by Dr David Allen

The idea that a fund manager must hold a concentrated portfolio to significantly outperform the benchmark is an enduring investing legend.

However, when you look at the data, this widely held conclusion seems somewhat questionable. Afterall, Renaissance Technology, the most successful hedge fund of all time has generated returns in excess of 70% p.a. before fees and has several thousand positions at any one time.

So, let’s dig in a little deeper.

Have concentrated managers generated superior performance to diversified managers on average over time?

The star manager effect

For decades, the idea of the “star fund manager”, with a perceived extraordinary ability to identify the super compounders hiding in plain sight, has reigned supreme.

Typically, the portfolios of star managers have been concentrated with less than fifty holdings.

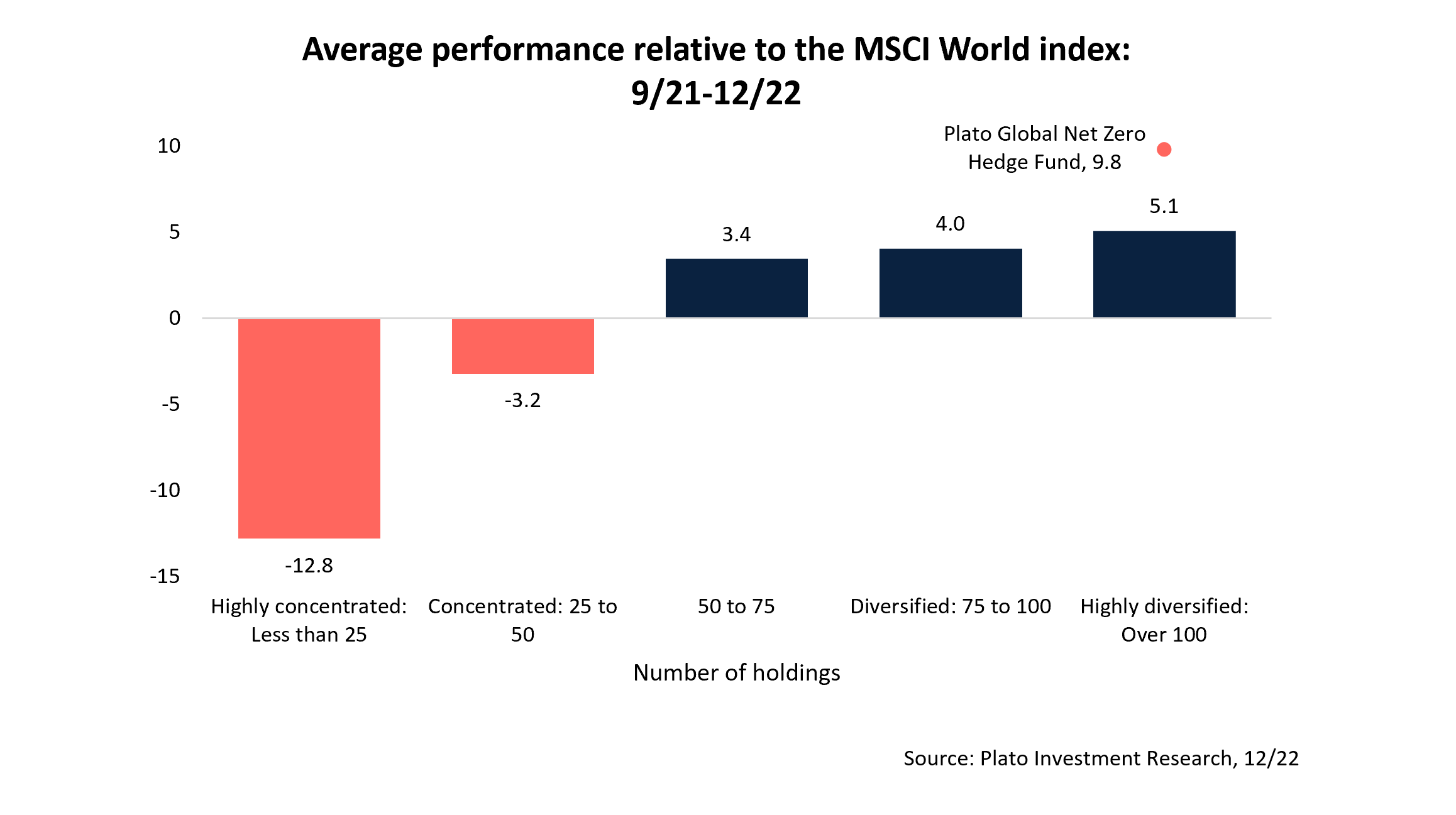

The chart below shows the average performance of global equity funds vs. the MSCI World by number of holdings since September 2021, the inception date of the Plato Global Net Zero Hedge Fund. For this analysis we took every global equity fund in the Morningstar database.

The results are striking. The most concentrated portfolios, holding less than 25 stocks imploded, underperforming by an average of 12.8%. Portfolios with 25 to 50 holdings also underperformed. These averages obscure some rather frightening underperformance from individual funds, with several underperforming by 30, 40 and 50%.

Meanwhile, you can see portfolios with more than 100 holdings outperformed by more than 5%.

