by Hamish Chamberlayne, CFA and Aaron Scully, CFA

For many years, the US has been perceived as a laggard, or even at times an obstruction, to the global pursuit of sustainability. With the US currently standing as the second-largest emitter of greenhouse gases (GHGs), its contribution to a global reduction in CO2 emissions is essential. But could President Biden’s new Inflation Reduction Act put an end to this uncomfortable truth?

Inflation by name, sustainable by nature

By name, the Inflation Reduction Act (IRA) may imply intentions to curb inflationary pressures caused by the hangover from pandemic-related fiscal and monetary policy, supply shortages and the Russian invasion of Ukraine. By nature, however, it is easy to identify a distinct sustainability-driven agenda nestled between the pages. We have long drawn parallels between a sustainable economy and achieving economic resilience, and we are pleased that the world’s most influential government views the need for economic security and addressing the climate emergency as one in the same.

Among the key areas of focus are lowering drug, healthcare and energy costs, with the intention to “build an economy that works for working families”. Interestingly, the details of the act include USD$400 billion of funding towards green activities, incentives to US homeowners to invest in electrical upgrades and insulation, specific provisions around tax free credits for electric vehicles (EVs) and regulatory clarity around the renewables sector.1 A statement from the White House referred to the Inflation Reduction Act as “the most aggressive action on tackling the climate crisis in American History”, aligning the US to the Paris Agreement.

What does the IRA mean for the global climate agenda?

How the US behaves impacts the bigger picture. It is the largest economy and the second largest emitter of GHGs behind China, accounting for nearly 13% of global emissions, and remains among the highest emitters per capita.2 With the urgency of climate change more pressing than ever, could the IRA catalyse a downward trend in US emissions and contribute towards driving global emissions in the right direction?

The use of renewable energy is essential to meet climate targets, with some reports suggesting that global renewables growth must double in order to meet the Paris Agreement goals.3Today, renewables are the cheapest forms of energy in countries that constitute two thirds of the global population and 75% of global GDP.4 Despite this, renewables account for only 12% of total energy consumption and 20% of electricity generation in the US.5 The Act is expected to progress clean energy in the US through infrastructure funding and federal tax cuts intended to increase wind and solar, clean hydrogen and zero emission nuclear power production.

Impressively, new build onshore wind and solar is cheaper than running amortised coal and gas power plants for 58% of the world’s population, representing two-thirds of energy generation.4 If the positive impact of clean energy was not enough, an improved renewables capacity would also stand to significantly lower energy costs, thereby reducing inflation – a win for people’s pockets and for meeting climate goals.

What does the IRA mean for the economy?

Energy is the engine that drives GDP; it is the foundation on which all productive economies rest. One barrel of oil alone contains six gigajoules of energy – enough to provide electricity consumption for the average US home for nearly two months.6 However, recent events highlight that traditional energy methods are simply no longer sustainable in the developed world. Divergent geopolitical regimes have shattered globalised energy markets and the climate crisis is more severe than ever. As a result, reshoring and redefining strategically important industries will be fundamental to creating an energy independent and sustainable economy.

With the next capital investment cycle long overdue, we believe that the IRA marks the beginning of the end of fossil fuels in the world’s largest economy. Today’s period of higher inflation provides a financial incentive for companies to invest in productivity, substitution and efficiency. The old model of resource arbitrage and global supply chains should naturally make way for a new economic model built upon clean, locally sourced energy and more efficient infrastructure. This should create jobs, improve economic security and nurture growth. Importantly, the IRA facilitates this change in the US. As Biden has made clear, “when [he] hears climate, [he] thinks jobs.”

It is clear to us that normalising inflation via the IRA hinges on creating a sustainable economy. We believe that both angles of the IRA – climate and growth – present fertile ground for active investors over the next decade.

