by Lei Qiu – Portfolio Manager, Disruptive Innovation Equities

Technology stocks have been pummeled this year, leading some investors to question the sector’s future. But despite the downturn, we think technological innovation is entering a new phase in several areas poised for strong growth.

Investors in technology stocks have been badly bruised. MSCI World Index technology stocks plunged by nearly 33% this year through September 30 in local-currency terms. In the US, the technology-heavy Nasdaq Composite Index has fallen by a similar amount while nonprofitable tech stocks suffered even steeper losses. After several years of steady gains, investors face a reckoning. Is this year a correction to align stock valuations with realistic company earnings? Or does it reflect a major slowdown in a sector that has matured after the pandemic-accelerated consumer use of technology? Perhaps there simply isn’t much growth left anymore.

Questions like these are inevitable but miss the point. In fact, the market for technology is changing, innovation is broadening, and new areas of leadership are emerging. Investors who search for growth in the right places can find exciting opportunities.

What’s Changed on the Innovation Curve?

Over the last two decades, innovation was driven by the proliferation of broadband and mobility. Since the iPhone launched in 2007, billions of people around the world embraced newfound abilities to surf, shop and play via their mobile devices. This drove massive growth in companies that powered mobile ecosystems, including network providers, chipmakers and phone manufacturers.

The technology and new media giants enjoyed explosive growth. Facebook, Apple, Amazon, Netflix and Google became known as the FAANGs, a group of highly profitable mega-cap stocks that seemed unstoppable until this year.

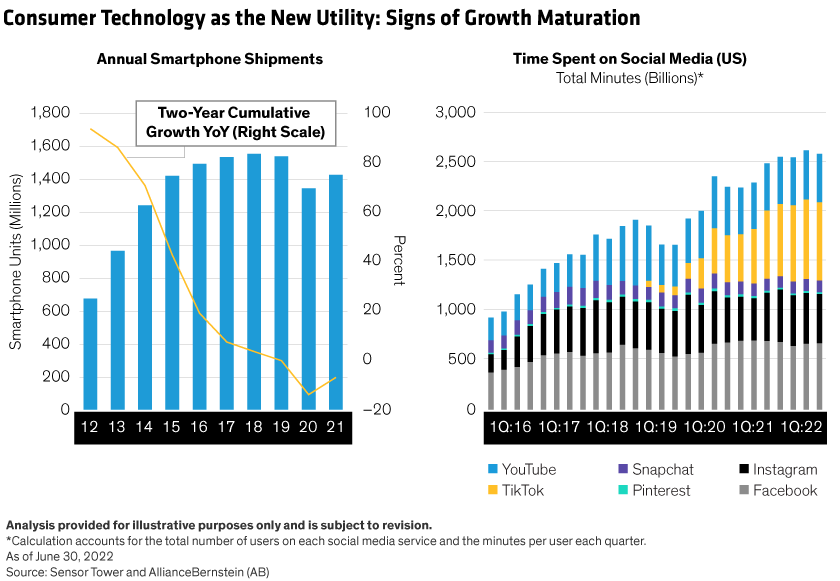

Some of these markets have matured (Display). For example, global smartphone penetration has exceeded 100% and unit shipments are slowing. The rapid growth in social media may also be peaking. To be sure, companies at the heart of the last digital decade are still likely to deliver growth. But they’ve become like utilities—companies that deliver essential services and may have reached peak profitability.

What’s Next? Technology-Enabled Infrastructure Transformation

But technology isn’t dead. On the contrary, innovation is fueling the transformation of technology-enabled infrastructure, which has become a necessity because of changes in consumer behavior. Every company that wants to survive and thrive in a digital world must strategically address its technology infrastructure. As a result, we believe that demand for advanced infrastructure technology will persist, even in a bleak economic environment.