How is it possible for well diversified portfolios like these to outperform so strongly? The global developed market equity universe contains almost 10,000 securities. A portfolio that holds 100 is therefore holding the most attractive 1% of opportunities and is a bona fide best ideas portfolio.

The Plato Global Net Zero Hedge Fund also has over 100 holdings and we have generated higher returns – outperforming the MSCI World index by almost 10% since inception.

Yes, Buffett has long rallied against the evils of “diworsification” – arguing that one should instead put all their eggs in one basket and watch that basket. However, this model has come crashing back to earth with many marquee managers underwater versus their benchmarks not only in 2022, but since inception.

The longer-term evidence

You could argue the above chart doesn’t provide a conclusive illustration of the performance of high concentration, covering a period which was predominately a bear market.

An analysis of the longer-term performance of concentrated managers versus diversified managers was also conducted by Morningstar.

Morningstar Research Services looked at the concentrated portfolios argument using a large sample of US mutual funds between January 1994 and December 2018.1

They concluded there was no statistical difference between the performance of the most concentrated and the most diversified funds. However, they did find that the more concentrated funds tend to have higher fees and more unpredictable returns.

“There Isn’t A Significant Relationship Between Portfolio Concentration And Gross Returns Among U.S. Equity Mutual Funds. Yet, Concentrated Managers Tend To Charge More, And The Risk Of Manager Selection Is Greater For These Funds Because Of The Wider Range Of Potential Returns Between Winners And Losers.”

Active share: A superior proxy for conviction?

