaked and is heading lower, the RBA lifted rates in early May to 3.85%, as they remain concerned about tight labour markets and wage rises filtering through to inflation. One wonders why they paused at all? What are the implications for our investment strategy in the Schroder Absolute Return Income Fund? None really; we have been shifting to a more defensive strategy for some time and the RBA’s policy decision provides us with more conviction in that strategy, as higher short-term rates get inflation under control but something in the economy breaks in this process.

Business cycle in decline

Our investment framework relies on three pillars: Valuations, Business Cycle and Liquidity, and we assess new information as it impacts each of those pillars. The business cycle is now clearly in decline with growth below trend, and central bank policy continues to be a cyclical headwind, as fighting inflation is prioritised over promoting growth. The RBA’s message to the markets has been consistent and it was reiterated following the latest rate rise: “the Board’s priority remains to return inflation to target”, but they also confirmed that “the path to achieving a soft landing remains a narrow one”.1 Due to the lags in the impact of changes in monetary policy, our view for some time has been that there is a risk that the RBA overtightens policy and tips the economy into recession – they clearly recognise the difficult task ahead to achieve their policy goal of bringing inflation back to their target band without causing a recession.

The global backdrop is also not supportive for the Australian economy. Our US recession indicator has been flashing red for 12 months now, with 65% of the indicators signalling recession. US employment, a lagging indicator, is starting to show some cracks. Although the headline unemployment rate remains at a historical low of 3.5%, initial jobless claims are now starting to rise, finally correlating with other negative labour market signals. We therefore expect the unemployment rate to increase over the remainder of the year.

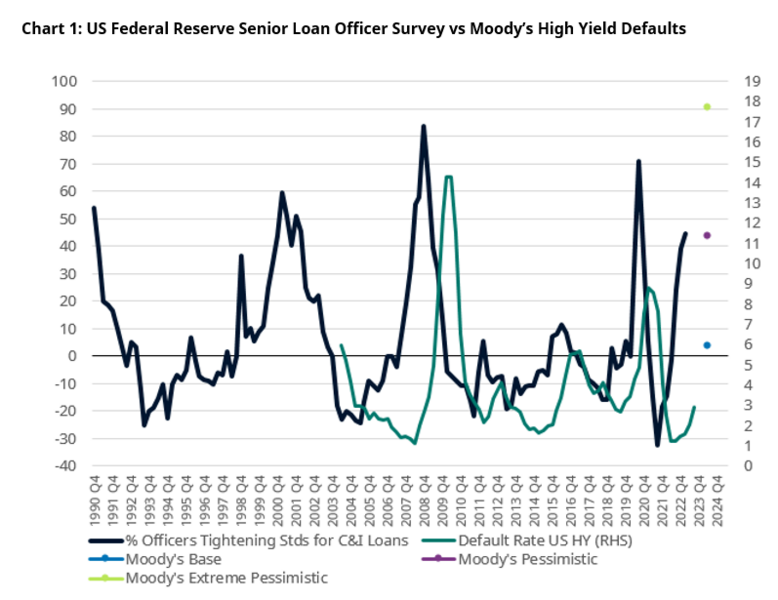

US lending standards tighten

We also remain in the midst of a US regional banking crisis, which is a direct consequence of the Federal Reserve’s policy actions. This will likely lead to a further tightening in lending standards by US banks which will restrict access to credit to the riskiest borrowers. Bank lending standards have already increased and are consistent with levels prior to past recessions. The chart below shows a FED survey of the percentage of senior loan officers tightening lending standards and the US high yield default rate. The latest survey was conducted prior to Silicon Valley Bank being closed by US regulators, but shows a significant tightening in lending standards was well underway and consistent with a significant increase in the default rates for the most risky corporate borrowers. The next senior loan officers survey is due out in early May and we expect confirmation of a further tightening of lending standards.

Source: US Federal Reserve. Moody’s Investors Service.

On the positive side, China remains the great hope for Australia to avoid recession. Australia is fortunate in that our largest trading partner is growing strongly. The latest quarterly GDP report shows annualised growth at 4.5% and forward expectations remain strong. This is despite external headwinds (from global trade) as the domestic economy is improving thanks to the release of pent-up demand following the reversal of their zero-COVID policy in late 2022. In addition, because inflation remains low in China, the policy environment has greater flexibility to be supportive for domestic growth.

Stepping back from credit as the honeymoon ends

Over the past few months, our strategy has been shifting to increasing duration risk and reducing credit risk as the balance of probabilities, in our view, shifts towards a recession in the US and Australia. We have been reducing exposure to credit, particularly higher risk credit, as we believe the riskiest borrowers will struggle to refinance their debt as lending standards tighten. This is an intentional consequence of tighter monetary policy. Credit availability will be restricted to both households and corporates that have high debt loads and reduced capacity to service that debt. The credit binge honeymoon is over and we are entering a period of deleveraging. Current credit spreads for non-investment grade issuers are insufficient to compensate investors for the level of defaults that typically occur in a recession, so we have cut all exposure to high yield credit and have implemented hedges via credit derivatives in high yield to reduce overall portfolio credit risk.

We have been increasing duration exposure whenever yields back up. Duration has increased to 1.5 years, from 0.7 years at the end of last year and we expect to increase further as opportunities present. Thus far, we have favoured longer-dated maturities to gain duration exposure in both the US and Australia as shorter maturities are still exposed to further policy tightening. Again patience is required, but we expect yields to eventually decline as inflation continues to fall towards 3% to 4% and growth turns negative.

We have recently increased foreign currency exposures by adding a 2% position in the Japanese yen (JPY) to diversify our currency exposures. Historically, the yen has performed well during cyclical declines, particularly against the Australian dollar, and together with a 2% exposure to the US dollar (USD), provides a downside risk hedge (alongside our higher duration exposure) against further weakness in credit spreads. In addition, the yen remains very cheap historically and we patiently wait for the new Governor of the Bank of Japan to begin the process of dismantling their yield curve control policy which is keeping real rates very negative. This should lift Japanese bond yields and the yen.

Patiently remaining patient

In summary, the portfolio remains very defensively positioned as we expect to see the negative impact of slowing growth on equity prices and higher risk credit over the coming months. The Schroder Absolute Return Income fund is a liquid, defensive income strategy with an objective to protect investor capital from drawdowns over one-year periods. Consistent with that objective and our macro outlook, our preference is to forego the higher yields on offer from non-investment grade credit and position the portfolio to avoid potential losses from credit issuers in the recession scenario. But how do we achieve our other objective of returns of cash plus 2% at the same time? Well in the short term it’s a more difficult task we have set ourselves, so we need to remain patient; we are positioning longer in duration with diversifying exposure to foreign currency; both of these exposures should benefit if our base case of recession is realised, with gains accruing from both lower bond yields and depreciation in the Australian dollar. To assist, we have maintained exposure to mostly Australian investment grade credit, where default rates are low and the yield premium above government bonds provides a good buffer of income to support returns as we wait patiently for the impact of monetary policy tightening.

- RBA monetary policy statement, 2 May 2023