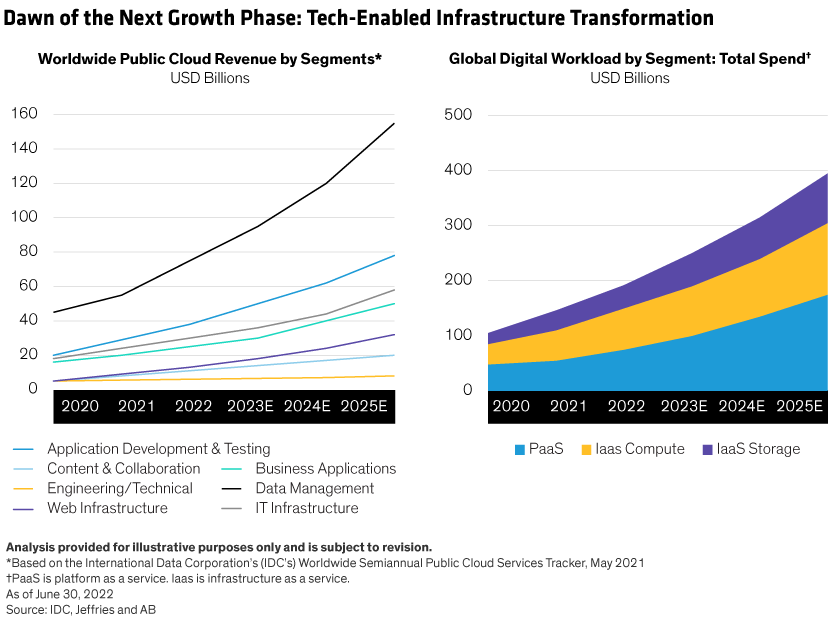

That’s because the future of society is rooted in digital technology. In the post-pandemic new normal, companies must ensure the flexibility and efficiency of their workforces. To do so, they must rapidly shift workloads to the cloud, using business applications and data-management tools (Display). This requires more spending in cloud infrastructure to ensure faster and reliable processing and response, along with cybersecurity tools to safeguard the virtual work environment.

Inflation is another impetus for technology spending, as companies face cost pressures because of labor and resource shortages. Companies worldwide are reviewing supply chain vulnerabilities, seeking to insource more activities and achieve energy independence amid the changing geopolitical landscape. Technological innovation can provide relief to cost deflation in many ways.

Where Are the Next Big Opportunities?

Different types of companies will require different technological solutions. However, some clear trends are already apparent.

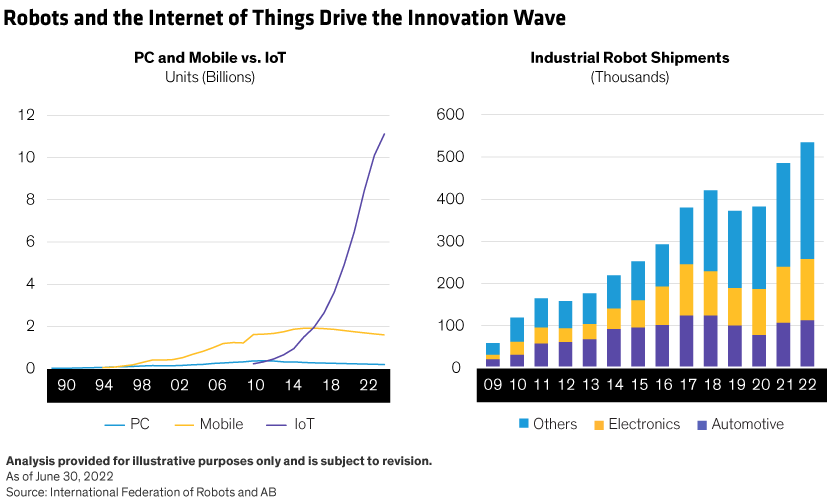

Robotics are on the rise (Display). It isn’t happening only in the auto and electronics industries, which were early adopters. From healthcare to agriculture to retail and logistics, companies are discovering that robotics can unleash efficiencies and cost savings, with faster and more formidable computing power than ever, and artificial intelligence capabilities to make decisions that mimic humans’.

Humans and machines are also communicating in new ways via the Internet of Things. Smart, cheap sensors are enabling the interconnection of every machine, checkout point and product, reshaping communication between humans and machines—and between machines. This is creating an “Internet of Everything” and redefining the future of manufacturing and transportation, with massive commercial potential.

Meanwhile, global efforts to push for energy independence also depend on technology. Innovation will make solar and wind power, as well as electric vehicles, more economical. Energy generation, storage and management all require technology solutions.

What do all these things have in common? First, the new innovation wave will transcend economic stress, since they address growing and enduring needs. Second, the companies enabling technology innovation are still maturing, and in many parts of the market, the leaders are still being defined. Market historians will recall how legends and leaders are constantly being replaced. From the nifty fifties of the 1970s to the four horsemen of the 1990s (Microsoft, Dell, Cisco and Intel) to the FAANGs, this is a normal process of renewal of leadership, particularly in the technology sector.

Equity investors should not be deterred by this year’s technology sector declines. Shares of technology companies now trade at much more attractive valuations than a year ago, creating attractive entry points for those with solid business models. The time is right to identify the next generation of innovative technology leaders that are transforming the world’s industrial economies and unlocking strong equity return potential along the way.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.