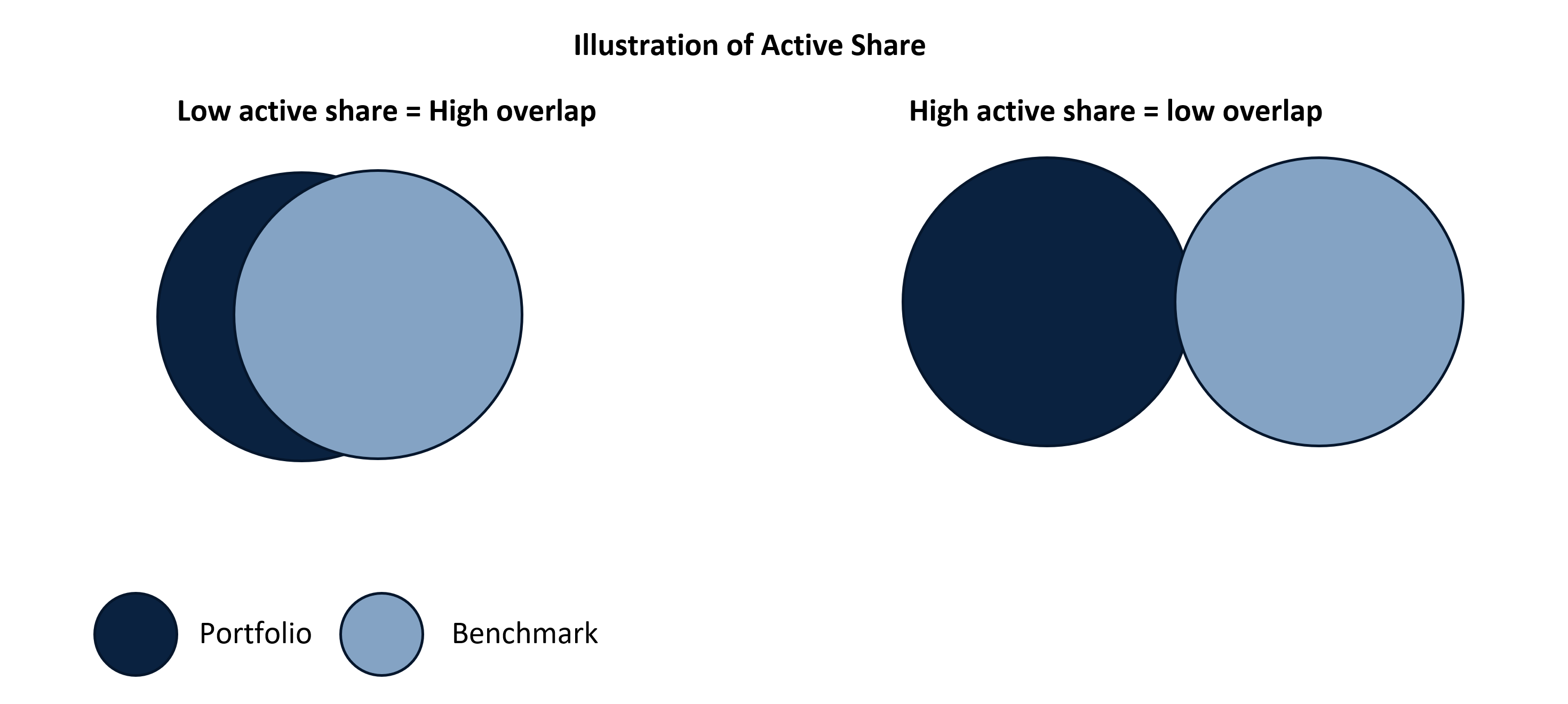

Active share measures the differences between a portfolio’s holdings and its benchmark.

In the below diagram, the dark blue area is the overlap between the holdings of a portfolio and its benchmark. The light blue area represents the non-overlapping holdings and is referred to as the active share. An index fund2 will have an active share of 0%, and an equity fund with no holdings in common with the benchmark will have an active share of 100%.

A portfolio that capitalisation weights the thirty largest holdings in the ASX 300 is not what most people would describe as high conviction.

The active share metric correctly diagnoses this with an active share of just 30%. Perhaps unsurprisingly, funds with the highest active share tend to outperform the market, whereas highly concentred funds do not.3

