Looking to 2023, income investors can’t ignore the tax-effective benefits of franking credits, and by extension of that, we think investors can ignore much of the scaremongering surrounding the future of franking credits.

In 2022 there were two key announcements from the Government regarding franking.

The first was draft legislation proposed in September preventing franking credits being attached to company distributions funded by a capital raisings. We see this as logical policy which will help protect the long-term integrity of the franking credits system. Not any of the additional income we delivered clients in franking credits in 2022, none came from distributions funded by capital raisings.

The second proposed change came in the October federal budget. Treasurer Jim Chalmers announced the tax treatment of off-market share buybacks would be aligned with on-market buybacks, meaning it’s likely no franking credits will be received by investors who participate in buybacks.

It’s true off-market buybacks provided some additional income to retirees and while we don’t support this move, we don’t believe it will have a major impact on retirement income.

Of the 9.8% income our Plato Australian Shares Income Fund has delivered since inception (including dividends and franking credits), off-market buybacks have been just a small part of that franking component, and importantly this move only impacts shareholders willing to sell their shares.

The bread and butter of franking income for Australian investors over many decades has come from sustainable dividend distributions by companies with strong balance sheets and quality management. This will not stop and there are no proposed changes to this.

Through active portfolio management and astute stock selection, there is no reason why income investors should not be able to maintain their historical level of average annual franking credit income, despite this change.

There is also a reasonable argument to make that because companies can no longer do off-market buybacks, they may pay out generally higher dividends and franking, given there will be no way to do this through off-market buybacks anymore. Companies have an incentive to distribute all the franking credits on their balance sheet – now they’ll only be able to do that with dividends.

So, in 2023 franking credits are here to stay (despite the hyperbole) and companies paying fully franked dividends can’t be ignored.

For every one dollar of income received from fully franked dividends by pension-phase and other tax-exempt investors, an additional 43 cents on top in franking is received.

Plato’s modelling is projecting that at an index level in 2023 the ASX200 will deliver a cash yield of 4.4%, and 6.0% when including franking credits. On top of this, we think active and tax-effective portfolio management will deliver significant additional income.

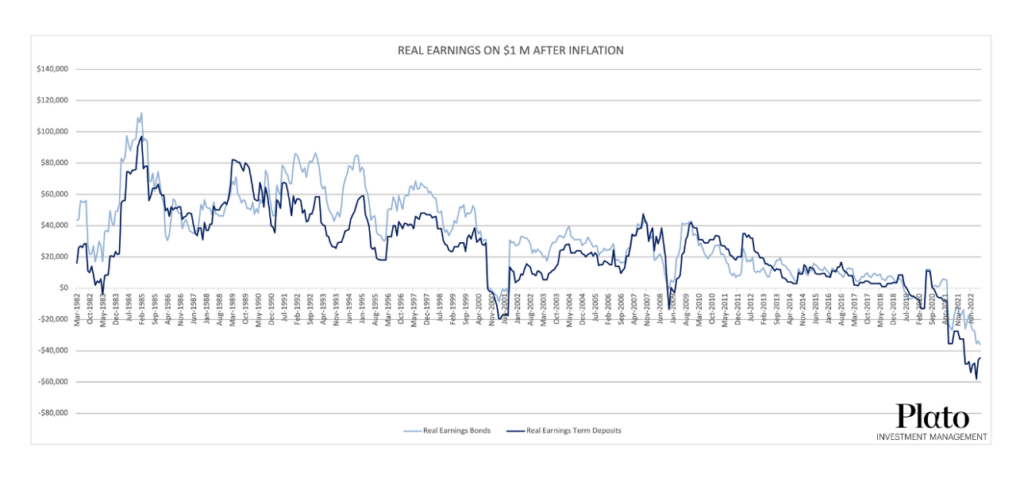

This is as term deposits and bonds continue to lose money in real terms (adjusted for inflation), as highlighted in the chart below.

Source: Plato, RBA. Updated On 30 September 2022.