The reindustrialisation of the US

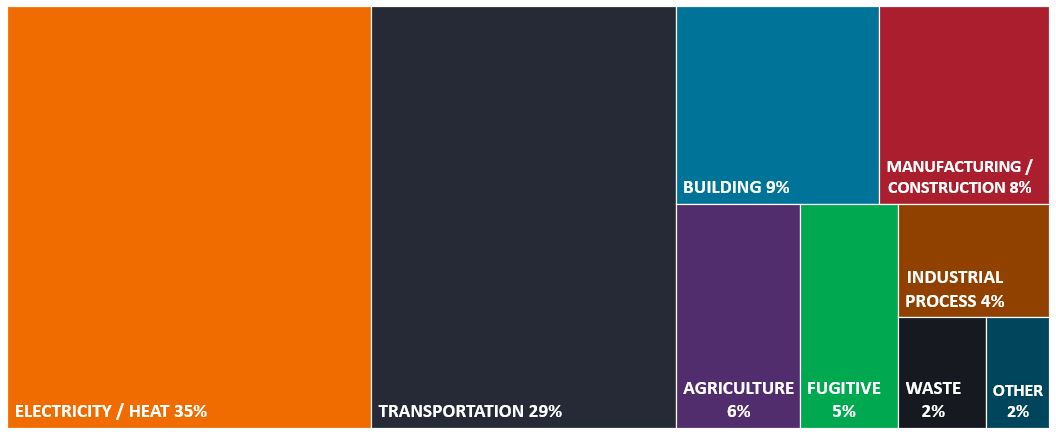

Transportation, building and manufacturing represent the three biggest emitters of GHGs after electricity/heating in the US, presenting enormous opportunity in the transition to clean energy – exhibit 1. Aside from the more obvious areas such as renewable power generation, batteries and electrification of transport, technologies such as the Internet of Things, data centres, communications, factory automation, digitalisation & software, and semiconductors should play a major role in the ‘green’ reindustrialisation of the US.

Exhibit 1: US greenhouse gas emissions by industry

Source: Climate Watch Historical Country Greenhouse Gas Emissions Data, sectoral GHG emissions data from 1990 to 2019.

We find semiconductors to be particularly interesting given their use in increasingly diverse end markets as technology progresses. Once viewed as being narrowly focused on computing end markets, semiconductors are now used across multiple industries to enable digitalisation of a broad array of products and applications. With this in mind, some might consider semiconductors to be more akin to industrials than tech. Either way, it is clear that the line between tech and industrials is blurring. We expect the next capital investment cycle to follow a similar shape, with today’s technology becoming the new foundation of the green industrial revolution.

Reshoring supply chains drives growth

Batteries are necessary to effectively increase the proportion of renewable energy and electrification across the economy. Currently, China dominates the battery industry and is responsible for nearly 80% of all battery production in 2021.7 Specifically, the world relies on China for its cathode power, which is essential for lithium-ion batteries and represents around 50% of the total battery cell cost.8 To encourage domestic EV production and minimise its reliance on China, the IRA seeks to offer big tax credit incentives to the automotive industry if its EV supply chain is completed solely in countries that have free trade agreements with the US. That is, an EV customer will not receive tax credits if the car in question contains materials from China, which does not have the necessary agreements in place.

Outside of China, Quebec in Canada holds all the materials and intellectual pedigree required for battery production. Home to many of the essential components of lithium-ion batteries – nickel, cobalt, lithium and graphite – and with a vibrant university research sector and sturdy regulatory framework it is emerging as the Silicon Valley for batteries. However, it currently accounts for only 10% of US battery demand.9 We believe that the IRA’s tax incentives inspire a compelling growth story associated with the clean development of battery technology, with Canada becoming the cornerstone of North American battery production.

Two birds, one stone

Crises often accelerate innovation, and we believe this is the case in the US. The IRA addresses two issues with one solution by seeking to create a sustainable and more resilient economy. Not only is it the most ambitious piece of climate legislation that the US has ever passed, but it is fully aligned to spurring investment and growth in the US economy. This fits with our long-term thesis, which we have spoken about many times before, focusing on energy independence, economic resilience and supply chain reshoring to create a sustainable global economy.

We believe that the US is on the cusp of a period of considerable value creation associated with a green industrial revolution, with dramatic technological change across multiple sectors. Combined with the relative economic strength of the US, this could present a great opportunity for investors.