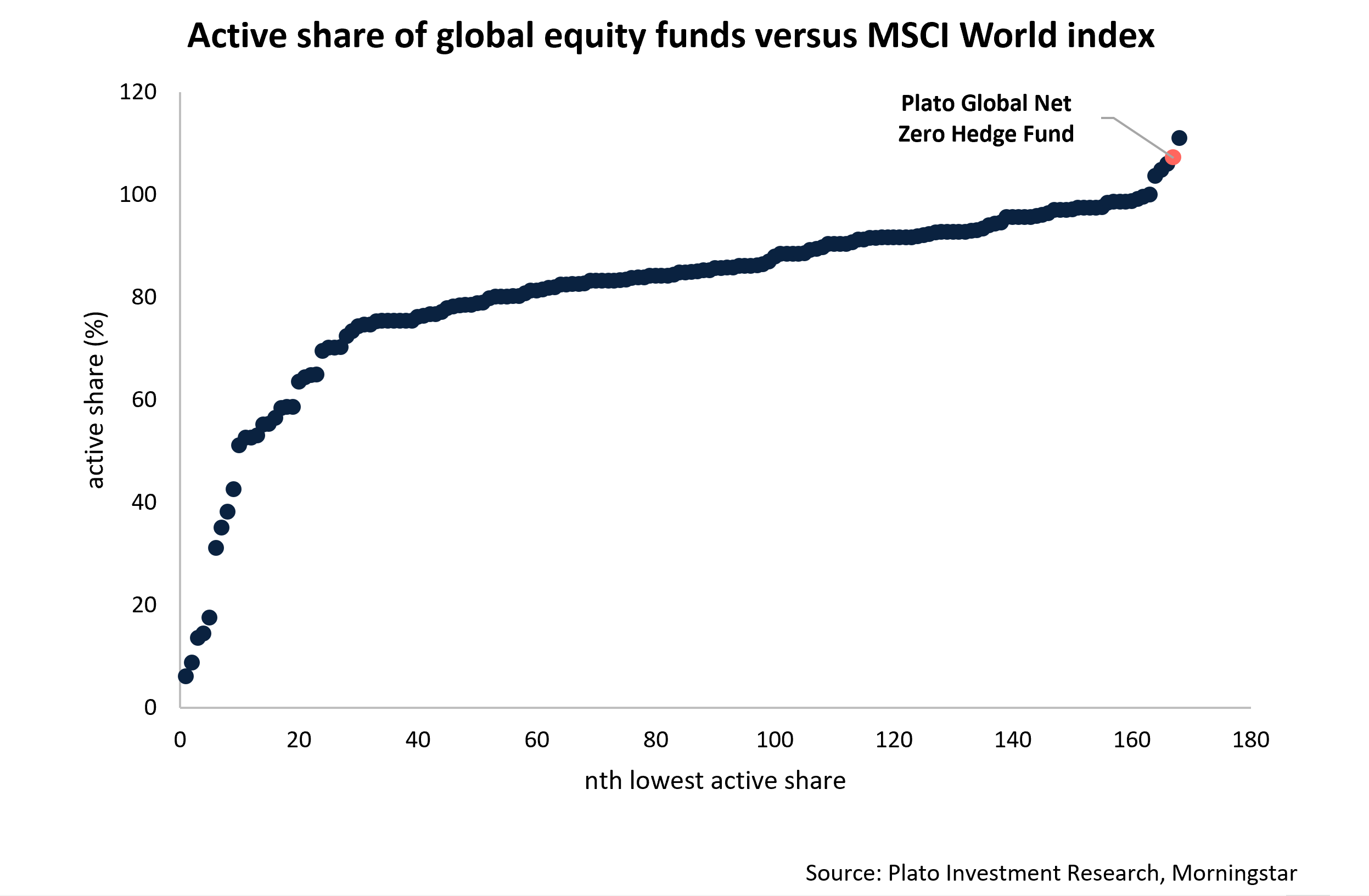

The active shares of all global equity funds in the Morningstar database are shown below, ranked low to high.

The Plato Global Net Zero Hedge Fund is a case in point. Since launch, the fund has outperformed the MSCI World index by 9.8% after fees, despite having a higher number of holdings than a typical concentrated fund.

The active share exceeds 100% (106%) which is possible because the portfolio is invested 150% long and 50% short.

The extra 50% on the long side relative to a traditional long-only fund gives 50% more exposure to our most attractive ideas, while the 50% short exposure allows the fund to profit by identifying underperformers.

Since launch, the majority of Plato Global Net Zero Hedge Fund’s excess returns have been generated from the short side. The larger number of holdings leads to a smoother, more predictable return stream and less stock specific drawdowns, for example when a certain electric vehicle CEO decides to become the CEO of Twitter.

A final word

The key takeaway from all of this is the data shows like most things in life, there is more than one route to success. Star managers and ‘best ideas portfolios’, might work in some cases, but to generate strong investment returns through-cycle, investors should remain open-minded and question if the data behind conventional wisdom really does stack up.

Dr David Allen is head of Short/Long Strategies at Plato, managing the Plato Global Net Zero Hedge Fund. He holds a PhD from Cambridge and Bachelor of Business with First Class Honours.